Since Bitcoin (BTC) was introduced to the world as an alternative to the current central bank system with a dying US dollar that is backed by nothing as its reserve currency, but now there is a plan by several governments to move ahead with implementing their own central bank digital currencies (CBDCs), which is a digital form of currency that is still backed by, you guessed it, nothing. The Nigerian government had made the decision to be the financial guinea pig for the globalist CBDC scheme, and so far, it has failed and that’s the good news. The bad news is that certain governments are still moving forward with the idea of using government-issued digital currencies. In the case of Nigeria, its citizens rejected their government’s plan to issue CBDCs by restricting cash in efforts to create a cashless society and so far, it seems that it has failed in epic fashion according to an opinion piece by author Nicholas Anthony that was published by coindesk.com ‘Nigerians’ Rejection of Their CBDC Is a Cautionary Tale for Other Countries’ is a warning to governments who are willing to take the same step:

In Nigeria, citizens have taken to the streets to protest the nation’s cash shortage, further objecting to their government’s implementation of a central bank digital currency (CBDC). The shortage came about due to cash restrictions aimed at pushing the country into a 100% cashless economy. Yet, instead of adopting the CBDC, Nigerian protesters are demanding paper money be restored.

The country’s experience strongly suggests the average citizen understands that CBDCs present a substantial risk to financial freedom while providing no unique benefit

Not only did the Nigerian people reject CBDCs, but they also demanded a return to paper currencies because they quickly found out that financial freedoms would be severely limited.

The concerns ranged from risking financial privacy to the possibility of financial oppression by government institutions. Anthony mentioned how “the Nigerian government has unleashed a flurry of tricks to spur adoption, but none has proven effective.” He even gave credit to the Nigerian government in terms of using modest approaches to influence its citizens to use CBDCs and it still failed:

To its credit, the Nigerian government initially tried to encourage use through modest measures. In August 2022, it removed access restrictions so that bank accounts were no longer required to use the CBDC. Then, in October, it offered discounts if people used the CBDC to pay for cabs. Yet, neither effort proved to be fruitful. Put simply, Nigerians prefer cash

However, the Nigerian government continued its assault on cash:

Unfortunately, the Nigerian government doubled down and moved to more drastic measures by restricting cash itself. In December the Central Bank of Nigeria began restricting cash withdrawals to 100,000 naira (US$225) per week for individuals and 500,000 naira ($1,123) for businesses.

To make matters worse, the Nigerian government also chose to redesign the currency during this time in a “move aimed at restoring the control of the Central Bank of Nigeria (CBN) over currency in circulation” and to “further deepen the push to [a] cashless economy,” according to a CBN press release

The Nigerians had a hard time adapting to the government’s restrictions on their hard earned cash, so they posted their concerns on Twitter, Tik Tok and other social media platforms to let the world know what went wrong. Soon after, major protests erupted on the streets because of the cash shortages imposed by the Central Bank of Nigeria:

NAIRA SCARCITY: Viral video shows the moment Benin protesters attempted to invade CBN office.

Protesters attempted to invade the Central Bank of Nigeria at Ring road in Benin, Edo State on Wednesday. pic.twitter.com/5sQcLfFeDo

The government decided to redesign the currency to restore control over the Central Bank of Nigeria as its governor, Godwin Emefiele claimed that “the destination, as far as I am concerned, is to achieve a 100% cashless economy in Nigeria.” To add insult to injury, “the company that designed the Nigerian CBDC called the cash restrictions a creative use of marketing and said other countries could be expected to take similar steps.” A top manager from a financial institutional ratings firm called Agusto and Co., Ayokunle Olumbunmi said that the central bank “doesn’t want us to be spending cash. They want us to be doing transactions electronically, but you can’t legislate a change in behavior.” Anthony concluded that the idea of CBDCs will not go very far, “CBDCs may be popular among central bankers, but money is ultimately a tool for the people. So long as the risks outweigh the benefits, it’s unlikely any CBDC will gain traction in Africa or elsewhere.”

Nicholas Anthony was correct to point out that CBDCs will not become mainstream as several countries have already demonstrated their unwillingness to move forward with the new form of digitized currencies.

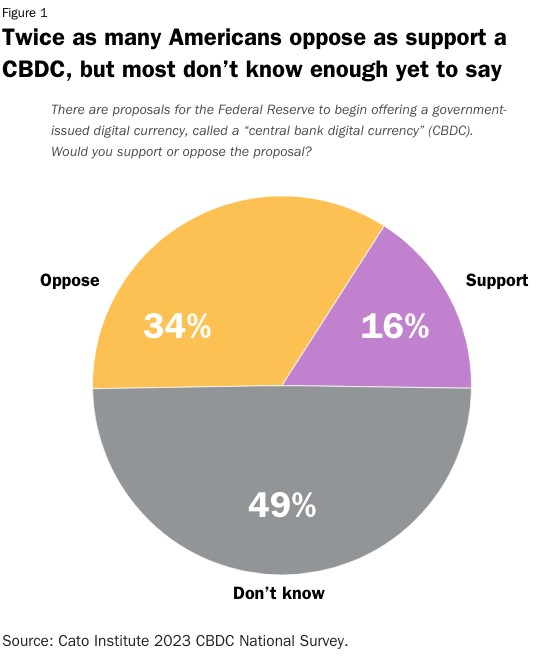

The average human being on earth understands that CBDCs is a bad idea, even in the United States where two-thirds of the population believes almost anything that their government tells them to believe are skeptical of CBDCs according to the Cato Institute, a think tank who also published an article by Nicholas Anthony on the findings of a survey that was conducted by the US federal Reserve Bank on how people view CBDCs. Here is what they found, “Specifically, more than 66 percent of the 2,052 commenters were concerned or outright opposed to the idea of a CBDC in the United States (Figure 1).”

Bitcoin.com published an article on the GOP’s 2024 presidential candidate, Florida’s governor, Ron DeSantis who is opposed to CBDCs,‘Ron DeSantis Vows to Prohibit CBDC, ‘Woke Politics,’ and ‘Financial Surveillance’ in Florida,’ he said “I think what the danger of the digital currency is that, one, they want to make that the sole currency, they want to get rid of crypto,” DeSantis continued, “They don’t like crypto because they can’t control crypto. So, they want to put everything in a central bank digital currency.” There were other politicians who also have similar views on CBDCs:

DeSantis shares the view of several Republican officials who have criticized the idea of a central bank digital currency (CBDC). Minnesota congressman Tom Emmer introduced the Central Bank Digital Currency (CBDC) Anti-Surveillance State Act, while Texas senator Ted Cruz has created legislation against the government developing a CBDC. Georgia representative Marjorie Taylor Greene has also spoken out against CBDCs, and 2024 Democratic presidential candidate Robert Kennedy Jr. has warned that a central bank digital currency could lead to financial slavery

Cash is King! How the CBDC Failed in Japan and Ecuador

Cointelegraph.com, an independent digital news platform that focuses on crypto assets, blockchain technology and emerging fintech trends published an article last year written by Helen Partz based on which countries have rejected CBDCs for one reason or another titled ‘Some central banks have dropped out of the digital currency race’ mentions Japan, who is a major player in the global economy, ultimately rejected developing a CBDC scheme. The Bank of Japan (BOJ) started testing their digital currency proof-of-concept in 2021 and had planned to finish the first phase by 2022 but in January “former BOJ official Hiromi Yamaoka advised against using the digital yen as part of the country’s monetary policy, citing risks to financial stability.”

The BOJ issued a report in July 2022 and stated that it had no plan to establish a CBDC system since there is a “strong preference for cash and high ratio of bank account holding in Japan” and that the regulator suggested for a CBDC to be used as a “public good” and it “must complement and coexist” with “private payment services in order for Japan to achieve secure and efficient payment and settlement systems.” However, it also said that “the fact that CBDC is being seriously considered as a realistic future option in many countries must be taken seriously,” in other words, the CBDC scheme in Japan will not move forward although several countries are still in the early stages of developing a plan for the use of CBDCs, but for Japan, cash is still and will be king well into the foreseeable future.

Ecuador is another example as its central bank, Banco Central del Ecuador (BCE) who launched its own electronic currency known as dinero electrónico (DE) in 2014 to increase some sort of financial inclusion for the public as well as to control the flow of fiat currencies. According to Partz “As of February 2015, Ecuador managed to adopt DE as a functional means of payment, allowing qualified users to transfer money via a mobile app. The application specifically allowed citizens to open an account using a national identity number and then deposit or withdraw money via designated transaction centers.” But industry observers were not so sure that the DE can take the form of a CBDC since Ecuador’s currency is the US dollar, and since Ecuador does not currently have its own sovereign currency, many were not so sure that they can call the DE, a form of CBDC. “The Ecuadorian government cited the support of its dollar-based monetary system as one of the goals behind its DE platform after it started to accept U.S. dollars as legal tender in September 2000.” It seems that Ecuador remains skeptical on any possibility that issuing CBDCs will be a success:

According to online reports, Ecuador’s DE operated from 2014 to 2018, amassing a total of 500,000 users at its peak out of a population of roughly 17 million people. The project was eventually deactivated in March 2018, with the BCE reportedly citing legislation abolishing the central bank’s electronic money system. Passed in December 2021, the law stated that e-payment systems should be outsourced to private banks.

Years after dropping its central bank digital money initiative, Ecuador has apparently remained skeptical about the whole CBDC phenomenon. In August 2022, Andrés Arauz, the former general director at Ecuador’s central bank, warned eurozone policymakers that a digital euro could potentially disrupt not only privacy but also democracy

Bottom line, the CBDC will not be a standard for financial transactions for the few countries who already tried launching their versions of digital currencies.

However, in the US, the Federal Reserve’s ‘FedNow’ was supposed to be launched sometime in July 2023. Here is the Federal Reserve’s Press Release:

The Federal Reserve announced that the FedNow Service will start operating in July and provided details on preparations for launch. The first week of April, the Federal Reserve will begin the formal certification of participants for launch of the service. Early adopters will complete a customer testing and certification program, informed by feedback from the FedNow Pilot Program, to prepare for sending live transactions through the system.

Certification encompasses a comprehensive testing curriculum with defined expectations for operational readiness and network experience. In June, the Federal Reserve and certified participants will conduct production validation activities to confirm readiness for the July launch.

“We couldn’t be more excited about the forthcoming FedNow launch, which will enable every participating financial institution, the smallest to the largest and from all corners of the country, to offer a modern instant payment solution,” said Ken Montgomery, first vice president of the Federal Reserve Bank of Boston and FedNow program executive. “With the launch drawing near, we urge financial institutions and their industry partners to move full steam ahead with preparations to join the FedNow Service”

For the US population, FedNow is a test that will eventually fail. People will be skeptical about a central bank digital currency once it proves that it is used to surveil people’s spending habits and control what they spend their money on, and God forbid they are anti-war, anti-vaccine activists, homeschoolers, pro-gun supporters or conspiracy theorists, the bankers can cut them off from using CBDCs and then what happens? Will there be riots in the streets?

Since Bitcoin was introduced as an alternative to central bank control, the creation of the CBDC is their answer in hopes of retaining their power, but that idea is not likely to happen, it will in some way, backfire.

When it comes to Bitcoin, it’s a different story. In an interesting article written by Jay Speakman of beincrypto.com ‘When You Buy Bitcoin You Gain Freedom’ says that “in a world where economic and political uncertainties abound, owning Bitcoin (BTC) could provide the path toward financial freedom and autonomy. It’s no longer just about investing in a digital asset. It’s about making a revolutionary move to gain control over your finances and future.” Speakman makes several main points on why people should own Bitcoins and one of those points is that owning sovereign cryptos such as Bitcoins, Ethereum’s and others is a step towards financial freedom:

It provides the opportunity to participate in the global economy without the limitations of traditional banking systems. Bitcoin is not subject to government regulations. At least not yet, and it is free from the inflationary policies which can erode fiat currency values. This means Bitcoin provides an alternative and potentially more secure, store of value

Another reason for owning Bitcoins is for future investment purposes:

Investing in Bitcoin is no longer simply making money. It is about investing in your future and securing your financial freedom. Bitcoin’s decentralized financial system operates independently of central authorities or governments. This means it is resistant to censorship and regulation. Bitcoin holders can make transactions without the need for banks, which are subject to government intervention

“Investment Diversification” is another reason to own Bitcoins since putting all your eggs in one basket, especially in a globalist banking system, is a bit risky:

Investing in Bitcoin can provide portfolio diversification as it is not correlated to traditional assets such as stocks and bonds. This means it may provide a hedge against inflation and market volatility, mitigating the risks associated with traditional investment portfolios

However, owning Bitcoins does have risks like everything else since the “market is notoriously volatile. Prices often fluctuate wildly based on a range of factors, from government regulations to media coverage.” Speakman also mentions that “BTC transactions can result in a permanent loss of funds. There is also the risk of hacking and theft, as these transactions are irreversible and untraceable.”

In conclusion, the article lays out what owning Bitcoins could mean for individuals and investors alike especially for those who do not trust the traditional banking system:

The decision to buy BTC is more than just a financial investment. It’s a move towards financial freedom, control, and security. Bitcoin’s feature of allowing individuals to act as their own banks. Providing a secure alternative to traditional banking systems which have exhibited instability and vulnerability to failures. Furthermore, the appeal goes beyond just financial security and autonomy. The digital currency resonates with libertarians who value individual freedom and limited government intervention. Despite a torrent of dissenting voices Bitcoin continues to gain mainstream adoption. As the technology continues to mature, it may address some of the concerns raised by the dissenting voices.

Investing in digital assets may involve risks such as volatility and the potential for hacking and theft. Yet, the benefits of financial freedom outweigh the downsides. As the world becomes increasingly uncertain, owning Bitcoin could be the first step toward financial security and autonomy

When you look at the difference between CBDCs along with the system imposed by international banking cartels who still maintain some form of financial dominance versus the Bitcoin revolution, there is a difference. CBDCs means no financial freedoms and owning Bitcoins means the exact opposite. Even though Bitcoins are still in the early stages, there is hope in the new crypto technology. But like everything else, you should be cautious, do not invest 100% of your net worth in just one asset, in other words, invest maybe 5% in bitcoins, and the rest? 15% in emergency preparedness (food, water filters, guns, flashlights, etc.) 20% in real estate or invest in a second passport, 20% in hard assets like gold, silver and copper, 20% in high-end watches, antiques, aged wines and liquor, collectibles etc. and the last 20% in foreign stocks especially those that are in politically stabilized environments or in gold and silver mining companies, but that’s just my opinion.

Government-backed CBDCs will be a failure because the people already do not trust international banking cartels to totally control their finances. So, for these banks to have total control over your financial wellbeing under their CBDC scheme would be an extremely difficult task for them to manage.

The banking cartel or the financial bureaucrats are about to discover that they will be in over their heads with an angry population. Just imagine if the banking cartels, certain governments and their corporate conglomerates are in control over the people’s finances, they will get to determine who eats and who will starve. This is the ultimate power grab the globalist bankers have been dreaming about for a very long time, but will the people stop this from happening? I’m an optimist, so I believe that they will demand their financial freedoms and that is something of value that they can hold and control in their own hands. The case for CBDCs will be a hard sell, so central banks who are proposing this idea should think twice about what they are trying to impose on the public, if not, they will face some form of resistance just like they did in Nigeria.

Building on millennia of learning how to structure and manage an economy to accumulate and consolidate control and wealth in particular hands, as explained in Part 1 of this investigation, the Global Elite launched its final coup in January 2020 under cover of the fake Covid-19 ‘pandemic’. Using the health threat supposedly implied by the existence of a pathogenic ‘virus’, the bulk of the world population was terrorized into submitting to an onerous series of violations of their human rights which was tantamount to a declaration of martial law. See ‘The Final Battle For Humanity: It Is “Now or Never” In The Long War Against Homo Sapiens’.

Under a barrage of propaganda delivered by Elite agents – including organizations such as the World Economic Forum, the United Nations, the World Health Organisation, governments, the pharmaceutical industry and corporate media as well as individuals such as Klaus Schwab, Yuval Noah Harari and Bill Gates – people were compelled to wear masks, use QR codes, stay locked down in their homes and, later, submit to a series of experimental but involuntary gene-altering bioweapons to acquire a ‘vaccine passport’, among other measures.

This inevitably adversely impacted the entire supply chain: That is, the process that connects the production of raw materials, such as food grown on farms and minerals mined from the Earth, to factories that produce everything from canned food to computers, and then to outlets that sell these products to the public. All components of this chain were either shut down completely at one or more times, as part of the imposed restrictions or other policy measures – watch, for example, ‘Biden pays farms to STOP – EU out of Feed – Meat taxes & Chicken permits – Up to you to GROW FOOD!’ – or just substantially curtailed by the unavailability of essential inputs, ranging from replacement parts to competent labour.

To exacerbate matters, the transport industry (trucking, railroads, shipping, airlines) was also effectively shut down, containers became unavailable (because they were in the wrong places) and logistics corporations (that organize the movement of trade goods) were disabled, including by cyber attacks. The airline and tourist industries were just two industries that were profoundly disrupted. But so was much of small business, with many businesses destroyed. As a result, hundreds of millions of people lost employment, many permanently, throughout the industrial economies and millions more were starved to death in Africa, Asia and Central/South America because the day-to-day economy, by which many survive, was shuttered and any ameliorative measures by governments and international organizations were, deliberately, woefully inadequate (or were siphoned into elite wallets). See ‘The Global Elite’s “Kill and Control” Agenda: Destroying Our Food Security’.

But ‘behind the (obvious) scenes’ outlined above, there has been a great deal more going on that has been deliberately concealed from public view, and this has been considered and discussed by some fine analysts.

According to Catherine Austin Fitts, using ‘national security’ as the justification, the U.S. National Security Act 1947 and the CIA Act 1949 were the basis of a series of Acts and Executive Orders that ‘created a secrecy machinery’ which essentially meant that ‘the most powerful financial interests in the world can keep a whole bunch of money secret’, thus creating a secret black budget. And, starting in 1998, according to US federal government documentation, huge sums of money were not accounted for while private equity firms began exploding and, despite having no capacity to raise such amounts, were suddenly investing huge sums of money in emerging markets. According to Fitts ‘we are now missing over $US21 trillion’, which she calls a ‘financial coup d’etat’ that is clearly in ‘massive violation’ of the US constitution. The financial value of what has transpired under the Covid-19 narrative is that the ‘magic virus’ can be used to explain, for example, why there is no money for healthcare or pension funds cannot pay on retirement those who paid into them throughout their lives. Watch ‘We Need to Talk about Mr Global – Part Two’ with a simple summary here: ‘The Real Game of Missing Money’.

‘We are now over $US100 trillion of undocumentable adjustments if we use their most recent figures and so I would say we are describing a financial system which is completely and utterly out of control…. If any of the allegations about financial fraud in the 2020 [US Presidential] election are true, and I believe that many of them are, we’ve now delinked both the election system and the finances [from] the constitution and the law so we are are now operating both in terms of who governs and how they spend the money completely outside of the law and completely outside of any democratic process. So this is a coup.’

To which Professor Skidmore responds:

‘The reason that I really struggled… watching what was going on during the last financial crisis, [was that] I thought ‘Wow we don’t have the rule of law’. It was so obvious that we didn’t ten years ago and it’s like it’s devolving even more and so I am not sure how much further we can go before we are just completely devoid of the rule of law at least for a subset of the very powerful.’

As an aside, while genuinely appreciative of the research of Fitts and Skidmore, as outlined earlier in this article and previously demonstrated, democracy has always been a sham and the Elite has always operated beyond the rule of law, routinely corrupting national political processes in pursuit of Elite ends. See ‘The Elite Coup to Kill or Enslave Us: Why Can’t Governments, Legal Actions and Protests Stop Them?’ All we are seeing in the current context is Elite corruption being flaunted in a way that reflects the sure knowledge that it can act corruptly, on a global scale, with impunity.

But to return to the subject at hand: In 2019, the central bankers of the G7 countries met for their regular conference at Jackson Hole, Wyoming and agreed to the ‘Going Direct Reset’, a plan devised (and later orchestrated) by BlackRock – see ‘Dealing with the next downturn’ – and, as explained by John Titus, the fundamental purpose of this ‘Reset’ was to orchestrate the largest asset transfer in history under cover of the forthcoming Covid-19 ‘pandemic’. Watch ‘Larry & Carstens’ Excellent Pandemic’ with a summary here: ‘Summary – Going Direct Reset’.

In the words of Titus: ‘In a nutshell, the arrival of the 2020 pandemic was about as accidental as an assassination. The pandemic narrative is nothing but a cover story to conceal from the public what in reality is the biggest asset transfer ever.’ See ‘Summary – Going Direct Reset’.

While you can learn the mechanics of how this was conducted in the excellent documents and videos immediately above, as Fitts points out in relation to the central banks: ‘Controlling and having access to data on fiscal and monetary policy is the basis of huge fortunes.’ And, combined with the secrecy that has protected their manipulations from public view – ‘if you look at all the technology and assets that have been transferred, by questionable means, into private and corporate hands, the liability is over the top’ – it has engendered the view that their only way forward is ‘complete, total central control’.

Central Bank Digital Currencies

How will this ‘total control’ be achieved? One key element will be the introduction of Central Bank Digital Currencies (CBDCs). According to Fitts: The fundamental value of digitized systems, from the elite perspective, is that they enable centralized control. So, by creating CBDCs the financial transaction control grid becomes the means by which you enable centralized control; that is, slavery. Watch ‘We Need to Talk about Mr Global – Part Two’.

How does this work? CBDCs allow the Central Bank to determine exactly what products and services your digital currency can be spent on, when it can spent and where it can be spent. It also allows the issuing authority to freeze, reduce or empty your bank account, and to alter its functionality with the latest ‘update’, based on your ‘social credit score’, political allegiance or if you do not comply with certain directives. But it goes beyond this.

According to the Bank for International Settlements:

‘The G20 has made enhancing cross-border payments a global priority and has identified CBDC as a potential way forward to improving such payments. A “holy grail” solution for cross-border payments is one which allows such payments to be immediate, cheap, universally accessible and settled in a secure settlement medium. For wholesale payments, central bank money is the preferred medium for financial

market infrastructures. A multi-CBDC platform upon which multiple central banks can issue and exchange their respective CBDCs is a particularly promising solution for achieving this vision, and mBridge is a wholesale multi-CBDC project that aims to advance towards this goal. It builds on previous work…. Project mBridge tests the hypothesis that an efficient, low-cost, real-time and scalable cross-border multi-CBDC arrangement can provide a network of direct central bank and commercial participant connectivity and greatly increase the potential for international trade flows and cross-border business at large…. All the while safeguarding currency sovereignty and monetary and financial stability by appropriately integrating policy, regulatory and legal compliance, and privacy considerations.’ See ‘Project mBridge: Connecting economies through CBDC’.

Apart from the fact that the G20 governments are distinctly unrepresentative of the world’s people, these words are typical of the type usually chosen when the Elite is intent on sugarcoating their lies to conceal their true agenda.

Fortunately, Agustin Carstens of the Bank for International Settlements has been more forthcoming: ‘We don’t know, for example, who’s using a $100 bill today, we don’t know who is using a 1,000 peso bill today. The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that.’ Watch ‘Cross-Border Payments: A Vision for the Future’. And here is the Bank of England advising government ministers in the UK on the issue of programming CBDCs: ‘Bank of England tells ministers to intervene on digital currency “programming”’. For a more detailed explanation, see ‘What Is Programmable Money?’ And for an update on progress in your country, see ‘CBDC: A Country-by-Country Guide’.

Before proceeding, however, it is worthwhile noting the conflict that is going on between the central banks and the commercial banks (the traditional actors in the retail banking sector, that is, the part of banking where people interact directly with a bank), as well as that between the commercial banks and the big tech companies, such as PayPal, Alipay, Facebook and Amazon that have developed or are developing their own digital currencies and/or payments systems outside the traditional financial system. While non-bank financial institutions long-ago overtook commercial banks in lending, bank influence generally continues to decline and is accelerating in the face of the competition from the technology giants. Why the conflict? Because a CBDC risks collapsing the commercial banking sector completely by eliminating retail banking and thus destabilizing the long-standing financial system. For some discussion of this, watch Alice Fulwood’s presentation ‘Could digital currencies put banks out of business?’ There is no doubt, of course, that this conflict will be resolved and that it will not be in our favour.

And to elaborate the significance of imprisoning you in a ‘smart’ city, Patrick Wood points out the evidence both in the literature and in practice: The intention is to force us off the land, as is already happening in China, and at gunpoint if necessary, so that ‘vacated farm land’ can be combined ‘into giant factory farms to be operated by advanced technology such as agricultural robots and automated tractors’. Once relocated into the ‘smart’ city of the government’s choice, everyone will be subject to 24 hour surveillance using a plethora of ‘smart’ technologies such as biometric facial scanning, geospatial tracking and CBDCs, forced onto public transport which will not include the option of leaving the city, and confined to those work and other activities approved by the relevant technocrats. See ‘Day 9: Technocracy And Smart Cities’.

The bottom line, in simple language however, is the same as it has always been: Endlessly acting to consolidate their control over the rest of us, our money is being stolen by the Elite for their own ends and they are not required to report it and they cannot be held accountable, legally or otherwise. The only difference to what has happened historically is that now even the pretense of some form of equity, the rule of law and even the notion of democracy are being abandoned in the final rush to techno-totalitarianism and wealth concentration.

Not content with these measures, however, the war in central Asia was precipitated by the Elite to advance key elements of their program. Superficially portrayed by most politicians and corporate media as a war between Russia and Ukraine, many thoughtful analysts perceive some of the deeper strands of what has occurred: Since the collapse of the Soviet Union and NATO commitments made at the end of the Cold War, NATO has consistently violated those commitments and there has been routine Ukrainian attacks on Donetsk and Luhansk over the past eight years. These and other events have ensured a long but steady ‘lead time’ in the final build up to the war, precipitating the military response of Russia, as intended. For just four thoughtful analyses, see ‘Understanding The Great Game in Ukraine’, ‘Ukraine, Russia, and the New World Order’, ‘Some of Us Don’t Think the Russian Invasion Was “Aggression.” Here’s Why.’ and ‘The U.S. Is Leading the World Into the Abyss’.

Obscured by the war, however, the leaderships of both Russia and Ukraine are heavily involved in the World Economic Forum and both have been heavily committed to imposing the elite agenda on their populations. In short, the Russia-Ukraine war serves elite purposes well with consequences including even greater disruption of food and fuel supply chains than the ‘Great Reset’ was able to achieve alone. See ‘The War in Ukraine: Understanding and Resisting the Global Elite’s Deeper Agenda’.

Similarly, the sabotage of the Nord Stream 1 & 2 gas pipelines – see ‘Ukraine War: New Developments’ – might be seen through various lenses but, again, it serves elite purposes well. As Tom Luongo noted: ‘The important thing I keep trying to point out [is] that thinking in terms of “country” is ultimately the wrong lens to view these people’s actions. Factions are the better lens. Factions cross political borders.’ See ‘The Curious Whodunit of Nordstreams 1 and 2’. Given that the sabotage of these two pipelines is seriously exacerbating the energy crisis in Europe, while displacing people’s anger onto one or other parties in the war, as always the elite forces driving destruction of the world economy escape scrutiny.

Beyond this, on 7 October 2022 the Biden Administration dealt a ‘nuclear’ strike to the hi-tech industry by imposing onerous new export rules that cut off supply of essential technology (advanced semiconductors, chip-making equipment and supercomputer components) to China, immediately and adversely impacting Chinese production. See ‘Implementation of Additional Export Controls: Certain Advanced Computing and Semiconductor Manufacturing Items’. But whatever pain this will inflict on the Chinese, it will inflict far more pain on ordinary people who will be required to deal with the outcomes of this latest supply-chain disruption: higher prices, more battered household budgets and fewer families able to scrape by on shrinking wages. See ‘Biden’s Tech-War Goes Nuclear’ and ‘US Economic War on China Threatens Global Microchip Industry’.

In any case, the ongoing destruction of the global economy will continue even while, apparently, considerable effort is being made to restructure key elements of it, such as those in relation to trade relations, trade routes, currencies and international banking being undertaken in various international fora. For one discussion of these ongoing efforts, see ‘Russia, India, China, Iran: the Quad that really matters’.

But, again, how serious are these efforts when all governments are collaborating closely on the fundamental Elite program? At one of these meetings, recently concluded, the G20 Summit in Bali – see ‘G20 Bali Leaders’ Declaration’ – Moscow, Beijing, Washington and all other governments present, agreed to ‘the creation of a global health-preserving Pandemic Fund sponsored by the WHO, the World Bank, Bill Gates, and the Rockefeller Foundation. The fund will ensure there is plenty of money for experimental genetic vaccines in the weeks, months, and decades ahead.’ Beyond this, however, the Declaration contains ‘purple prose’ about ‘digital transformation’, ‘interoperability of Central Bank Digital Currencies (CBDCs) for cross-border payments’, and other elements of the Elite’s technocratic program. As Riley Waggaman observed: ‘It’s truly heart-warming that even amidst ceaseless geopolitical squabbling, Moscow and the Collective West can sit down at the negotiating table, break bread, and agree to cattle-tag the entire world.’ See ‘World leaders agree to cattle-tag the planet’.

And while a recent World Economic Forum report, based on the views of 50 chief economists from around the world, sanitized economic prospects by simply referring to a likely forthcoming ‘recession’ either in 2022 or 2023, spokesperson Saadia Zahidi couldn’t avoid mentioning the heavy consensus that real wages will decline, poverty will increase and ‘social unrest is expected to continue to rise’ in response to rises in the cost of living, particularly due to production and supply chain disruptions in fuel and food supplies. See ‘Special Agenda Dialogue on the Future of the Global Economy’.

Taking a similarly ‘moderate’ stance, in its recent ‘World Economic Outlook’, the International Monetary Fund warned that ‘More than a third of the global economy will contract this year or next, while the three largest economies – the United States, the European Union, and China – will continue to stall. In short, the worst is yet to come, and for many people 2023 will feel like a recession.’ See ‘World Economic Outlook – Countering the Cost-of-Living Crisis’. At the media briefing to launch the report, the Director of the IMF’s Research Department, Pierre-Olivier Gourinchas, noted that ‘the global economy is headed for stormy waters’ and ‘Too many low-income countries are close to or are already in debt distress. Progress toward orderly debt restructuring… is urgently needed to avert a wave of sovereign debt crises. Time may soon run out.’ See ‘WEO Press Briefing Annual Meetings 2022’.

But other reports suggest something far worse.

Summarizing his own extensive research on the subject over the past three years, in a recent interview Professor Michel Chossudovsky simply explains what triggered the economic collapse, referring to the origin of the crisis with decisions made in early 2020: ‘This is really Economics 101:… the announcement of the lockdown… implies the confinement of the labor force on the one hand and the freezing of the workplace on the other…. What happens? The answer is obvious: Collapse! Economic and social collapse on an unprecedented basis because it was implemented simultaneously in 190 countries.’ Watch ‘The Worldwide Corona Crisis, Global Coup d’Etat Against Humanity’.

Noting the complete failure of authorities to hold even one corporate executive to account for the financial collapse they caused in 2008 – when banking institutions intentionally sold securities they knew were bad to defraud customers and increase their own profits, as carefully reported in a ‘Frontline’ documentary in 2013 – Dr Joseph Mercola argues that the ‘same criminal bankers are now intentionally destroying the global financial system in order to replace it with something even worse – social credit scores, digital identity and Central Banking Digital Currencies (CBDCs), which will give them the ability to control not only your individual finances but also everything else in your life’. Apparently unaware of the extensive lead time on what is happening, he goes on to observe that ‘We’re now at the point where banksters have self-selected themselves to rule the whole world, tossing notions of democracy, freedom and human dignity in the waste bin along the way.’ See ‘Who Is Behind the Economic Collapse?’

As explained above, these ‘banksters’ operate beyond the rule of law too.

According to the Irish economist Philip Pilkington: ‘The Western world today faces a serious risk of slipping into another Great Depression. This risk has arisen… due to global economic relations deteriorating to the point of all out warfare.’ Noting the critical importance of the sabotage of the Nord Stream pipelines, leaving Europe with ‘insufficient access to energy, the price of energy in Europe will remain extremely high for years to come. European industry, for which energy is a key input, will become uncompetitive.’ See ‘The next Great Depression? Economic warfare has severe implications’.

According to former BlackRock manager, Edward Dowd, the outcome of what has been happening, which is being accelerated by the corruption that has plagued Wall Street since the 1990s, is that the forthcoming financial collapse is a ‘mathematical certainty’ and will occur within the next six to 24 months. Watch ‘Ex-BlackRock Manager: Global Financial Collapse a “Mathematical Certainty”’.

Or, in the words of strategic risk consultant William Engdahl: What is coming in the months ahead, barring a dramatic policy reversal, ‘is the worst economic depression in history to date’. See ‘Global Planned Financial Tsunami Has Just Begun’.

After listing a sequence of industry shutdowns and other measures in Europe because of energy shortages, Michael Snyder simply observes that ‘This is what an economic collapse looks like’, notes the prospect (also predicted by NATO Secretary General Jens Stoltenberg and, as we saw above, the World Economic Forum) of ‘civil unrest’ and warns that ‘Europe is going to descend into “the new Dark Ages” this winter, and the entire world will experience extreme pain as a result.’ See ‘This Winter, Europe Plunges Into “The New Dark Ages”’.

According to Irina Slav, countries of the European Union have suffered a consistent decline in gas and electricity consumption this year amid record-breaking prices. Businesses are shutting down factories, downsizing or relocating, while production of such basic products as steel, zinc, aluminium, chemicals, plastics and ceramics has been cut substantially, if not slashed dramatically. Observing that the European Union is heading for a recession that is ‘quite clear to anyone watching the indicators’ she goes on to state that ‘Europe may well be on the way to deindustrialization’. See ‘Europe May See Forced De-Industrialization As Result Of Energy Crisis’.

Dr. Seshadri Kumar agrees. He has offered an intensively detailed critique of the economic fallout from the ongoing Russia-Ukraine war and events such as the sanctions against Russia and the sabotage of the Nord Stream 1 & 2 gas pipelines. Following his careful analysis, he notes a series of conclusions including that ‘The scarcity of oil and gas, combined with the scarcity of commodities, will lead to the De-Industrialization of Europe in short order.’

‘Europe needs what Russia has (and what China has). It cannot do without those things. But Russia (and China) can do without what Europe has. They are self-sufficient. The financial impact of European sanctions on Russia is minimal. Therefore, economic sanctions against Russia (or China) will never work. But, because of the overwhelming dependence of Europe on Russian (and Chinese) goods, sanctions on Russia (or China) will utterly destroy Europe. The only hope for Europe to prevent a total economic catastrophe is to achieve an agreement with Russia that ends the current destructive sanctions as soon as possible, and at whatever political cost, including the abandonment of Ukraine and cession of Ukrainian territory to Russia. The longer this is postponed, the more extensive the permanent economic damage to Europe will be….

‘A New World Order is taking birth before our eyes….

Commenting on the banking system, precious metals businessman Stefan Gleason warns that ‘The global fractional-reserve banking system is teetering on the brink of failure. Financial strains are exposing major banks as under-capitalized and ill prepared to weather additional strains from high inflation, rising interest rates, and a weakening economy. Banks operating outside the United States are presently most vulnerable. A spike in interest rates concomitant with a spike in the exchange rate of the Federal Reserve note “dollar” is wreaking havoc in global debt markets and driving capital flight. Many analysts fear bank runs are coming. They are already hitting developing countries.’ See ‘Banks on the Brink: Is Your Money Safe?’

Noting that imposition of technologies associated with the fourth industrial revolution and the war in Ukraine are impacting the labor force, among a wide variety of other impacts on society as a whole, ‘Winter Oak’ observes that while anticipating future employment trends is not easy, ‘the combined threat of pandemics and wars means the labour force is on the brink of an unprecedented reshuffle with technology reshaping logistics, potentially threatening hundreds of millions of blue and white collar jobs, resulting in the greatest and fastest displacement of jobs in history and foreshadowing a labour market shift which was previously inconceivable.’

Furthermore: the nation state model is being upended ‘by a global technocracy, consisting of an unelected consortium of leaders of industry, central banking oligarchs and private financial institutions, most of which are predominantly non-state corporate actors attempting to restructure global governance and enlist themselves in the global decision-making process.’ See ‘The Great Reset Phase 2: War’.

James Corbett simply observes that ‘the financial order we have known our whole lives is slated for destruction’. The demolition of the economy provides cover to conceal implementation of other key elements of the elite plan in which all fit neatly together: ‘vaccine passports introduce the digital ID. The digital ID provides the infrastructure for the CBDCs. The CBDCs provide a mechanism for enforcement of a social credit system.’ As Corbett notes: ‘To see these events as separate events unfolding haphazardly and coincidentally is to miss the entire point.’ See ‘The Controlled Demolition of the Economy’.

And, according to a source cited by Anviksha Patel, executives at the giant hedge-fund firm Elliott Management Corp. recently sent a letter to investors advising that the world is ‘on the path to hyperinflation’ which could lead to ‘global societal collapse and civil or international strife’. See ‘Hedge-fund giant Elliott warns looming hyperinflation could lead to “global societal collapse”’.

Among many other commentaries offering insight into one or more aspects of what is happening, Oxfam documents the fact that ‘billionaires in the food and energy sectors are increasing their fortunes by $1 billion dollars every two days’ and that a new billionaire is being created every 30 hours while nearly a million people are being pushed into extreme poverty at nearly the same rate. See ‘Pandemic creates new billionaire every 30 hours – now a million people could fall into extreme poverty at same rate in 2022’.

But perhaps the most evocative account of what is transpiring is offered by Egon von Greyerz, founder and managing partner of Matterhorn Asset Management in Switzerland, a company that has ‘always held a deep respect for analysing and managing risk’: By the end of the 1990s, it was clear ‘that global [financial] risk was growing increasingly apparent as debts and derivative levels rapidly rose’. See Matterhorn Asset Management: History.

Noting that laws governing the functioning of modern economies ensure that ‘No banker, no company management or business owner ever has to take the loss personally if he makes a mistake. Losses are socialised and profits are capitalised. Heads I win, Tails I don’t lose!’ Greyerz goes on to note that ‘there are honourable exceptions.’ Some Swiss banks still operate in accordance with the principle of unlimited personal liability for the partners/owners which clearly encourages a responsible, ethical approach to the conduct of business.

He observes: ‘If the global financial system and governments applied that principle, imagine how different the world would look not just financially but also ethically.’ If we had such a system, he contends, then human values would come before adoration of ‘the golden calf’. And evaluation of an investment proposal or a loan would be based on a judgment about its soundness economically and ethically, as well as a judgment that the risk of loss was minimal, rather than just the size of the personal profit it might return.

Instead, since 1971 (when President Nixon unilaterally terminated convertibility of the US dollar into gold, effectively ending the 1944 Bretton Woods system) ‘governments and central banks have contributed to the creation of almost $300 trillion of new money plus quasi money in the form of unfunded liabilities and derivatives [‘the most dangerous and aggressive financial instrument of destruction’] of $2.2 quadrillion making $2.5 [quadrillion] in total. As debt explodes, the world could easily face a debt burden of $3 quadrillion by 2025-2030.’ At the same time, ‘Central banks around the world hold $2 trillion [in gold reserves].’

The outcome is inevitable: ‘with over $2 quadrillion (2 and 15 zeros) of debt and liabilities resting on a foundation of $2 trillion of government-owned gold that makes a gold coverage of 0.1% or a leverage of 1000X!… an inverse pyramid with a very weak foundation.’ Noting that a sound financial system ‘needs a very solid foundation of real money’ it is simply the case that quadrillions of debt and liabilities ‘can not survive resting on this feeble amount of gold. So the $2 quadrillion financial weapon of mass destruction is now on the way to totally destroy the system. This is a global house of cards that will collapse at some point in the not too distant future…. No government and no central bank can solve the problem that they have created. More of the same just won’t work.’ See ‘$2 Quadrillion Debt Precariously Resting on $2 Trillion Gold’.

The fundamental summary then, according to Greyerz, is this: ‘This system will start to implode.’… ‘The whole banking system is rotten. With the problems in Europe now it is actually a critical situation…. We have a two tier economy:… the rich are still rich but the poor are really poor. And you see that in every country in the world now… People haven’t got enough money to live…. This is going to be a human disaster of major proportions: it’s so sad and governments will not have any chance of doing anything about it.’ In the US outside the metropolitan areas, ‘the poverty is incredibly high and people live in boxes… poverty is everywhere and sadly, we are only seeing the beginning and there is no solution…. From a human point of view, we are looking at a major disaster.’ Watch ‘$2.5 Quadrillion Disaster Waiting to Happen’.

Will action be taken to halt the collapse? According to alternative economist Brandon Smith, it won’t. Consider this: ‘What if the goal of the Fed is the destruction of the middle class?… What if they are luring investors into markets with rumors of a pivot, tricking those investors into pumping money back into markets and then triggering losses yet again with more rate hikes and hawkish language? What if this is a wealth destruction steam valve? What if it’s a trap? I present this idea because we have seen this before in the US, from 1929 through the 1930s during the Great Depression. The Fed used very similar tactics to systematically destroy middle class wealth and consolidate power for the international banking elites.’

And that, of course, is the point: the crash has been engineered. Why?

In summarizing the ongoing collapse of European infrastructure and industry, and energy shortages in the USA, Mike Adams notes that the ‘globalists are decimating the pillars of civilization in order to cause collapse and depopulation…. The overarching goal is to exterminate the vast majority of the human population, then enslave the survivors.’ See ‘Dark Times: Industry and infrastructure collapsing by the day across Europe and the USA’.

But this is no surprise. All that any thoughtful observer needs to do is consider history, listen to what the Global Elite is telling us they are doing, observe them doing it, and then simply inform people what is at hand: The destruction of the global economy, as part of the fundamental reshaping of world order.

After all, the Elite has been crystal clear. It’s fundamental aim is to kill off a substantial proportion of the human population and reduce those humans and transhumans left alive to slavery while confined in their technocratic prison; even wealth concentration is anciliary to that, although a product of it. See ‘The Elite Coup to Kill or Enslave Us: Why Can’t Governments, Legal Actions and Protests Stop Them?’ And if you crash the global economy denying people regular food, energy to stay warm and the capacity to communicate effectively, most of those left alive will be inclined to submit to whatever conditions they are offered in order to survive. How bad does your technocratic prison sound now? Even if you are eating insects?

So, to reiterate a vital point, the Elite agenda in relation to the economy is intimately related to its wider agenda in relation to eugenics and technocracy.

How will this happen? While it will obviously require several of the range of measures being introduced, particularly including the deployment of 5G, the digitization of your identity and the utilization of a range of other technologies such as artificial intelligence and geofencing, here is what Clive Thompson, retired Managing Director of Union Bancaire Privée in Switzerland, believes might happen:

‘I think its quite likely that the CBDC will arrive and it will also be the subject of the currency reset at the same time. At some point the world is going to go into a crisis or a country is going to go into a crisis…. When that happens I think they will close the banks, you will wake up on a Sunday morning and hear the news that they’ve shut the banks, they’re not going to open on Monday. Then by Monday evening or Tuesday you’ll get the announcement that we’re having a new currency – the CBDC – and don’t worry it will be one-to-one against the old currency but there will be some restrictions on your ability to convert your old money into the new money.

‘So if you’re poor and you have a small bank account it will be converted one-to-one straight away, and you’ll probably even find that you get a free gift from the government to kickstart the system, maybe three or five thousand pounds will be given to every citizen gratuitiously to kickstart the new system to the new CBDC. But if you have a hundred thousand or a million in the bank you’re going to be told ‘Yes, it’s one-to-one but you’re going to have to wait to convert it to the new currency.’ Now “wait” means “never”, we all know that. But they won’t tell you that. They’ll say it’s a temporary suspension because we’re in the middle of a crisis, the people are rioting in the street, we need to calm the system so ‘Here’s some free money everybody, go and enjoy yourselves.’…

‘So I think the CBDC will arrive as a consequence of a crisis and when that happens there will be a limitation on how much of your old currency you can convert, at one-to-one, with the new one…. But the advantage of this, from the government’s point of view, is it’s to all intents and purposes wiping the slate clean because all their liabilities will be denominated in a currency that nobody can use, nobody can spend.’ Watch ‘The Currency Reset Will Wipe Out Creditors and Usher in CBDCs. Part 1’.

In preparing to cope with the disruption this must inevitably cause, among other assets that would be critically useful while retaining value, such as open-pollinated (non-hybrid) seeds, Thompson suggests gold and silver (including gold and silver coins), land, property, equities, collectibles (such as art and rarer coins), machine and other tools, electricity generators, useful items, animals, firewood, washing powder, canned food and house extensions. See ‘The Currency Reset Will Wipe Out Creditors and Usher in CBDCs. Part 2.’

Of course, Thompson might be wrong in his prediction of precisely how the technocratic state will ultimately be imposed. But imposed it will be, one way or another, unless we are effectively resisting the foundational components of the Elite program.

Is cryptocurrency part of the answer?

Many people are suggesting cryptocurrencies as one way around some of the problems we face. However, the very basis of sound economy for any world that is unfolding is self-reliance, particularly in relation to essential needs around food, water, clothing, shelter and energy, within a local, sustainable community that is as self-sufficient as possible, and able to nonviolently defend itself.

Complemented by use of local markets and trading schemes – whether using local currencies or goods and services directly – this will maximise economic survival prospects for those participating (and no doubt some others besides).

And unless a currency is backed by something with genuine value – as currencies were backed by gold or other metals in earlier eras – or there is widespread confidence in a currency for another reason (as currencies around the world have been backed by their governments until now), it can become valueless very quickly.

But for an extremely succinct warning against crypto, check out this brief statement from Catherine Austin Fitts: ‘If you move to crypto, and I just want to really underscore this, crypto is not a currency, it is a control system.’ See ‘The Dangers Of Cryptocurrencies’.

For another of the many critiques of crypto, see retired corporate accountant Lawrence A. Stellato’s ‘The Dangers of Cryptocurrencies’.

Crypto has a high environmental cost too, given the technology it uses and the energy it needs to run.

In essence: Just not part of the future we must work together to build.

The Rothschilds and Transhumanism

Before concluding this investigation, it is worth returning to consideration of the Rothschild family in relation to one final issue: Transhumanism.

Why is this important?

Throughout this investigation, I have endeavoured to document a few basic facts: The Global Elite is intent on reshaping world order by killing off a substantial proportion of the human population and enslaving those left alive as transhuman slaves imprisoned in ‘smart’ cities. As part of achieving this outcome, the global economy is being ransacked and destroyed: This is intended to deprive people of the sustenance necessary to resist the entire Elite program that, among other outcomes, will concentrate virtually all remaining wealth in Elite hands.

This program has been planned in detail by elite agents in organizations like the World Economic Forum and the World Health Organization and is being implemented by relevant international organizations and multinational corporations (particularly those in the pharmaceutical and biotechnology industries, and the corporate media), as well as national governments and medical organizations.

But, as I have pointed out, every organization, corporation and government is composed of individual human beings who make decisions (consciously or unconsciously) about what they do in any given circumstance. And while structural power is not something that can be ignored, individuals do have agency.

To illustrate this point, I have used the House of Rothschild as one example of a family of individuals who make decisions about how to act in the world and how the decisions of this family exercise enormous influence over world events. Consider another brief example of the decisions made by Rothschild family members and what has transpired as a result.

The Rothschild influence over world banking and the global economy, and thus political systems, is heavily documented and illustrated above. So, given the current Elite push to substantially reduce the human population and introduce a technocratic state populated by transhuman slaves, one question that inevitably suggests itself as worthy of further investigation concerns the possible involvement of the Rothschilds in the research and development of the technologies and biotechnologies that make this all possible.

An investigation soon reveals that Nathaniel Mayer Victor Rothschild, the 3rd Baron Rothschild, was born in 1910 and attended Trinity College, Cambridge, where he read physiology, later gaining a PhD. After working for MI5 during World War II, ‘he joined the zoology department at Cambridge University from 1950 to 1970. He served as chairman of the Agricultural Research Council from 1948 to 1958 and as worldwide head of research at Royal Dutch/Shell [as noted above, a family business] from 1963 to 1970.’ See ‘Victor Rothschild, 3rd Baron Rothschild’.

Beyond this, however, articles in ‘The Financial Times’ in 1982-1983 reveal that N.M. Rothschild, of which the biologist Lord Rothschild was head, had established a venture capital fund called Biotechnology Investments in 1981 to attract £25m investments for biotechnology research. However, the fund, registered in the tax haven of Guernsey, had such exacting scientific and financial standards that it was having trouble identifying companies that could meet those standards despite the rapidly growing field. According to one news report in 1982: ‘City [of London] estimates put the number of new technology companies established in the last five years at about 150, mostly in North America. At least 70 are practising genetic engineering.’ See ‘Newsclippings re. Biotechnology Investments Limited (BIL) owned by N.M. Rothschild Asset Management’.

But lest you are concerned that the Rothschilds failed to establish a firm foothold in this fledgling industry, you might be reassured, but no wiser, to read the entry on the CHSL Archives Repository (that focuses on ‘Preserving and promoting the history of molecular biology’) titled ‘Rothschild Asset Management – Rothschild, Lord Victor’.

You will be no wiser because the archive is marked ‘Closed until Jan 2045 – Suppress all images for 60 years’.

As it turns out, however, the Rothschilds, whose business acumen is never questioned, are still raising funds and investing heavily in biotechnology. See ‘Edmond de Rothschild private equity unit to invest in biotech’. It’s just that, as usual, while you are hearing from elite agents (such as Klaus Schwab, Yuval Noah Harari and Elon Musk) who publicly promote transhumanist endeavours, you are hearing very little from those, like the Rothschilds, who prefer control and profit to publicity.

Consequently, the Rothschilds are playing a key role both in the ongoing ransacking of the global economy and in profiting from the control they are helping to make possible through introduction of transhumanist technologies. It goes without saying that the family has heavy investments in many other technologies too, including those that will be critical to the success of the imminent technocratic world order, such as the Internet of Things. See, for example, Rothschild Technology Limited.

Because it controls the political, economic, financial, technological, medical, educational, media and other important levers of society, the Elite profits hugely from daily human activity. But it can also precipitate an ‘extreme event’ (or the delusion of one) – a war, financial crisis (including depression), revolution, ‘natural disaster’, ‘pandemic’ (if you think that the Covid-19 scam was the last of its kind, see ‘Who’s Driving the Pandemic Express?’ and watch the plan for the next one, already available: ‘Catastrophic Contagion’) – and use its control of the political, economic, technological and other levers mentioned to manage how events unfold while simultaneously managing the narrative about what is taking place so that the truth is concealed.

This means that the Elite’s killing and exploitation of the human population at large is hidden behind whatever ‘enemy’ (human or otherwise) that Elite agents in government and the media direct the attention of the public towards at any given time.

It doesn’t matter whether we all end up blaming Hitler, Saddam or ‘the Russians’, ‘the capitalists’ or ‘Wall Street’, ‘the government’, ‘the climate’ or ‘the virus’, we never blame the Elite. So we never take action that is focused on stopping those individuals and their corporations and institutions that are fundamentally responsible for inflicting unending harm on us all, as well as the Earth and all of its other creatures too.

Fortunately, while the Elite is adept at devising an ever-expanding range of tools that can be used to manipulate events while simultaneously concealing this behind a barrage of propaganda, there is still just enough time to finally recognize what is happening and to end it. Otherwise, just as in the board game ‘Monopoly’, where one player finally owns everything and the other players have been forced out of the game, the Elite will win the ‘final battle’ against humanity, capture all wealth and reduce those humans and transhumans left alive to the status of slaves. See ‘The Final Battle for Humanity: It is “Now or Never” in the Long War Against Homo Sapiens’.

But just because someone is insane and their plan is insane, it doesn’t mean they cannot succeed. Remember Adolf Hitler? Idi Amin in Uganda? Pol Pot in Cambodia? Insane violence of unspeakable magnitude can succeed if too many people either cannot perceive the insanity, are afraid of it or simply believe it is too preposterous – ‘It can’t be true.’ – and do nothing about it. Or, in the cases just mentioned, not until it was too late to prevent vast killing.

So here is the summary: Humanity faces the gravest threat in our history. But because our opponent – the Global Elite – is insane, we cannot rely on reason or thoughtfulness alone to get us out of this mess: You cannot reason with insanity. And because the Global Elite controls international and national political processes, the global economy and legal systems, efforts to seek redress through those channels must fail. See ‘The Elite Coup to Kill or Enslave Us: Why Can’t Governments, Legal Actions and Protests Stop Them?’

Hence, if we are going to defeat this long-planned, complex and multifaceted threat, we must defeat its foundational components, not delude ourselves that we can defeat it one threat at a time or even by choosing those threats we think are the worst and addressing those first.

This is because the elite program, whatever its flaws and inconsistencies, as well as its potential for technological failure at times, is deeply integrated so we must direct our efforts at preventing or halting those foundational components of it that make everything else possible. This is why random acts of resistance will achieve nothing. Effective resistance requires the focused exercise of our power. In simple terms, we must be ‘strategic’.

If you are interested in being strategic in your resistance to the ‘Great Reset’ and its related agendas, you are welcome to participate in the ‘We Are Human, We Are Free’ campaign which identifies a list of 30 strategic goals for doing so.

In addition and more simply, you can download the one-page flyer that identifies a short series of crucial nonviolent actions that anyone can take. This flyer, recently updated and now available in 23 languages (Chinese, Croatian, Czech, Danish, Dutch, English, Finnish, French, German, Greek, Hebrew, Hungarian, Italian, Japanese, Malay, Polish, Portuguese, Romanian, Russian, Serbian, Spanish, Slovak and Turkish) with several more languages in the pipeline, can be downloaded from here: ‘One-page Flyer’.

If this strategic resistance to the ‘Great Reset’ (and related agendas) appeals to you, consider joining the ‘We Are Human, We Are Free’ Telegram group (with a link accessible from the website).

And if you want to organize a mass mobilization, such as a rally, at least make sure that one or more of any team of organizers and/or speakers is responsible for inviting people to participate in this campaign and that some people at the event are designated to hand out the one-page flyer about the campaign.

If you like, you can also watch, share and/or organize to show, a short video about the campaign here: ‘We Are Human, We Are Free’ video.

In parallel with our resistance, we must create the political, economic and social structures that serve our needs, not those of the Elite. That is why long-standing efforts to encourage and support people to grow their own food, participate in local trading schemes (involving the exchange of knowledge, skills, services and products with or without a local medium of exchange) and develop structures for cooperation, governance, nonviolent defence and networking with other communities are so important. Of course, indigenous peoples still have many of these capacities – lost to vast numbers of humans as civilization has expanded over the past five millennia – but many people are now engaged in renewed efforts to create local communities, such as ecovillages, and local trading schemes, such as Community Exchange Systems. Obviously, we must initiate/expand these forms of individual and community engagement in city neighbourhoods too.

Moreover, as Catherine Austin Fitts reminds us, if we choose that option, there is nothing to stop us having our own decentralised money system, starting with our own local community central bank and our own local community currency. Watch ‘We Need to Talk about Mr Global – Part Two’.

Finally, as noted by Professor Carroll Quigley in the very last words of his nearly-1,000 page epic Tragedy & Hope:

‘Some things we clearly do not yet know, including the most important of all, which is how to bring up children to form them into mature, responsible adults.’ See Tragedy & Hope: A History of the World in Our Time, p. 947.

Fortunately, the passage of time since Quigley wrote these words has revealed an answer to this challenge. So, if you want to raise children who are powerfully able to investigate, analyze and act, you are welcome to make ‘My Promise to Children’.

Conclusion

Since the dawn of human civilization 5,000 years ago, in one context after another, some people who are more terrified than others in their immediate vicinity have sought what they perceived to be increased personal ‘security’ by gaining and exercising greater control over the people and resources around them.

Progressively, over time, this serious psychological dysfunctionality has been compounding until, today, the degree of ‘security’ and control that some people require includes all of us and all of the world’s resources. For want of a better term, we might call them the ‘Global Elite’ but it is important to understand that they are insane, criminal and ruthlessly violent.

This takeover of all of us and everything on Planet Earth is currently being attempted by this Elite through the ‘Great Reset’ and its related fourth industrial revolution, eugenicist and transhumanist agendas.

In essence, the intention is to kill off a substantial proportion of us, as is now happening, enclose the commons forever (and force those who live in regional areas off the land) while imprisoning those left alive as transhuman slaves in their technocratic ‘smart cities’ where we will ‘own nothing’ but provide the compliant workforce necessary to serve Elite ends.

Whether wars or financial crises (including depressions), ‘natural disasters’, revolutions or ‘pandemics’, great events are contrived by the Elite to distract attention from and facilitate profound changes in world order and obscure vast transfers of wealth from ordinary people to this Elite.

And this is done with the active complicity of Elite agents – including international organizations such as the United Nations, national governments and legal systems – which is why redress cannot be found through mainstream political or legal channels.

However, distracted by an endless stream of irrelevant ‘news’, superficial debates such as capitalism vs. socialism, monarchy vs. democracy, this political party vs. that political party, or even which football team is better, virtually all people are oblivious to how the world really works and who is orchestrating how history will be written by elite agents.

Is there conflict between individuals, families and groups within the Elite? Of course! But unlike the conflicts they endlessly throw in our faces to distract and manipulate us, the unifying agenda to which they all subscribe is to perpetually restructure world order to expand Elite control and extract more wealth for Elites. 5,000 years of human history categorically demonstrates that point.

Hence, if humanity is to defeat this Elite program, we must do it ourselves.

And if you want your resistance to this carefully-planned Elite technocratic takeover to be effective, then it must be strategic. Otherwise, your death or technocratic enslavement is now imminent.

I thank Anita McKone for thoughtful suggestions to improve the original draft of this investigation.

Robert J. Burrowes has a lifetime commitment to understanding and ending human violence. He has done extensive research since 1966 in an effort to understand why human beings are violent and has been a nonviolent activist since 1981. He is the author of ‘Why Violence?’ His email address is flametree@riseup.net and his website is here. He is a regular contributor to Global Research.

Crypto is finally interesting with the collapse of FTX exposing a political network. These were no seaside Millennials building sand-castles with other people’s money. The justly-named Sam Bankman-Fried was the second biggest donor in the midterms.

The firm crashed last week when depositors tried to withdraw $6 billion. As the money’s been used to fund derivative bets, it may have a knock-on effect. This is no simple Ponzi or trading fraud as the press is pretending.

The setup is spooky from its connections, timings and complexity, to the firms’ logos. It bears an uncanny resemblance to the upscale Theranos viral testing fraud. A crypto pioneer warns of an intelligence sex trafficking ring and promptly drowns.

Individual parts of the story, while suggestive of corruption or wrongdoing, do not tell of the sheer extent of collusion, or the span of this network. For that you need a lofty perspective.

To begin in a spirit of caution, let’s start with a post on one of the Reddit crypto threads: “So much of this FTX meltdown has been connected to various braindead conspiracy theory bullshit at this point. I don’t like the WEF, but this is neither surprising nor consequential to me and I’m highly suspicious of anyone who is suddenly shouting, I knew it! This goes all the way to the top!”

The individual, one g_squidman, says there is no reason to assume Ukrainian officials were siphoning aid money into black money markets; that FTX being located in a tax haven is a “Panama Papers type of conspiracy”; that the crisis serves as a pretext to destroy crypto; that the media lionized FTX out of nowhere; or that its connection to top financial watchdogs might mean it was somehow a deep state project.

“There’s no global deepstate that appointed FTX with the responsibility to make you eat bugs.”

There you have the classic conflation of issues intended to ridicule anyone asking questions. Often there’s a mention of the Moon landings, though not this time.

It was just one greedy billionaire stealing other people’s money — nothing to see. That is what the state corporate media said about Jeffrey Epstein: that it was just one greedy billionaire feeding his sex addiction.

Behind the screen

However this Reditor’s tone of the “only adult in the room” betrays a poor appreciation for how the media or politics works. Neither grants easy access. It is rationed — that is the source of its power. You do not gain publicity or political connections overnight as did Sam Bankman-Fried. By the way, I will hereinafter call him Sam, for the SBF acronym is too reminiscent of Saudi Arabia’s MBS, who has genuine wealth and power.

Look at his family connections plastered across Twitter. Did Sam’s sudden prominence generate those connections or is it the other way around — those connections were behind his rise?

We have watched for three years as events and personages emerge, as from behind a screen, taking their place in ongoing events, like an actor opening the next scene. Much of this cast enriches a narrative or an operation that’s already underway, and they advance rather than hinder its objectives.

As somone once said, if events were random, wouldn’t the little guy win just once in a while?

It does go to show how tiny a world it is — money going to Ukraine’s government, which employs FTX, a new broker loudly promoted by the corporate media and the World Economic Forum, that same broker donating to the Democratic Party and that funds research to bash Ivermectin and promote pandemics; a broker launched by two recent graduates, whose parents work with key government regulators — but it’s not a world that you or I could enter with ease. [1]

People follow celebrities so closely that they mistake them for friends: those on the screen slap each other on the back and share coffee; we imagine ourselves joining in.

Likewise followers of the crypto space — in which Sam is a celebrity if only for his notoriety — can fall for the illusion. His trademark tousled hair and cargo shorts add to the familiarity. Yet that should be a warning (not proof, of course) that he was cast for the role.

Every time a tech entrepreneur dons a black tennis shirt it seems they’re trying to sell something — because they are! They are the sales jocks pushed to the front. The world stage has only just seen the back of tousled Boris Johnson. Tousled Trudeau is still smarming his charm.

The team

To cut to the chase, Mark Wetjen has been FTX head of policy and regulatory strategy since Nov 2021. He served as Commodity Futures Trading Commissioner under President Barack Obama from 2011. He was deputy to the Gary Gensler, until the latter became Securities and Exchange Commisioner.

If the penny hasn’t dropped: how could the government not have known that FTX was a fraud for at least a year?

Sam met Gensler at the SEC several times over regulatory issues — perhaps linked to FTX’s acquisition of U.S.-based crypto lender BlockFi, which already had the regulatory approval, to see if this could be extended as an umbrella to cover FTX.

No evidence has emerged that Gensler did anything wrong — actually he has a reputation for slow-walking a regulatory framework that would encourage the crypto industry.

The U.S. is inconsistent in its regulation of crypto exchanges, banning in particular those it considers anonymous. While authorities do not recognize crypto as legal tender, they regard it as a value transaction and thus subject to tax.

Then, in early 2022, Sam met the chairman of the Federal Reserve.

A FOIA request shows that around midday on Feb 1, 2022, Federal Reserve Chairman Jerome Powell was scheduled to meet with: Sam Bankman-Fried, CEO and founder, Brett Harrison, president, Ryne Miller, general counsel, and Mark Wetjen, head of policy and regulatory strategy, FTX US and Zach Dexter, CEO, FTX US Derivatives. [2]