Does anyone really believe that the renunciation of massive, sustained stimulus of speculation in housing would leave housing valuations unchanged because valuations are solely the result of “shortages”?

Let’s begin by stipulating that speculation (i.e. gambling) is part of human nature. The role of regulations and policy is to limit the damage that gambling inevitably inflicts when “sure things” cliff-dive into losses.

In other words, where the speculative frenzy and money flows matters. When the South Sea Bubble expanded circa 1713-1720, this flood tide of speculative capital did not distort the cost of shelter and bread in England; it was limited to a purely financial marketplace of shares in the company. When the bubble imploded in 1720, the losses fell mostly on wealthy investors like Isaac Newton.

The same can be said of the speculative mania of the dot-com era: the bubble and collapse were limited to the tech sector and those participating in the sector and the speculative frenzy. The cost of rent and bread did not double due to the speculative bubble’s inflation or bursting.

In contrast, when speculation floods into shelter / housing, it fatally distorts the cost of housing non-speculators must pay. I say fatally because shelter, along with food, energy and water (the FEW resources), are essential to life. These are not discretionary things we can decide not to have. When the price of essentials soars due to speculation that only rewards the speculators at the expense of non-speculators, the fuse of social disorder is lit.

Anyone who believes policies that encourage the wealthy to hoard housing to the point that the bottom 80% (or the bottom 95% in some areas) cannot afford to buy a home are just peachy is overdosing Delusionol. The social consequences are severe and uncontainable once the worm turns.

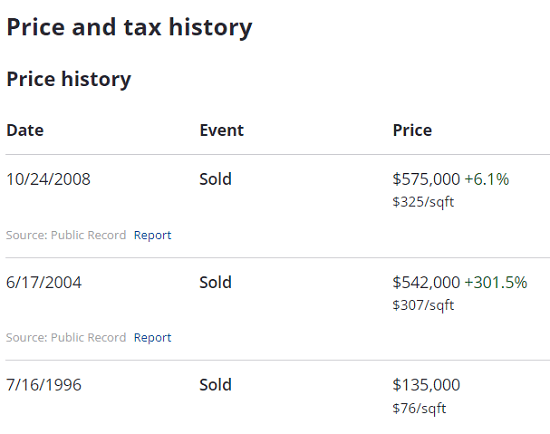

Exhibit #1 in Shelter Becoming a Speculative Asset is a modest house in the San Francisco Bay Area that sold for $135,000 in mid-1996. By modest I mean small, old, and on a small lot in a neighborhood of other small lots and homes. (A screenshot of the Zillow history is below.)

Today the home’s value is estimated to be about ten times higher: $1.35 million. Let’s do some basic math to understand just how distorted this market has become.

The median household income in 1996 was about $39,000. For a house costing $135,000, this represents 3.5 ratio of income to housing, well within the traditional ratio of 4 to 1 (4 X income = cost of the home).

Median household income has almost doubled to $75,000, roughly in line with inflation according to the Bureau of Labor Statistics. According to the BLS, the house that cost $135,000 in July 1996 would now cost $264,000 when adjusted for inflation, and the $39,000 median income would be $76,000.

Let’s say the house appreciated above the rate of inflation to $300,000 today. That’s still within the 4 to 1 ratio of income to house cost (4 X $75,000 = $300,000.) So even though the house rose 2.2X in cost, it would still be affordable to a median household.

At a value of $1.35 million, a household would need to make $337,500 annually–an income that is in the top 5% of households–to buy the house today. In other words, an income that is 4.5 times the median household income is the minimum needed to buy this modest house.

The house is now worth 4.5 times what it would have been worth if it had appreciated well above inflation.

The conventional argument holds that this four-fold increase in housing costs is due solely to a shortage of housing. Let’s consider some data before concluding this is the only dynamic in play.

Chart #1: Case Shiller housing index: this chart shows two massive housing bubbles in the past 20 years.

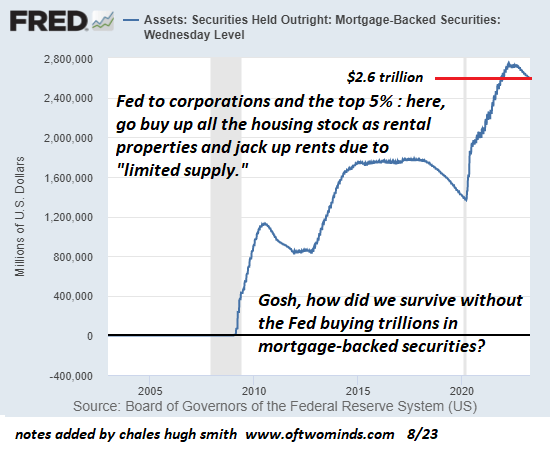

Chart #2: Federal Reserve’s purchases of mortgage backed securities (MBS) to goose the housing market. The “housing shortage” argument claims the unprecedented Fed purchases of trillions of dollars of MBS is not correlated to the housing bubble, but this claim makes no sense: dropping mortgage rates to unprecedented lows while soaking up trillions of dollars in securitized mortgages was like injecting speculative crack cocaine into the housing market. Gosh, how did we survive without the Fed buying $2.5 trillion in mortgages?

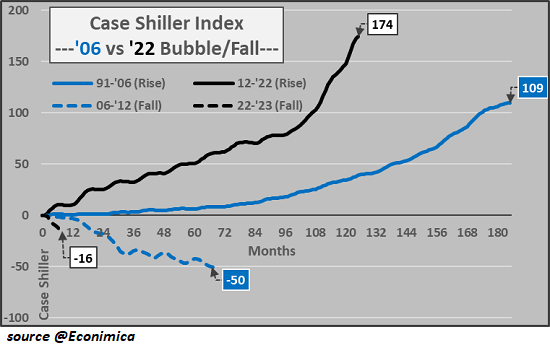

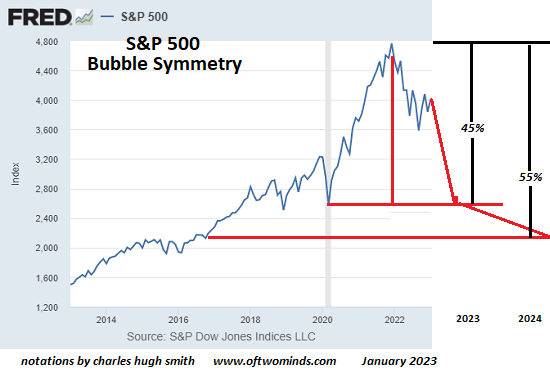

Chart #3: the current housing bubble compared to the 2000-2006 housing bubble: today’s bubble is even more extreme than housing bubble #1.

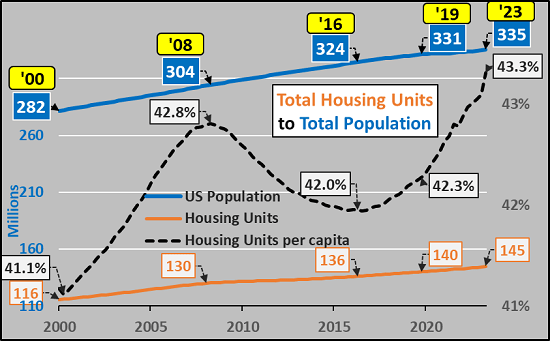

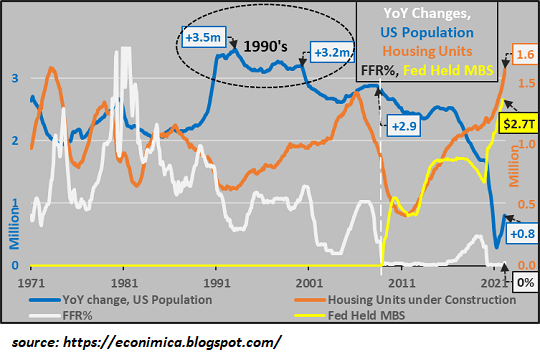

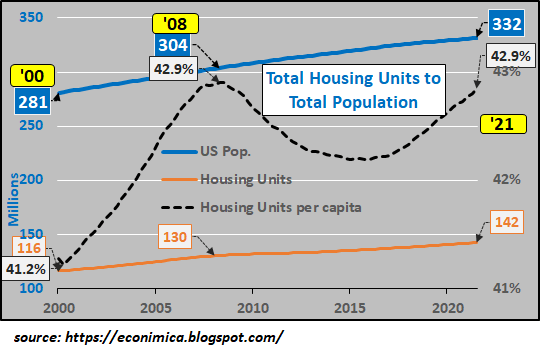

Chart #4: housing per capita (per person) has reached a new high: if there’s such a severe shortage of housing, how can the housing per capita be at an all-time high? Population rose 4 million in the past 4 years while 5 million housing units were added–plus a pig-in-a-python of housing in the pipeline.

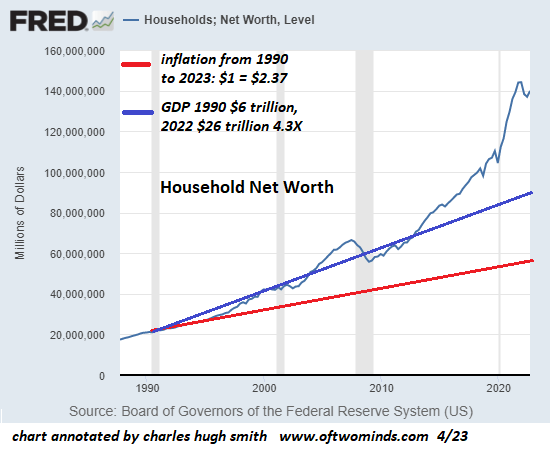

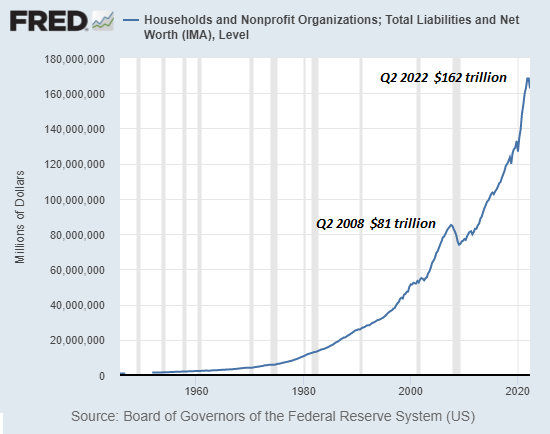

Chart #5: household net worth is $50 trillion above trend, the direct result of massive monetary and fiscal stimulus. Tens of trillions of dollars were borrowed into existence and pumped into so-called risk assets–assets such as housing that the wealthy buy for speculative appreciation.

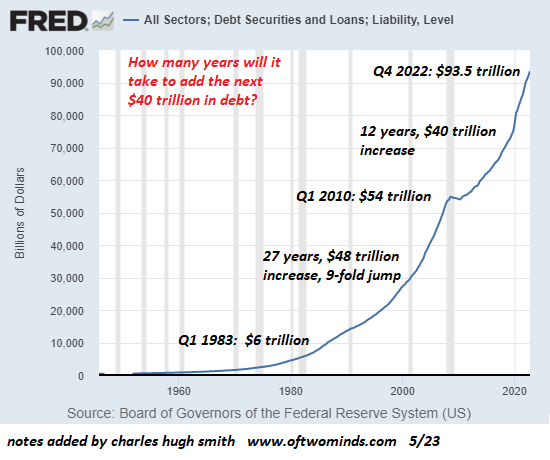

Chart #6: total debt–private and public–soared from $20 trillion in 1996 to $95 trillion now. Is it merely coincidental that this is $55 trillion above the trendline of inflation, which would have placed total debt at $40 trillion today?

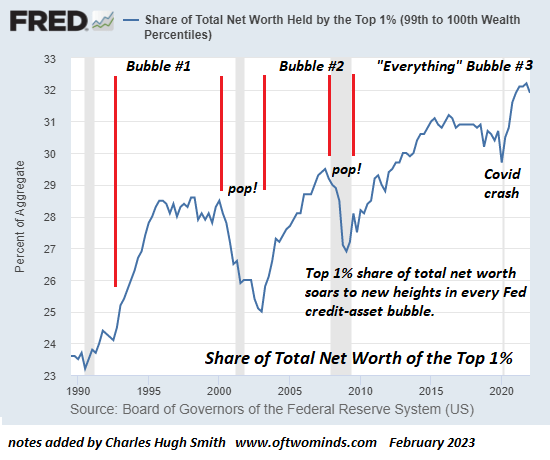

Chart #7: net worth of the top 1% households, which soared from 23% of all net worth to 32%: this 9% gain in the percentage of all household net worth represents a gain of $14 trillion above and beyond the $28.7 trillion in gains registered by the 23% they owned in 1990.

1990 total net worth: $21 trillion, 23% = $4.8 trillion; 2023 total net worth: $146 trillion, 23% = $33.5 trillion; $33.5 trillion – $4.8 trillion = $28.7 trillion.

This unprecedented bubble in housing valuations is due not to shortages but to decades of massive financial stimulus that incentivized speculative capital to flood into housing as a low-risk way to skim stupendous gains for creating zero gains in productivity. If you doubt this, then run this scenario and tell us what happens:

The Fed dumps its entire portfolio of mortgage backed securities and stipulates it will never buy any again. It also renounces all the other stimulus gimmicks that incentivized expansions of debt and speculation.

Does anyone really believe that the renunciation of massive, sustained stimulus of speculation in housing would leave housing valuations unchanged because valuations are solely the result of “shortages”? If so, there’s a little shack under the Brooklyn Bridge I’ll let you have for a couple of million. I’m sure the Airbnb rent will mint you millions.

The resulting erosion of collateral will collapse the global credit bubble, a repricing/reset that will bankrupt the global economy and financial system.

Scrape away the complexity and every economic crisis and crash boils down to the precarious asymmetry between collateral and the debt secured by that collateral collapsing. It’s really that simple.

In eras of easy credit, both creditworthy and marginal borrowers are suddenly able to borrow more. This flood of new cash seeking a return fuels red-hot demand for conventional assets considered “safe investments” (real estate, blue-chip stocks and bonds), demand which given the limited supply of “safe” assets, pushes valuations of these assets to the moon.

In the euphoric atmosphere generated by easy credit and a soaring asset valuations, some of the easy credit sloshes into marginal investments (farmland that is only briefly productive if it rains enough, for example), high-risk speculative ventures based on sizzle rather than actual steak and outright frauds passed off as legitimate “sure-fire opportunities.”

The price people are willing to pay for all these assets soars as the demand created by easy credit increases. And why does credit continue increasing? The assets rising in value create more collateral which then supports more credit.

This self-reinforcing feedback appears highly virtuous in the expansion phase: the grazing land bought to put under the plow just doubled in value, so the owners can borrow more and use the cash to expand their purchase of more grazing land. The same mechanism is at work in every asset: homes, commercial real estate, stocks and bonds: the more the asset gains in value, the more collateral becomes available to support more credit.

Since there’s plenty of collateral to back up the new loans, both borrowers and lenders see the profitable expansion of credit as “safe.”

This safety is illusory, as it’s resting on an unstable pile of sand: bubble valuations driven by easy credit. We all know that price is set by what somebody will pay for the asset. What attracts less attention is price is also set by how much somebody can borrow to buy the asset.

Once the borrower has maxed out their ability to borrow (their income and assets-owned cannot support more debt) or credit conditions tighten, then those who might have paid even higher prices for assets had they been able to borrow more money can no longer borrow enough to bid the asset higher.

Since price is set on the margin (i.e. by the last sales), the normal churn of selling is enough to push valuations down. At first the euphoria is undented by the decline, but as credit tightens (interest rates rise and lending standards tighten, cutting off marginal buyers and ventures) then buyers become scarce and skittish sellers proliferate.

Questions about fundamental valuations arise, and sky-high valuations are found wanting as tightening credit reduces sales, revenues and profits. Once the “endless growth” story weakens, the claims that bubble prices are “fair value” evaporate.

As defaults rise, lenders are forced to tighten credit further. The first tumbling rocks are ignored but eventually the defaults trigger a landslide, and the credit-inflated bubble in asset valuations collapses.

As valuations plummet, so too does the collateral backing all the new debt. Debt that appeared “safe” is soon exposed as a potential push into insolvency. When the bungalow doubled in value from $500,000 to $1 million, the trajectory of valuation gains looked predictably rosy: every decade housing prices went up 30% or more. So originating a mortgage for $800,000 on a house that looked to be worth $1.3 million in a few years looked rock-solid safe.

But the $1 million was a bubble based solely on easy, abundant, low-cost credit. When credit tightens, the home is slowly but surely repriced at its pre-bubble valuation ($500,000) or perhaps much lower, if that value was merely an artifact of a previous unpopped bubble.

Now the collateral is $300,000 less than the mortgage. The owner who made a down payment of $200,000 will be wiped out by a forced sale at $500,000, and the lender (or owner of the mortgage) will take a $300,000 loss.

Given the banking system is set up to absorb only modest, incremental losses, losses of this magnitude render the lender insolvent. The lender’s capital base is drained to zero by the losses and then pushed into negative net-worth by continued losses.

The collateral collapses when bubbles pop, but the debt loaned against the now-phantom collateral remains.

This is the story of the Great Depression, a story that’s unloved because it calls into question the current series of credit-inflated bubbles and resulting financial crises. So the story is reworked into something more palatable such as “the Federal Reserve made a policy error.”

This encourages the fantasy that if central banks choose the right policies, credit bubbles and valuations detached from reality can both keep expanding forever. The reality is credit bubbles always pop, as the expansion of borrowing eventually exceeds the income and collateral of marginal borrowers, and this tsunami of cash eventually pours into marginal high-risk speculative vebtures that go bust.

There is no way to thread the needle so credit-asset bubbles never pop. Yet here we are, watching the global Everything Bubble finally start collapsing, guaranteeing the collapse of collateral and all the debt issued on that collateral, and the rabble is arguing about what policy tweaks are needed to reinflate the bubble and save the global economy from bankruptcy.

Sorry, but global bankruptcy is already baked in. Too much debt has been piled on phantom-collateral and income streams derived from bubble assets rising (for example, capital gains, development taxes, etc.). The asymmetry is now so extreme that even a modest decline in asset valuations/collateral due to a garden-variety business-cycle recession of tightening financial conditions will trigger the collapse of The Everything Bubble and the mountain of global debt resting on the wind-blown sands of phantom collateral.

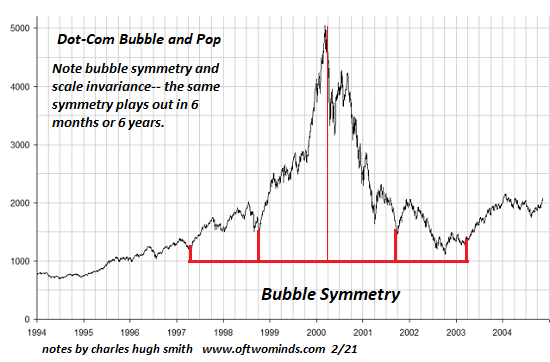

There are persuasive reasons to suspect global debt far exceeds the official level around $300 trillion, most saliently, the largely opaque shadow banking system. When assets roughly double in a few years, bubble symmetry suggests that valuations will decline back to the starting point of the bubble in roughly the same time span.

The resulting erosion of collateral will collapse the global credit bubble, a repricing/reset that will bankrupt the global economy and financial system.

I don’t have to tell you that your money doesn’t go as far as it once did. You see it every time that you go shopping. Our leaders flooded the system with money and pursued highly inflationary policies for years, and now we are all paying the price. The cost of living has been rising much faster than our incomes have, and this is systematically destroying the middle class. Survey after survey has shown that a solid majority of the population is living paycheck to paycheck, and at this point most U.S. consumers are tapped out. In fact, one brand new survey just discovered that 57 percent of Americans cannot even afford to pay a $1,000 emergency expense…

According to Bankrate’s Annual Emergency Fund Report, 68% of people are worried they wouldn’t be able to cover their living expenses for just one month if they lost their primary source of income. And when push comes to shove, the majority (57%) of U.S. adults are currently unable to afford a $1,000 emergency expense.

When broken down by generation, Gen Zers (85%) and Millennials (79%) are more likely to be worried about covering an emergency expense.

These numbers are quite ominous, because they clearly demonstrate that we are completely and utterly unprepared for any sort of a major economic downturn.

And thanks to the rapidly rising cost of living, we are losing even more ground with each passing month.

Nearly three-quarters, or 72%, of middle-income families say their earnings are falling behind the cost of living, up from 68% a year ago, according to a separate report by Primerica based on a survey of households with incomes between $30,000 and $100,000. A similar share, 74%, said they are unable to save for their future, up from 66% a year ago.

We haven’t experienced anything like this in the United States in decades.

When I walked into a Walmart store the other day, I was shocked by how high the prices are now.

Isn’t Walmart supposed to be the place with “low prices every day”?

Well, the prices were certainly not “low” when I walked through the store.

And I was stunned to learn that McDonald’s is now selling one hash brown for three dollars.

I am sure that many of you can remember a time when they were 50 cents.

Sadly, those days are not coming back.

Food prices are going to continue to go up, and the CEO of Unilever recently admitted that his company has actually “been accelerating the rate of price increases that we’ve had to put into the market”…

“For the last 18 months we’ve seen extraordinary input cost pressure … it runs across petrochemical derived products, agricultural derived products, energy, transport, logistics,” he said.

“It’s been feeding through for quite some time now and we’ve been accelerating the rate of price increases that we’ve had to put into the market,” he added.

US retail sales continued their fall in December, dropping by 1.1% as inflation remained high, the Commerce Department reported Wednesday.

That’s the largest monthly decline since December 2021, and practically every category (except for building materials, groceries and sporting goods) saw sales drop from the prior month.

U.S. existing home sales slowed for the 11th consecutive month in December as higher mortgage rates, surging inflation and steep home prices sapped consumer demand from the housing market.

-More Americans than ever before are being forced to pay at least 30 percent of their incomes on rent…

The average US household is now considered ‘rent-burdened’ as a record-high number of people are spending more than 30 percent of their income on rent.

According to Moody’s Analytics’ latest affordability report, the national average rent-to-income (RTI) ratio reached 30 percent for the first time since the company began tracking the data more than 20 years ago.

U.S. consumers are being stretched financially like never before, and many are turning to debt to help them maintain their current lifestyles.

As a result, the savings rate has plunged to a historic low, credit card debt has surged to a record high, and the average rate of interest on credit card balances has also risen to a record high. As Zero Hedge has aptly noted, this is “nothing short of catastrophic”…

The combination of record high credit card debt and record high credit card interest is nothing short of catastrophic for both the US economy, and the strapped consumer who has no choice but to keep buying on credit while hoping next month’s bill will somehow not come. Unfortunately, it will and at some point in the very near future, this will also translate into massive loan losses for US consumer banks; that’s when Powell will finally panic.

For a long time, we have been warned that the very foolish economic policies that our leaders were implementing would have deeply tragic consequences.

And now it is starting to happen right in front of our eyes.

Sadly, the truth is that this is just the beginning.

The entire system is cracking and crumbling all around us, and there is much more pain ahead.

The signs are already present and obvious, but the overall economic picture probably won’t be acknowledged in the mainstream until the situation becomes much worse (as if it’s not bad enough). It’s a problem that arises at the onset of every historic financial crisis – Mainstream economists and commentators lie to the public about the chances of recovery, constantly giving false reassurances and lulling people back to sleep. Even now with price inflation pummeling the average consumer they tell us that there is nothing to worry about. The Federal Reserve’s “soft landing” is on the way.

I remember in 2007 right before the epic derivatives collapse when media pundits were applauding the US housing market and predicting even greater highs in sales and in valuations. I had only been writing economic analysis for about a year, but I remember thinking that the overt display of optimism felt like compensation for something. It seemed as if they were trying to pull the wool over the eyes of the public in the hopes that if people just believed hard enough that all was well then the fantasy could be manifested into reality. Unfortunately, that’s not how economics works.

Supply and demand, debt and deficit, money velocity and inflation; these things cannot be ignored. If the system is out of balance, collapse will set its ugly foot down somewhere and there’s nothing anyone including central banks can do about it. In fact, there are times when they deliberately ENGINEER collapse.

This is the situation we are currently in today as 2022 comes to a close. The Fed is in the midst of a rather aggressive rate hike program in a “fight” against the stagflationary crisis that they created through years of fiat stimulus measures. The problem is that the higher interest rates are not bringing prices down, nor are they really slowing stock market speculation. Easy money has been too entrenched for far too long, which means a hard landing is the most likely scenario.

In the early 2000s the Fed had been engaged in artificially low interest rates which inflated the housing and derivatives bubble. In 2004, they shifted into a tightening process. Rates in 2004 were at 1% and by 2006 they rose to over 5%. This is when cracks began to appear in the credit structure, with 4.5% – 5.5% being the magic cutoff point before debt became too expensive for the system to continue the charade. By 2007/2008 the nation witnessed an exponential implosion of credit, setting off the biggest money printing bonanza in US history in order to save the banking sector, at least for a time.

Since nothing was actually fixed by the Fed back then, I will continue to use the 5% funds rate as a marker for when we will see another major contraction. The difference this time is that the central bank does not have the option to flood the economy with more fiat, at least not without immediately triggering a larger stagflationary spiral. I am also operating on the premise that the Fed WANTS a crash at this time.

“Mainstream financial commentators want to believe the Fed will capitulate because they desperately want the party in stock markets to continue, but the party is over. Sure, there will be moments when the markets rally based on nothing more than a word or two from a Fed official planting false hopes, but this will become rare. Ultimately, the Fed has taken away the punch bowl and it’s not coming back. They have the perfect excuse to kill the economy and kill markets in the form of a stagflationary disaster THEY CAUSED. Why would they reverse course now?”

“What stands out for visitors?” I asked our guide during a Honolulu Chinatown tour with my out-of-town guests. “Always the same, the homeless. Even Mainlanders from big cities like San Francisco and New York are surprised how many we have here. I’m waiting to see how the Japanese and Korean guests respond when they start traveling again.”

You can’t miss his point. During our brief walk through Chinatown’s markets we saw a disturbed man dressed only in his underwear touching himself, several seriously street-worn people begging, and watched the fire department respond to a prone homeless man who was dead or simply drugged into paralysis. When someone in our party needed the toilet, the shopkeeper apologized for having to keep it locked to prevent misuse by vagrants. Many places simply had signs saying “no public toilet.” Despite some great tasting food, it was hard to keep up a holiday spirit. Same for when we passed the tent cities and parks overtaken by homeless along a drive on the Windward side.

The numbers only begin to tell the story. Pre-COVID, there were an estimated 6,458 homeless in Hawaii. The Big Island saw the biggest jump in homelessness from 2019-2020, a 16 percent increase. On Oahu the homeless population is up 12 percent. San Francisco before COVID counted over 8,000 homeless persons, and while COVID-era numbers are hard to pin down, one measure is overdose deaths among the homeless, which have tripled. New York has the highest homeless population of any American metropolis, close to 80,000 and growing. The number of homeless there today is 142 percent higher than it was 10 years ago, and currently at the highest level since the Great Depression. Some 3,000 human beings make their full-time home in the subway.

Estimates for the United States as a whole run well over half a million people living homeless. The number shoots up dramatically if one includes people living in their cars, people on their way to exhausting the good will of friends who offered a couch, and those who slide in and out of motels as money ebbs and flows. Some 21 percent of American children live in poverty, homeless or not. In the end nobody actually knows how many people are living without adequate shelter except that it is a large number and it is a growing number and there is nothing in line to lower it, only to find new ways to tolerate it.

We have in many places already surrendered our public parks and libraries. The hostile architecture of protrusions and spikes which make it impossible to sleep on a park bench are pretty much sculpted into the architecture of the city, markers of the struggle for public space. The idea even has its own Instagram account. A security firm offers tips: restrict access to sidewalk overhangs protected from inclement weather, remove handles from water spigots, and keep trash dumpsters locked. If things get too bad, the company, for a price, will deploy “remote cameras with military-grade algorithms capable of detecting people in areas they shouldn’t be in.”

Keep in mind that all of these homeless people coexist in a United States whose wealthiest citizens have their own spaceships. NYC alone is home to 70 billionaires, more than any other American city. New York is also home to nearly one million millionaires, more than any other city in the world. How is it that the nation’s wealthiest city and poorest city are the same place?

All the solutions seem to fail. There are not enough shelters we are told but even when more shelters are built the homeless are too paranoid to move in,or the shelters become too dirty, too dangerous, chaos compacted, so the transition from an encampment to supportive housing isn’t easy. In ravaged San Francisco, one out of 10 of the city’s already existing supportive housing units are empty, with the director of the Department of Homelessness (!) placing the blame on individuals. So the homeless problem becomes a mental health problem which becomes a drug and alcohol problem which becomes a public health problem. Our society will not force people into care, and it will not deport the homeless against their will to desert camps. Instead we simply do nothing absent throwing a few bucks into food programs as an expedient over stepping around too many bodies in the street. Meanwhile nobody asks why nothing seems to work.

When you look at history with enough perspective you see very little happens without cause and effect. Things are connected. Casualty matters more than randomness. Answering the question of what to do about homelessness requires first answering the question of why we have the problem in the first place. Because while homelessness exists elsewhere in the developed world, you simply do not see it at pandemic proportions in equally-developed nations across Europe, and certainly not in the economic superstates like China, Japan, Singapore, et al. Scale and size matter and America wins on both. Why?

Because the American economic system requires homelessness. That’s why we can’t solve homelessness; no matter how much solving you do the system just makes more.

The Democratic arguments over raising the minimum wage are a smokescreen. As long there is a minimum wage and businesses do not have to compete for workers, there have to be homeless people. Think of the homeless as run-off, the unfortunate but necessary waste product of an economic system designed to exploit workers for the benefit of space-traveling overlords. The homeless — no wagers — are the endpoint of an economic spectrum dominated by the minimum wagers, people whose salary and hours, and thus whose chance at lifetime wealth status, are capped by agreement between the government and industry.

Until slavery ended, human beings were considered capital, just like stock today. Now we’re “human resources” so everything’s better. Bringing up race hides the real story of how long this has been going on and how deep a part of our way of life it is. The line between controlling someone with a whip and controlling someone through ever-lower wages gets finer and finer over time.

This is what “systematic” means: a system of public-private sector agreements codified as laws which push workers into a cesspool as grab-and-go disposable labor. Those who sink end up homeless. Those who tread water are guaranteed a life of maybe just enough, their place in society fixed for others’ goals, never their own. It also assures the sales of drugs, alcohol, and lottery tickets as the working poor try to convince themselves all this can’t be true. Can it?

The next step is clear. The working poor are allowed to exist at survival levels only because they are in jobs too expensive or difficult to automate. You think there are a lot of homeless now? Wait until self-driving vehicles click in and another job category simply disappears, leaving drivers and delivery people nowhere to go (there are more than 3.5 million truck drivers in the U.S., making driving one of the most popular occupations.) Same for fast food and other service jobs. Soon enough AI and/or remote online learning will make live teachers an expensive luxury for the children of the wealthy.

If you wanted a clever term about why we have and ignore and can’t address the homeless problem, you could call it systemic inequality in tune with the times’ nomenclature. A system designed to exploit will always exploit too much at its edges. It is supposed to, in order to keep driving the center downward, from 1950s middle class to 2022’s working poor.

But in the near term the issue isn’t confronting the reality of inequality, it is navigating the society it has created, much as my tour guide directed us around the homeless nests in Chinatown so we could sample the dim sum at leisure. “Don’t make eye contact” was some of his best advice.

Ramin Bahrani makes films about the American Dream as seen through the eyes of those on the margins of the increasingly unrealistic “mainstream” life: immigrants, children, transplants, or those too damaged to participate anymore (like the grizzled old dude played by Red West in “Goodbye Solo“). For the most part, these people still believe in the American Dream. They hope, strive, plan. But the system has failed them. The system is broken, and never more broken than in Bahrani’s latest film, “99 Homes,” starring Michael Shannon, Andrew Garfield and Laura Dern.

“Don’t get emotional about real estate,” warns real estate broker Rick Carver (Shannon) throughout “99 Homes,” as people are forcibly evicted after defaulting on bank payments. Carver’s may be practical advice, considering the economic crash and the housing crisis, but it is also heartless. Real estate to Rick Carver means money and opportunity; real estate to everyone else means “home,” and what is more emotional to human beings than the concept of “home”?

The film opens with a brutal eviction sequence, filmed in one take. Blood spatters the bathroom walls as the resident commits suicide, all as the sheriff’s department swoops through the house, overseen by Rick Carver, a shark-eyed man in an ill-fitting blue suit, smoking a glowing-blue electric cigarette. The story shifts to Dennis Nash (Andrew Garfield), a single dad living with his mother (Laura Dern) and his little boy Connor (Noah Lomax) in the family home. Mom works a hairdressing business out of the living room. Dennis works construction but jobs are hard to come by. Nobody’s building anymore. Bills pile up. They are in danger of losing their home. Dennis goes to court to fight for more time, he tries to get a lawyer to work pro bono.

One day, the reckoning arrives. The sheriff’s department shows up, led by Rick, to evict them. In a harrowing scene of mounting panic, Dennis and his mother protest as Rick drawls, both easily and with enormous aggression, “This isn’t your house anymore, son.” The fight that ensues is acted and filmed with almost unbearable immediacy (cinematographer Bobby Bukowski does superb work throughout). Given two minutes to vacate, the hyperventilating family pile up whatever possessions they can fit into the back of a pick-up truck, and head to a cheap motel, filled with people in the same situation. “We’ve been here two years now,” says a woman.

Dennis will do what it takes to get his home back, including accepting a job working construction for his nemesis Rick. It’s a deal with the devil, and all that that implies. Dennis gets sucked into Carver’s circle of easy cash, shady deals. Within almost no time, Dennis is on the other side of those evictions, standing in the doorway, waiting for the confused angry residents to vacate. The door-to-door sequences are masterful. These people don’t seem to be professional actors (although they may be), their reactions are so raw and real. The audience is placed in the uncomfortable position of voyeurs, eavesdroppers, on a human being’s lowest moment.

“99 Homes” operates like a thriller (from its stunning opening one-take sequence), with elements of melodrama to heighten the stakes. (Some of the melodramatic elements don’t work as well as the rest, relying, as they do, on coincidence, racing against the clock, etc; the reality is horrifying enough.) Held together with Antony Partos and Matteo Zingales’ portentous original score, thrumming underneath almost every scene, “99 Homes” represents a shift for Bahrani. His other features have been small dramas, filmed accordingly: lots of hand-held camera work and a naturalistic approach. “99 Homes” has a strong look, a bold mood, with attention-getting shots like that opener, as well as a couple of aerial shots showing homes stretched out below. From that vantage point, homes look generic. To those on the ground, of course, it’s a very different story.

Andrew Garfield, as a man who has “failed” in his duty as protector and provider, has an almost constant sense of panic throughout, catching his breath in his throat, his posture tight and alert. Tears threaten to overwhelm him, but Dennis does not have time for self-pity. Nobody does. His one goal is to get his house back, the crevasse of permanent instability opening beneath him and his family. Bahrani keeps that heat turned up in the machinations of the plot, as Carver seduces Dennis with offers of wealth (meaning, in Carver’s world, self-respect). “America doesn’t bail out losers,” Carver tells Nash. “America bails out winners.”

Michael Shannon is both ruthless and strangely tender in his seemingly irredeemable character. Carver explains his background to Dennis, his humble roots, his roofer father, his jobs in construction. Up until the crash, his job was putting people into homes. It’s not his fault that his job has now become throwing people out. Any hard economic time will create a man like Rick Carver, determined to make more money off the slump than the boom. It’s a very honest performance.

Reminiscent of the films of Jafar Panahi (which also focus on those on the margins), Bahrani’s films are a critique of the very concept of “mainstream.” If there is to be a mainstream, then the boundaries must be more inclusive. Bahrani’s films represent an urgent demand that audiences pay attention to the world and the people around them. His films insist: Look. See. Bahrani accomplishes this not by making “message” films, but by focusing on individual characters, whether it be a Pakistani former singer who now pushes a food cart in Manhattan (“Man Push Cart,”) a little Latino boy working in an auto-body shop (“Chop Shop,”) or the optimistic Senegalese-American who drives a cab and dreams of being a flight attendant (“Goodbye Solo.”) Through these characters, Bahrani critiques American life, its economics, its class divides, its assumptions and social strata. Like Panahi, he is a humanist. The dignity of the individual is all.

“99 Homes” is a ferocious excavation of the meaning of home, the desperation attached to real estate, the pride of ownership and the stability of belonging. The pace never lets up. Once a person slips below the mainstream, it is nearly impossible to gain a foothold again. These characters struggle like hell to survive.

Are we heading into another real estate bubble / crash? Those who say “no” see the housing shortage as real, while those who say “yes” see the demand as a reflection of the Federal Reserve’s artificial goosing of the housing market via its unprecedented purchases of mortgage-backed securities and “easy money” financial conditions.

My colleague CH at econimica.blogspot.com recently posted charts calling this assumption into question. The first chart (below) shows the U.S. population growth rate plummeting as housing starts soar, and the second chart shows housing unit per capita, which has just reached the same extreme as the 2008 housing bubble.

Demographics and housing do not reflect a housing shortage nationally, though there could be scarcities locally, of course, and other factors such as thousands of units being held off the market as short-term rentals or investments by overseas buyers who have no interest in renting their investment dwellings.

On a per capita basis, housing has reached previous bubble levels. That suggests housing shortages are artificial or local, not structural.

Next, let’s consider how the current housing bubble differs from previous bubbles in the late 1970s and 2000s. In my view, the previous bubbles were driven by demographics, inflation and monetary policy: in the late 70s, the 65 million-strong Baby Boom generation began buying their first homes, pushing demand higher while inflation soared, making real-world assets such as housing more desirable.

Once the Federal Reserve pushed interest rates to 18%, mortgage rates rose in lockstep and housing crashed as few could afford sky-high housing prices at sky-high mortgage rates.

The housing bubble of 2007-08 was largely driven by declines in mortgage rates (as the Fed pursued an “easy money” policy to escape the negative effects of the Dot-Com stock market bubble crash) and a loosening of credit/mortgage standards. These fueled a bubble that morphed into a speculative free-for-all of no-down payment and no-document loans.

This decline in the cost of borrowing money (mortgage rates) enabled a sharp rise in the price of housing, a speculative boom that was greatly accelerated by “innovations” in the mortgage market such as zero down payments loans, interest-only loans, home equity loans, and no-document “liar loans”–mortgages underwritten without the usual documentation of income and net worth.

These forces generated a speculative frenzy of house-flipping, leveraging the equity in the family home to buy two or three homes under construction and selling them before they were even completed for fat profits, and so on.

Needless to say, the pool of potential buyers expanded tremendously when people earning $25,000 a year could buy $500,000 houses on speculation.

Once the bubble popped, the pool of buyers shrank along with the home equity.

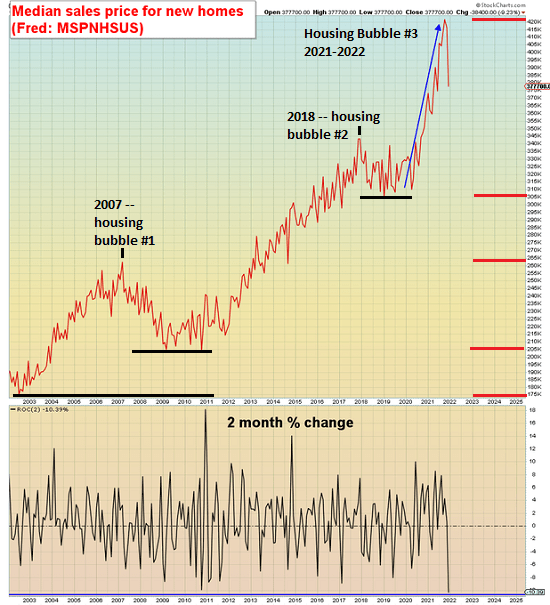

If we study this chart below of new home prices (courtesy of Mac10), we can see that the 21st century’s Bubble #2 rose as the Federal Reserve pushed mortgage rates far below historic norms. Once rates reached a bottom, the 7-year inflation of home prices (from 2011 to 2018) began rolling over.

This deflation of home prices was reversed by the pandemic recession, as the Fed’s vast expansion of credit and mortgage-buying, which pushed mortgage rates to new lows. Trillions of dollars in new credit and cash stimulus ignited a speculative frenzy in stocks, bonds and real estate, a frenzy which drove bubble #3 to extraordinary heights.

All this unprecedented fiscal and monetary stimulus also ignited inflation, and so rates are rising in response. Bubble #3 is already deflating, at least by the measure of new home prices.

But the current bubble has a number of dynamics that weren’t big factors in previous bubbles.

One is the rise of remote work. Many people have been working remotely since the late 1990s enabled Internet-based work, but the pandemic greatly increased the pool of employers willing to accept remote work as a permanent feature of employment.

This trend has been well documented, but the consequences are still unfolding: remote workers are no longer trapped in unaffordable, congested cities and suburbs.

Several other trends have attracted much less attention, but I see them as equally consequential.

1. Housing in many urban zones are out of reach of all but the top 10% without extraordinary sacrifice, and now that employment isn’t necessarily tied to urban zones, the bottom 90% of young people without family wealth or high incomes are coming to realize the benefits of urban living are not worth the extreme sacrifices needed to buy an overvalued house.

A middle-class life–home ownership, financial security, leisure and surplus income to invest in one’s family and well-being–is no longer affordable for the majority of young Americans.

Few are willing to concede this because it reveals the neofeudal nature of American life. Those who bought homes in coastal urban zones 20+ years ago are wealthy due to soaring housing valuations while young people can’t even afford the rent, much less buying a house.

If you’re not making $250,000 or more a year as a couple, the only hope for a middle-class life that includes leisure and some surplus income to invest is top move to some place with much lower housing and other costs. That place is rural America.

2. The benefits of urban living are deteriorating while the sacrifices and downsides are increasing. Urban living is fun if you’re wealthy, not so fun if you don’t have plenty of surplus income to spend.

Urban problems such as homelessness, traffic congestion and crime are endemic and unresolvable, though few are willing to state the obvious. Americans are expected to be optimistic and to count on some new whiz-bang technology to solve all problems.

Unfortunately, problems generated by dysfunctional, overly complex institutions, corruption and unaffordable costs can’t be solved by some new technology, and so the decay of cities will only gather momentum.

The hope that billions of federal stimulus funding would solve these problems is about to encounter reality as the funds dry up and all the problems remain or have actually expanded despite massive “investments” in solutions.

Few analysts have looked at the finances of high-cost cities. The decline in bricks-and-mortar retail, rising crime, soaring junk fees, rents and property taxes have all made urban small business insanely costly and therefore risky.

Small businesses are the core sources of employment and taxes. As high costs, crime, etc. choke small businesses, employment and tax revenues drop and commercial real estate sits empty, generating decay and defaults.

Once office and retail space is no longer affordable or necessary, commercial real estate crashes in value as owners who bought at the top default and go bankrupt.

People need shelter but they don’t need office space or to start a bricks-and-mortar retail business.

As urban finances unravel, cities won’t have the funding to run their bloated, inefficient, overly complex and unaccountable bureaucracies.

3. In geopolitics, we speak of the core and the periphery. Empires have a core (Rome and central Italy in the Roman Empire) and a periphery (Britain, North Africa, Egypt, the Levant).

As finances and trade decay and costs soar, the periphery is surrendered to maintain the core.

In urban zones, the same dynamic will become increasingly visible: the peripheral neighborhoods will be underfunded to continue protecting the wealthy enclaves.

Crime will skyrocket in the periphery even as residents of the wealthy enclaves see little decay in their neighborhoods.

This asymmetry–already extreme–will drive social unrest and disorder. This is a self-reinforcing feedback: as the periphery neighborhoods deteriorate, the remaining businesses flee and the smart money sells and moves away.

Tax revenues plummet and city services decay even further, persuading hangers-on to move before it gets even worse. Cities compensate for the lower revenues by increasing taxes on the remaining residents and cutting services.

Each turn of the screw triggers more closures and selling and fewer tax revenues.

4. Dependency chains will become increasingly consequential: the greater a city’s dependency on essentials trucked/shipped from hundreds or thousands of of kilometers/miles away, the more prone that city will be to disruptions of essentials: food, energy, materials and infrastructure.

Though few are willing to dwell on such vulnerabilities, most cities are totally dependent on diesel fueled fleets of trucks, rail and jet fuel for luxuries flown in from afar for virtually all goods. Cities produce very little in the way of essentials such as food and energy.

The past reliability of long supply chains has instilled a confidence that these supply chains stretching thousands of kilometers and miles are unbreakable and forever. They aren’t, and the initial disruptions will be a great shock to Americans who believe full gas tanks and fully stocked store shelves are their birthright.

5. As I’ve explained in my new book Global Crisis, National Renewal, the era of cheap, reliable abundance has drawn to a close and now we are entering an era of scarcity in essentials.

Another reality few discuss is the relative stability of global weather over the past 40 years. As weather becomes less reliable, so too do crop yields and food supplies.

Globalization has poured capital into expanding acreage under cultivation to the point that the planet’s forests are being decimated to grow more soy to feed animals to be slaughtered for human consumption.

On the margins, land that was once productive has been lost to desertification. Fresh water aquifers have been drained and glaciers feeding rivers are melting away. Soil fertility has declined even as fertilizer use has expanded.

The low-hanging fruit of GMO seeds, fertilizers, insecticides, herbicides and Green Revolution hybrids have all been plucked. The gains have been reaped but now the downsides of these dependencies are becoming increasingly consequential: fertilizer costs are rising fast, insects and diseases are evading chemicals and vaccines, and the vulnerabilities of mono-crop, industrialized agriculture and animal husbandry threaten to cascade into crop failures, soaring prices and shortages.

6. This will have two consequences: rural incomes which have been falling for decades due to globalization (i.e. bringing in cheap food from places with no environmental standards, cheap labor and few taxes / social costs) will start rising sharply, fueling a reversal in the long decline of rural communities based on agricultural income.

The soaring costs of essentials will reduce the disposable income of the bottom 90%, reducing the money they’ll have to spend on eating out, retail shopping, etc.–all the surplus spending that drives cities’ economies and tax revenues.

Few (if any) commentators forecast a cyclical reversal of the demographic trend of people moving from rural locales to cities. I think this trend has already reversed and will gather momentum as cities become increasingly unlivable, disposable incomes decline as scarcities push prices higher and people flee for lower cost, more secure environs.

7. As I often note, following what the super-wealthy are doing is a pretty sound investment strategy because the super-wealthy spend freely to buy the best advice and are highly motivated to protect their wealth.

People who live in well-known, highly desirable rural towns (Telluride, Jackson Hole, Lake Tahoe, etc.) are describing a feeding frenzy of wealthy urbanites buying multi-million dollar homes. Small cities such as Bozeman, MT and Ashville, NC are experiencing a flood of new residents that is straining infrastructure and pushing housing prices out of reach for local residents with average wages.

8. Rural towns in the U.S., Italy, Japan and even Switzerland are trying to attract new residents with offers of free land, subsidized rent, low cost homes, etc. This shows that the trends are global and not limited to any one nation. Would you take free land in rural America?

The decay of urban life isn’t yet consequential enough to push people into making a major move, but once someone has been robbed, repeatedly found human feces on their doorstep or experienced scarcities that trigger the madness of crowds, the decision to leave becomes much, much easier.

Some cities will manage the decline of employment and tax revenues more gracefully than others. Most will suffer from the dynamic I’ve often described on the blog: the Ratchet Effect. Costs move effortlessly higher as tax revenues have increased in one speculative bubble after another, but once revenues drop, cities have no mechanisms or political constituency to manage a sharp, long-term decline in revenues.

They then become prone to the other dynamic I’ve described, the Rising Wedge Breakdown (see chart below): as agencies and institutions become sclerotic, unaccountable and self-serving, even a relatively modest cut in revenues triggers institutional collapse, as the system requires 100% funding to function. A 10% reduction doesn’t cause a 10% decline in service, it causes an 50% decline in service, on the way to complete dysfunction.

Few believe cities can unravel, but remote work, geographic arbitrage (discussed below), tightening credit, rising crime, the decline of commercial real estate, end of massive stimulus, scarcities, the madness of crowds, the decline of civic services and amenities and an insanely high cost of living all have consequences and second-order effects.

What were beneficial synergies become fatal synergies as dynamics reverse and begin reinforcing each other.

So let’s put all this together.

A. The cycle of declining interest rates and inflation has ended and a cycle of much higher interest and mortgage rates and inflation is beginning. Higher mortgages rates will depress housing prices as only the highest income households will be able to afford today’s prices once mortgage rates rise.

B. The decay of urban finances and quality of life will accelerate as stimulus ends, credit dries up and inflation decimates disposable income.

C. The stress of trying to make enough money to afford the high costs of city/suburban living as the real estate bubble pops and the benefits of city living decline will burn out increasing numbers of people who will have no choice but to find more affordable, more secure and more livable places.

D. While the wealthy have already secured second or third homes in the toniest desirable towns, there are still opportunities for lower cost, more secure residences in rural areas.

E. This migration, even at the margins, will further depress urban housing prices and push prices in desirable rural locales higher.

F. This migration will have regional, ethnic and cultural variations. For example, some African-Americans leaving the upper Midwest are finding favor with communities in the South where family, church and cultural ties beckon.

G. Correspondent John F. used the phrase geographic arbitrage which means earning money remotely in high-wage sectors while living some place that’s low cost and secure.

I wrote about this many years ago in my post about young Japanese maintaining a part-time remote-work gig while pursuing farming in rural communities: Degrowth Solutions: Half-Farmer, Half-X (July 19, 2014).

H. Though monetary / inflationary forces will pop housing prices based solely on low mortgage rates, this doesn’t mean housing everywhere will decline: as burned out urbanites seek lower cost, more secure and livable places in rural locales, homes in desirable towns and small cities could rise sharply because they’re starting from such low levels.

I. If urban areas decay rapidly, housing prices could plummet much faster than most people think possible.

When cities lose employment, tax revenues and desirability, they can go down fast. Property values can fall in half and then by 90%.

How is this possible? Supply and demand: if demand falls off a cliff, there won’t be buyers for thousands of homes that come on the market all at once. This is just like a stock market in which buyers disappear, as no one wants to buy an asset that’s rapidly losing value.

As I’ve noted many times, prices for assets are set on the margins: the last sale of a house resets the price for the entire neighborhood.

The stock market is easily manipulated by the big players, who can stop a slide in prices by buying huge chunks of stocks and call options. There are no equivalent forces which can stop a decline in housing prices.

And since rates will rise regardless of what the Federal Reserve does because global capital is demanding a real return above inflation, then the hope for lower mortgage rates to support bubble-level housing prices will be in vain.

How low could housing go? As explained above, there will likely be very asymmetric declines and increases in housing valuations going forward. But on a technical-analysis level, we can anticipate a general decline to previous lows, first to the 2019 lows and then to the 2011 lows.

Some analysts believe inflation will funnel capital into housing as investors seek assets that will go up with inflation, but this is a murky forecast: the bottom 90% of American households are already priced out of coastal housing, so inflation only robs their wages of purchasing power. They don’t have any hope of buying a house anywhere near current prices.

Corporations are buying thousands of houses for the rental income, but once all the stimulus runs out and the excesses of speculation reverse, they’ll find few renters can afford their sky-high rents. At that point corporate buyers become corporate sellers, but they won’t find buyers willing or able to pay their asking prices, which are based on bubble pricing, not reality.

All these swirling currents will affect housing valuations in different places differently. Some areas could see 50% declines while others see 50% increases, regardless of mortgage rates or Fed policy.

What will become most desirable is a low cost of living, security and livability, which includes community, reduced dependency on long supply chains and local production of essentials.

We are all prone to believing the recent past is a reliable guide to the future. But in times of dynamic reversals, the past is an anchor thwarting our progress, not a forecast.

Most Americans don’t realize this, but we truly have entered historic territory. As you will see below, the inflation crisis of 2022 has now escalated to a level that is beyond anything that we experienced during the horrible Jimmy Carter era of the 1970s. If you are old enough to have been alive back then, you probably remember the constant headlines about inflation. And you also probably remember that it seemed like the impotent administration in power in Washington was powerless to do anything about it. In other words, it was a lot like what we are going through today. Unfortunately for us, this new economic crisis is still only in the very early chapters.

Of course the mainstream media would like us to believe that what we are experiencing today is not even close to what Americans went through in the late 1970s and early 1980s. According to CNN, the U.S. inflation rate hit a peak of 14.6 percent in the first half of 1980…

The inflation rate hit a record high of 14.6% in March and April of 1980. It helped to lead to Carter’s defeat in that fall’s election. It also led to some significant changes in the US economy.

Compared to that, the numbers we have been given in early 2022 seem rather tame. On Tuesday, we learned that the official rate of inflation in the U.S. hit 8.5 percent in the month of March…

Prices that consumers pay for everyday items surged in March to their highest levels since the early days of the Reagan administration, according to Labor Department data released Tuesday.

The consumer price index, which measures a wide-ranging basket of goods and services, jumped 8.5% from a year ago on an unadjusted basis, above even the already elevated Dow Jones estimate for 8.4%.

8.5 percent is much lower than 14.6 percent, and so to most people it would seem logical to conclude that we are still a long way from the kind of nightmarish crisis that our nation endured during the waning days of the Carter administration.

But is that the truth?

In reality, we can’t make a straight comparison between the official rate of inflation in 2022 and the official rate of inflation in 1980. The way that the inflation rate is calculated has been changed more than 20 times since 1980, and every time it was changed the goal was to make the official rate of inflation appear to be lower.

What we really need is an apples-to-apples comparison; fortunately, John Williams over at shadowstats.com has done the math for us.

According to Williams, if the inflation rate was still calculated the way that it was back in 1980, the official rate of inflation would be somewhere around 17 percent right now.

17 percent!

That means that the inflation that we are seeing now is even worse than anything that Americans went through during the Jimmy Carter era.

And government figures for individual categories seem to confirm that inflation is now wildly out of control. For example, the price of gasoline has risen by 48 percent over the past year…

The price of gasoline rose by 48.0 percent from March 2021 to March 2022, according to numbers released today by the Bureau of Labor Statistics.

In just one month—from February to March—the seasonally adjusted price of gasoline went up 18.3 percent.

Vehicle prices have escalated to absurd levels as well. If you can believe it, the average retail selling price of a used vehicle at CarMax has risen by 39.7 percent in just 12 months…

CarMax experienced a slowdown in fourth-quarter used car sales volume as its average retail selling price jumped 39.7% year-over-year to $29,312, an increase of approximately $8,300 per unit.

And I discussed yesterday, home prices in the United States have jumped 32.6 percent over the past two years.

We have entered a full-blown inflationary nightmare, and the Biden administration is trying to blame Vladimir Putin for it.

Needless to say, that is extremely disingenuous of Biden, because prices were already skyrocketing even before the war in Ukraine started.

But it is true that the war is making economic problems even worse all over the globe, and that isn’t going to end any time soon.

A couple of weeks ago there was a bit of optimism that some sort of a ceasefire agreement could be reached, but now there appears to be no hope that there will be one any time soon.

On Tuesday, Putin told the press that peace talks have reached “a dead end”…

Talks with Ukraine have reached “a dead end,” Russian President Vladimir Putin said in fresh Tuesday remarks. “We will not stop military operations in Ukraine until they succeed.” He explained that Ukraine has “deviated” from agreements and any possible prior progress reached during the Istanbul meetings, according to state-run RIA.

The strong remarks aimed at both Kiev and the West were given during a joint presser with his Belarusian counterpart Alexander Lukashenko. He further hailed that the military operations is still going “according to plan,” Bloomberg reports, however while admitting to the domestic population that “Russian logistics and payment systems remain a weakness and the long-term impact of western measures could be more painful.” But he also said the county has withstood the economic “blitzkrieg” from the West.

Ukrainian President Volodymyr Zelensky named recognition of the annexation of the Crimea region as one of his red lines for Moscow in any potential peace talks with Russian President Vladimir Putin to end war between the two countries.

Russia annexed the southern region of Crimea in 2014. Russian-backed separatists and forces, as well Ukrainian soldiers, have since been fighting in the eastern region of Ukraine.

Russia will never, ever willingly give Crimea back to Ukraine.

Anyone who thinks otherwise is simply being delusional.

So unless someone changes their tune, this war between Russia and Ukraine is going to keep going until someone achieves total victory.

And that could take a really long time.

Meanwhile, global food supplies will get tighter and tighter, and global economic conditions will continue to rapidly deteriorate.

And so what happens if another “black swan event” or two hits us later in 2022?

We are so vulnerable right now, and it wouldn’t take much at all to push us over the edge and into an unprecedented worldwide crisis of epic proportions.