By Brandon Smith

Source: Alt-Market.us

In my 16 years as an alternative economist and political writer I have spent around half that time warning that the ultimate outcome of the Federal Reserve’s stimulus model would be a stagflationary collapse. Not a deflationary collapse, or an inflationary collapse, but a stagflationary collapse. The reasons for this were very specific – Mass debt creation was being countered with MORE debt creation while many central banks have been simultaneously devaluing their currencies through QE measures. On top of that, the US is in the unique position of relying on the world reserve status of the dollar and that status is diminishing.

It was only a matter of time before the to forces of deflation and inflation met in the middle to create stagflation. In my article ‘Infrastructure Bills Do Not Lead To Recovery, Only Increased Federal Control’, published in April of 2021, I stated that:

“Production of fiat money is not the same as real production within the economy… Trillions of dollars in public works programs might create more jobs, but it will also inflate prices as the dollar goes into decline. So, unless wages are adjusted constantly according to price increases, people will have jobs, but still won’t be able to afford a comfortable standard of living. This leads to stagflation, in which prices continue to rise while wages and consumption stagnate.

Another Catch-22 to consider is that if inflation becomes rampant, the Federal Reserve may be compelled (or claim they are compelled) to raise interest rates significantly in a short span of time. This means an immediate slowdown in the flow of overnight loans to major banks, an immediate slowdown in loans to large and small businesses, an immediate crash in credit options for consumers, and an overall crash in consumer spending. You might recognize this as the recipe that created the 1981-1982 recession, the third-worst in the 20th century.

In other words, the choice is stagflation, or deflationary depression.”

It’s clear today what the Fed has chosen. It’s important to remember that throughout 2020 and 2021 the mainstream media, the central bank and most government officials were telling the public that inflation was “transitory.” Suddenly in the past few months this has changed and now even Janet Yellen has admitted that she was “wrong” on inflation. This is a misdirection, however, because the Fed knows exactly what it is doing and always has. Yellen denied reality, but she knew she was denying reality. In other words, she was not mistaken about the economic crisis, she lied about it.

As I outlined last December in my article ‘The Fed’s Catch-22 Taper Is A Weapon, Not A Policy Error’:

‘First and foremost, no, the Fed is not motivated by profits, at least not primarily. The Fed is able to print wealth at will, they don’t care about profits – They care about power and centralization. Would they sacrifice “the golden goose” of US markets in order to gain more power and full bore globalism? Absolutely. Would central bankers sacrifice the dollar and blow up the Fed as an institution in order to force a global currency system on the masses? There is no doubt; they’ve put the US economy at risk in the past in order to get more centralization.’

The Fed has known for years that the current path would lead to inflation and then market destruction, and here’s the proof – Fed Chairman Jerome Powell actually warned about this exact outcome in October of 2012:

“I have concerns about more purchases. As others have pointed out, the dealer community is now assuming close to a $4 trillion balance sheet and purchases through the first quarter of 2014. I admit that is a much stronger reaction than I anticipated, and I am uncomfortable with it for a couple of reasons.First, the question, why stop at $4 trillion? The market in most cases will cheer us for doing more. It will never be enough for the market. Our models will always tell us that we are helping the economy, and I will probably always feel that those benefits are overestimated. And we will be able to tell ourselves that market function is not impaired and that inflation expectations are under control. What is to stop us, other than much faster economic growth, which it is probably not in our power to produce?

When it is time for us to sell, or even to stop buying, the response could be quite strong; there is every reason to expect a strong response. So there are a couple of ways to look at it. It is about $1.2 trillion in sales; you take 60 months, you get about $20 billion a month. That is a very doable thing, it sounds like, in a market where the norm by the middle of next year is $80 billion a month. Another way to look at it, though, is that it’s not so much the sale, the duration; it’s also unloading our short volatility position.”

As we all now know, the Fed waited until their balance sheet was far larger and until the economy was MUCH weaker than it was in 2012 to unleash tightening measures. They KNEW the whole time exactly what was going to happen.

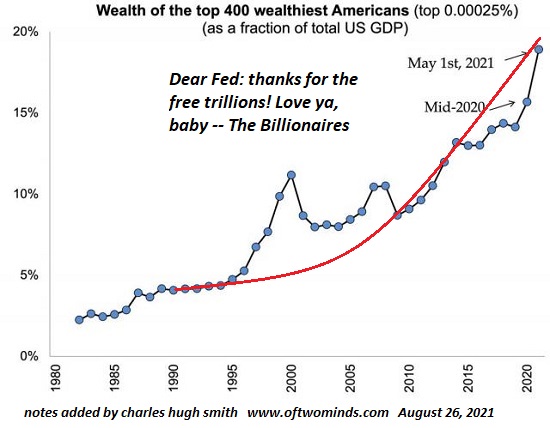

It is no coincidence that the culmination of the Fed’s stimulus bonanza has arrived right after the incredible damage done to the economy and the global supply chain by the covid lockdowns. It is no coincidence that these two events work together to create the perfect stagflationary scenario. And, it’s no coincidence that the only people who benefit from these conditions are proponents of the “Great Reset” ideology at the World Economic Forum and other globalist institutions. This is an engineered collapse that has been in the works for many years.

The goal is to “reset” the world, to erase what’s left of free market systems, and to establish what they call the “Shared Economy” system. This system is one in which the people who survive the crash will be made utterly dependent on government through Universal Basic Income and one that will restrict all resource usage in the name of “carbon reduction.” According to the WEF, you will own nothing and you will like it.

The collapse is engineered to create crisis conditions so frightening that they expect the majority of the public to submit to a collectivist hive mind lifestyle with greatly reduced standards. This would be accomplished through UBI, digital currency models, carbon taxation, population reduction, rationing of all commodities and a social credit system. The goal, in other words, is complete control through technocratic authoritarianism.

All of this is dependent on the exploitation of crisis events to create fear in the population. Now that economic destabilization has arrived, what happens next? Here are my predictions…

The Fed Will Hike Interest Rates More Than Expected, But Not Enough To Stop Inflation

Today, we are witnessing the poisonous fruits of a decade-plus of massive fiat money creation and we are now at the stage where the Fed will reveal its true plan. Hiking interest rates fast, or hiking them slow. Fast hikes will mean an almost immediate crash in markets (beyond what we have already seen), slow hikes will mean a drawn out process of price inflation and general uncertainty.

I believe the Fed will hike more than expected, but not enough to actually slow inflation in necessities. There will be an overall decline in luxury items, recreation commerce and non-essentials, but most other goods will continue to climb in cost. It is to the advantage of globalists to keep the inflation train running for another year or longer.

In the end, though, the central bank WILL declare that the pace of interest rates is not enough to stop inflation and they will revert to a Volcker-like strategy, pushing rates up so high that the economy simply stops functioning altogether.

Markets Will Crash And Unemployment Will Abruptly Spike

Stock markets are utterly dependent on Fed stimulus and easy money through low interest rate loans – This is a fact. Without low rates and QE, corporations cannot engage in stock buybacks. Meaning, the tools for artificially inflating equities are disappearing. We are already seeing the effects of this now with markets dropping 20% or more.

The Fed will not capitulate. They will continue to hike regardless of the market reaction.

As far as jobs are concerned, Biden and many mainstream economists constantly applaud the low unemployment rate as proof that the American economy is “strong,” but this is an illusion. Covid stimulus measures temporarily created a dynamic in which businesses needed increased staff to deal with excess retail spending. Now, the covid checks have stopped and Americans have maxed out their credit cards. There is nothing left to keep the system afloat.

Businesses will start making large job cuts throughout the last half of 2022.

Price Controls

I have no doubt that Joe Biden and Democrats will seek to enforce price controls on many goods as inflation continues, and there will be a handful of Republicans that will support the tactic. Price controls actually lead to a reduction in supply because they remove all profits and thus all incentive for manufacturers to keep producing goods. What usually happens at that point is government steps in to nationalize manufacturing, but this will be substandard production and at a much lower yield.

In the end, supplies are reduced even further and prices go even higher on the black market because no one can get their hands on most goods anyway.

Rationing

Yes, rationing at the manufacturing and distribution level is going to happen, so be sure to buy what you need now before it does. Rationing occurs in the wake of price controls or supply chain disruptions, and usually this coincides with a government propaganda campaign against “hoarders.”

They will hold up a few exaggerated examples of people who buy truckloads of merchandise to scalp prices on the black market. Then, not long after, they will accuse preppers and anyone who bought goods BEFORE the crisis of “hoarding” simply because they planned ahead.

Rationing is not only about controlling the supply of necessities and thus controlling the population by proxy; it is also about creating an atmosphere of blame and suspicion within the public and getting them to snitch on or attack anyone that is prepared. Prepared people represent a threat to the establishment, so expect to be demonized in the media and organize with other prepared people to protect yourself.

Be Ready, It Only Gets Worse From Here On

It might sound like I am predicting success of the Great Reset program, but I actually believe the globalists will fail in the end. That’s not going to stop them from making the attempt. Also, the above scenarios are only predictions for the near term (within the next couple of years). There will be many other problems that stem from these situations.

Naturally, food riots and other mob actions will become more commonplace, perhaps not this year, but by the end of 2023 they will definitely be a problem. This will coincide with the return of political unrest in the US as leftist factions, encouraged by globalist foundations, demand more government intervention in poverty. At the same time, conservatives will demand less government interference and less tyranny.

At bottom, the people who are prepared might be called a lot of mean names, but as long as we organize and work together, we will survive. Many unprepared people will NOT survive. Understand that the economic conditions ahead of us are historically destructive; there is no way that serious consequences can be avoided for a large part of the population, if only because they refuse to listen and to take proper steps to protect themselves.

The denial is over. The crash is here. Time to take action if you have not done so already.