Does anyone really believe that the renunciation of massive, sustained stimulus of speculation in housing would leave housing valuations unchanged because valuations are solely the result of “shortages”?

Let’s begin by stipulating that speculation (i.e. gambling) is part of human nature. The role of regulations and policy is to limit the damage that gambling inevitably inflicts when “sure things” cliff-dive into losses.

In other words, where the speculative frenzy and money flows matters. When the South Sea Bubble expanded circa 1713-1720, this flood tide of speculative capital did not distort the cost of shelter and bread in England; it was limited to a purely financial marketplace of shares in the company. When the bubble imploded in 1720, the losses fell mostly on wealthy investors like Isaac Newton.

The same can be said of the speculative mania of the dot-com era: the bubble and collapse were limited to the tech sector and those participating in the sector and the speculative frenzy. The cost of rent and bread did not double due to the speculative bubble’s inflation or bursting.

In contrast, when speculation floods into shelter / housing, it fatally distorts the cost of housing non-speculators must pay. I say fatally because shelter, along with food, energy and water (the FEW resources), are essential to life. These are not discretionary things we can decide not to have. When the price of essentials soars due to speculation that only rewards the speculators at the expense of non-speculators, the fuse of social disorder is lit.

Anyone who believes policies that encourage the wealthy to hoard housing to the point that the bottom 80% (or the bottom 95% in some areas) cannot afford to buy a home are just peachy is overdosing Delusionol. The social consequences are severe and uncontainable once the worm turns.

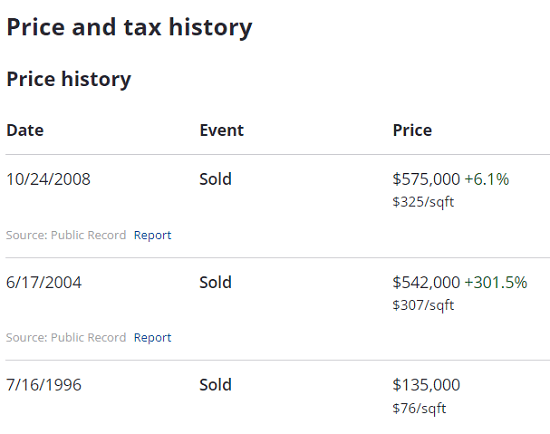

Exhibit #1 in Shelter Becoming a Speculative Asset is a modest house in the San Francisco Bay Area that sold for $135,000 in mid-1996. By modest I mean small, old, and on a small lot in a neighborhood of other small lots and homes. (A screenshot of the Zillow history is below.)

Today the home’s value is estimated to be about ten times higher: $1.35 million. Let’s do some basic math to understand just how distorted this market has become.

The median household income in 1996 was about $39,000. For a house costing $135,000, this represents 3.5 ratio of income to housing, well within the traditional ratio of 4 to 1 (4 X income = cost of the home).

Median household income has almost doubled to $75,000, roughly in line with inflation according to the Bureau of Labor Statistics. According to the BLS, the house that cost $135,000 in July 1996 would now cost $264,000 when adjusted for inflation, and the $39,000 median income would be $76,000.

Let’s say the house appreciated above the rate of inflation to $300,000 today. That’s still within the 4 to 1 ratio of income to house cost (4 X $75,000 = $300,000.) So even though the house rose 2.2X in cost, it would still be affordable to a median household.

At a value of $1.35 million, a household would need to make $337,500 annually–an income that is in the top 5% of households–to buy the house today. In other words, an income that is 4.5 times the median household income is the minimum needed to buy this modest house.

The house is now worth 4.5 times what it would have been worth if it had appreciated well above inflation.

The conventional argument holds that this four-fold increase in housing costs is due solely to a shortage of housing. Let’s consider some data before concluding this is the only dynamic in play.

Chart #1: Case Shiller housing index: this chart shows two massive housing bubbles in the past 20 years.

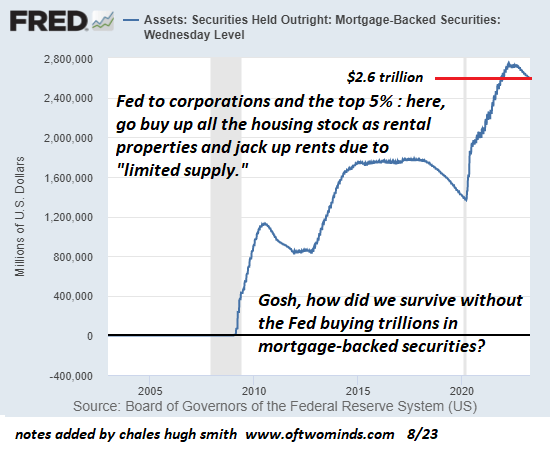

Chart #2: Federal Reserve’s purchases of mortgage backed securities (MBS) to goose the housing market. The “housing shortage” argument claims the unprecedented Fed purchases of trillions of dollars of MBS is not correlated to the housing bubble, but this claim makes no sense: dropping mortgage rates to unprecedented lows while soaking up trillions of dollars in securitized mortgages was like injecting speculative crack cocaine into the housing market. Gosh, how did we survive without the Fed buying $2.5 trillion in mortgages?

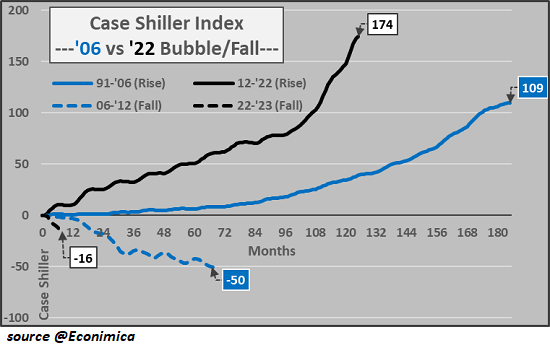

Chart #3: the current housing bubble compared to the 2000-2006 housing bubble: today’s bubble is even more extreme than housing bubble #1.

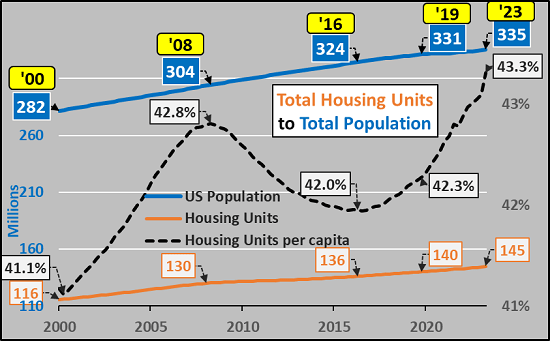

Chart #4: housing per capita (per person) has reached a new high: if there’s such a severe shortage of housing, how can the housing per capita be at an all-time high? Population rose 4 million in the past 4 years while 5 million housing units were added–plus a pig-in-a-python of housing in the pipeline.

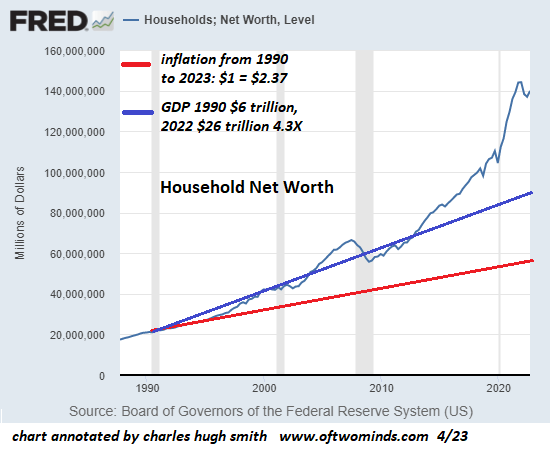

Chart #5: household net worth is $50 trillion above trend, the direct result of massive monetary and fiscal stimulus. Tens of trillions of dollars were borrowed into existence and pumped into so-called risk assets–assets such as housing that the wealthy buy for speculative appreciation.

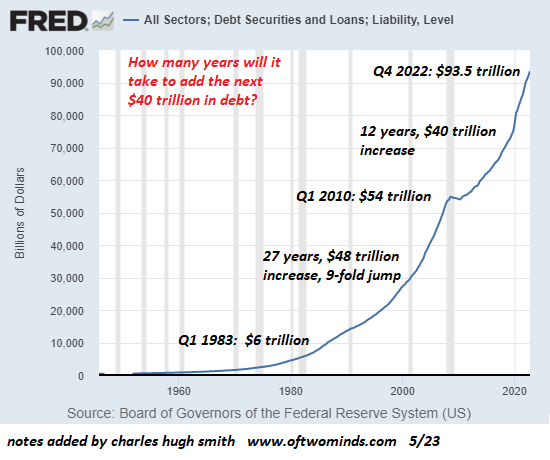

Chart #6: total debt–private and public–soared from $20 trillion in 1996 to $95 trillion now. Is it merely coincidental that this is $55 trillion above the trendline of inflation, which would have placed total debt at $40 trillion today?

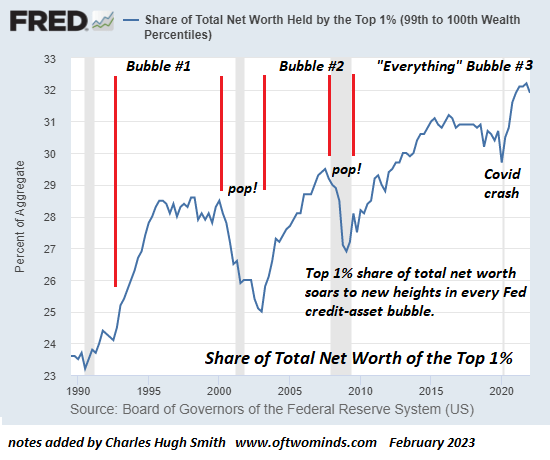

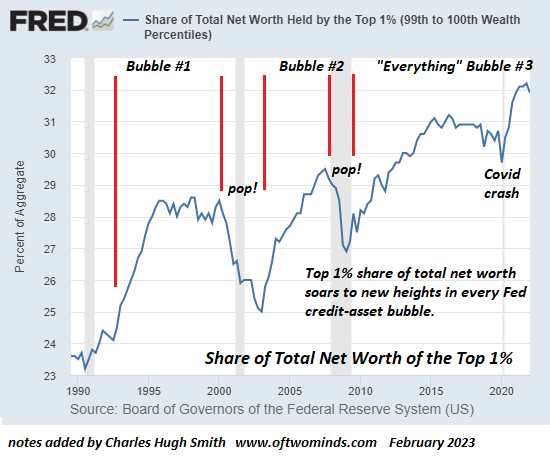

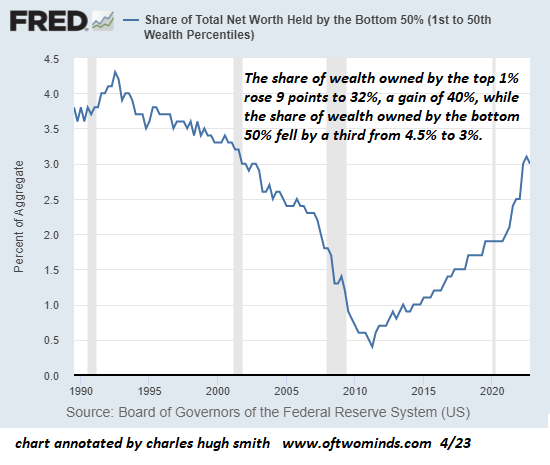

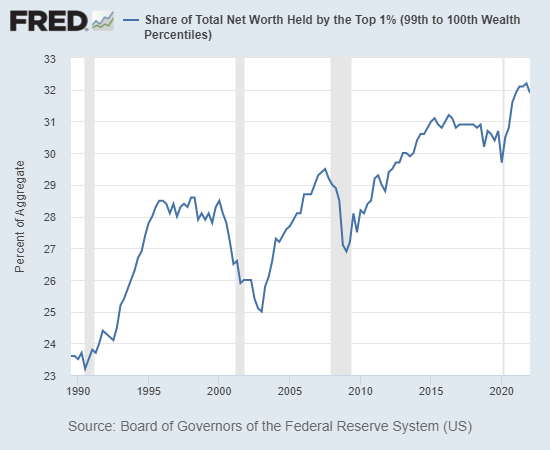

Chart #7: net worth of the top 1% households, which soared from 23% of all net worth to 32%: this 9% gain in the percentage of all household net worth represents a gain of $14 trillion above and beyond the $28.7 trillion in gains registered by the 23% they owned in 1990.

1990 total net worth: $21 trillion, 23% = $4.8 trillion; 2023 total net worth: $146 trillion, 23% = $33.5 trillion; $33.5 trillion – $4.8 trillion = $28.7 trillion.

This unprecedented bubble in housing valuations is due not to shortages but to decades of massive financial stimulus that incentivized speculative capital to flood into housing as a low-risk way to skim stupendous gains for creating zero gains in productivity. If you doubt this, then run this scenario and tell us what happens:

The Fed dumps its entire portfolio of mortgage backed securities and stipulates it will never buy any again. It also renounces all the other stimulus gimmicks that incentivized expansions of debt and speculation.

Does anyone really believe that the renunciation of massive, sustained stimulus of speculation in housing would leave housing valuations unchanged because valuations are solely the result of “shortages”? If so, there’s a little shack under the Brooklyn Bridge I’ll let you have for a couple of million. I’m sure the Airbnb rent will mint you millions.

If you listen to conventional economists, everything’s rosy: thanks to the expansion of alt-energy like wind and solar, energy is getting cheaper, batteries will power the new global economy, we’re getting smarter — just look at the rising number of advanced college degrees, wages are finally growing, inflation is trending down, household balance sheets and corporate profits are strong, debt loads are not an issue yet and GDP is rising.

All this happy news is backed by statistics, of course, but there’s one little problem: all the conventional cheerleaders are living in a bubble of like-minded elites who are insulated from the neofeudal realities of life in the real world.

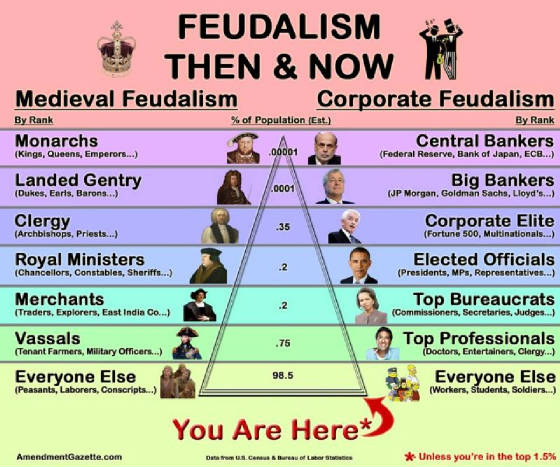

Outside the bubble of wealthy, protected elites that generate the statistics and the “news,” the global economy is completely, totally neofeudal–and so is the American economy. What does neofeudal mean? It refers to a two-tiered socio-economic system in which an aristocracy owns the vast majority of the wealth and collects the lion’s share of the income, and uses this financial dominance to buy political and narrative dominance.

In a neofeudal arrangement, the machinery of governance protects and enforces elite dominance. Cartels and monopolies have free rein to price-fix and exploit, tax revenues flow freely to cartels, elite organizations such as family trusts get tax breaks, and so on.

In other words, “the market” is rigged and the government maintains the status quo.

Toiling away to enrich the aristocratic owners of capital are the serfs and peasants, who own a tiny shred of income-producing capital. Their primary assets–the family home and vehicles–are actually income streams for the wealthy who collect the mortgage and auto-loan interest paid by the serfs.

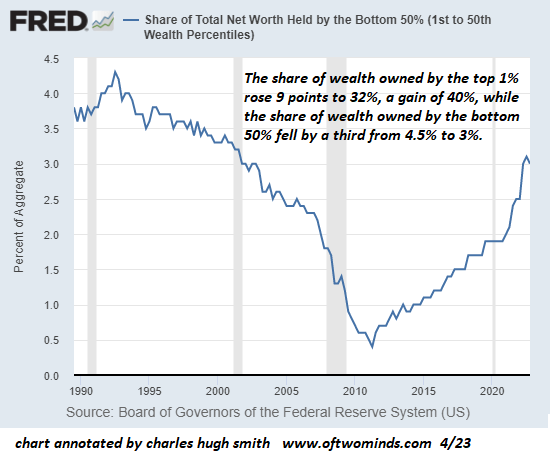

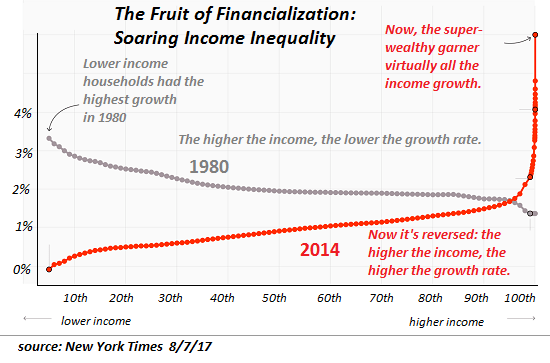

The core dynamic in neofeudalism is the already-wealthy increase their share of the wealth, and everyone else sees their meager share diminish. As the charts below show, the vast majority of financial gains generated by the US economy flow to the top 0.1% of households. The top 1%’s share has risen by 40% while the bottom 50%’s share of the wealth has slipped to 3%–essentially signal noise.

Social mobility is limited to the occasional serf clawing their way into the technocrat class, the top 5% who slavishly serve the interests of the financial aristocracy. This class lives in a self-contained, protected bubble: an echo chamber of privilege, residential enclaves, jetting around the world, and so on: everything’s great because we’re doing great.

Life is good in the bubble because there’s no homeless encampment a block away, there’s plenty of money coming in and our wealth–401Ks, inherited bonds and rental property, university pensions, corporate stock options, and so on–increases smartly, year after year and decade after decade.

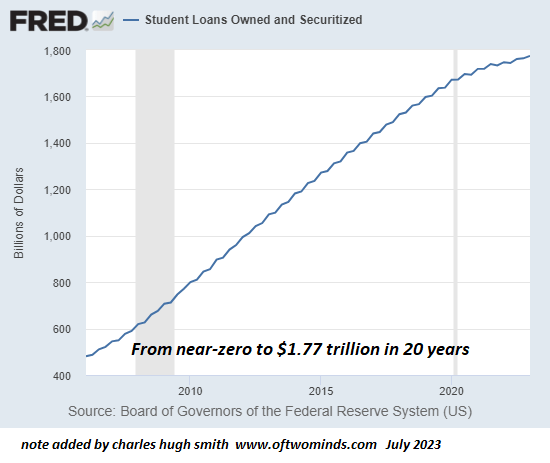

That all this wealth expansion is the result of unprecedented central bank intervention is left unsaid. As noted above, the role of the state and central bank is to maintain the status quo of the already-wealthy increasing their share of the national wealth and income, and loading more (very profitable) debt on the serfs. (See student loan debt chart below.)

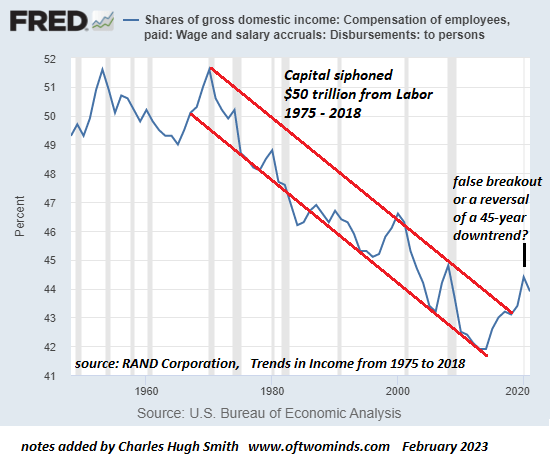

Outside the technocrats’ privileged bubble, wages’ share of the economy have been stripmined by the aristocracy for 45 years. Oh dear; could this be why I’m having such trouble finding low-wage reliable “help”?

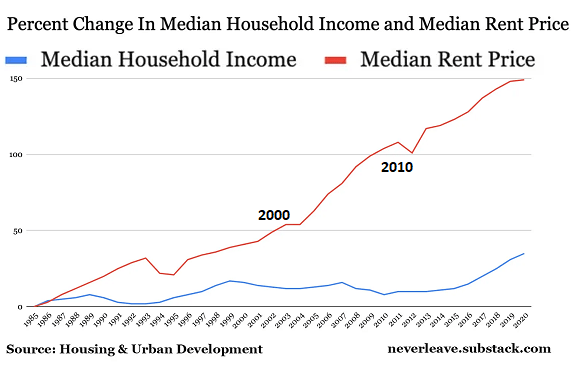

While wages inch up, costs of shelter, utilities, debt, vehicles, public transport, childcare and other essentials soar. Please glance at the chart of wages and rents below. This is neofeudalism in a nutshell. Wages have flatlined (or fallen when measured in purchasing power) while rent has steadily increased, eating away at the serfs’ disposable income.

Inside the technocrat class bubble, everything’s wunnerful. AI will boost profits (all of which flow to the aristocracy, so that’s wunnerful), energy’s getting cheaper and more abundant, and so on.

Oh, wait. Alt-energy only looks cheap because all the full lifetime costs have been ignored (i.e. externalized), and these modest additions to our vast hydrocarbon consumption aren’t actually replacing hydrocarbons, they’re simply adding more energy for us to consume.

In other words, conventional economists and the other technocrats maintain their privileged bubble by clinging to a delusionally disconnected-from-the-real-world mindset. There’s always a slew of academic papers or think-tank / corporate reports to bolster the inside-the-bubble confidence that everything’s great, because generating positive narratives that leave the neofeudal structure untouched in the primary industry of the technocrat class.

If you want to understand the neofeudal reality, study these charts. There are no rebuttals, there are only sputtering obfuscations: b-b-but the mission to Mars! Taylor Swift raked in a billion bucks! OnlyFans pulled in $5 billion! Stocks are rallying! Everything’s great!

Sure–if your dose of Delusional is high enough. Then you can go back to complaining about air travel delays, finding someone to repair your pool pump and bragging about how well your investments are doing.

Today, we are witnessing the nudging (manipulation) of the population to accept a ‘new normal’ based on a climate emergency narrative, restrictions on movement and travel, programmable digital money, ‘pandemic preparedness’ courtesy of the World Health Organization’s tyrannical pandemic treaty, unaccountable AI and synthetic ‘food’.

Whether it involves a ‘food transition’, an ‘energy transition’, 15-minute cities or some other benign-sounding term, all this is to be determined by a supranational ‘stakeholder’ elite with ordinary people sidelined in the process. An undemocratic agenda designed to place restrictions on individual liberty, marking a dramatic shift towards authoritarianism.

In the 1980s, to help legitimise the deregulation-privatisation neoliberal globalisation agenda, government and media instigated an ideological onslaught, driving home the primacy of ‘free enterprise’, individual rights and responsibility and emphasising a shift away from the role of the state, trade unions and the collective in society.

We are currently seeing another ideological shift: individual rights and freedoms are said to undermine the wider needs of society and the planet – in a stark turnaround – personal freedom is now said to pose a threat to national security, public health or the climate.

As in the 1980s, this messaging is being driven by an economic impulse. This time, the collapsing neoliberal project.

The Bank of England’s chief economist, Huw Pill, says that people should ‘accept’ being poorer. This is similar to the response of Rob Kapito, co-founder of the world’s biggest asset management firm, BlackRock. In 2022, the unimaginably rich and entitled Kapito said that a “very entitled” generation of (ordinary working) people who have never had to sacrifice would soon have to face shortages for the first time in their lives.

While business as usual prevails in Kapito’s world of privilege and that of major arms, energy, pharmaceuticals and food companies, whose megarich owners continue to rake in massive profits, Kapito and Pill tell ordinary people to get used to poverty and the ‘new normal’ as if we are ‘all in it together’ – billionaires and working class alike. They conveniently use COVID and the situation in Ukraine as cover for the collapsing neoliberalism.

But this is part of the hegemonic agenda that seeks to ensure that the establishment’s world view is the accepted cultural norm. And anyone who challenges this world view – whether it involves, for instance, questioning climate alarmism, the ‘new normal’, the nature of the economic crisis, the mainstream COVID narrative or the official stance on Ukraine and Russia – is regarded as a spreader of misinformation and the ‘enemy within’.

Although the term ‘enemy within’ was popularised by Margaret Thatcher during the miners’ strike in 1984-85 to describe the striking miners, it is a notion with which that Britain’s rulers have regarded protest movements and uprisings down the centuries. From the Peasants’ Revolt in 1381 to the Levellers and Diggers in the 17th century, it is a concept associated with anyone or any group that challenges the existing social order and the interests of the ruling class.

John Ball, a radical priest, addressed the Peasants’ Revolt rebels with the following words:

Good friends, matters cannot go well in England until all things be held in common; when there shall be neither vassals nor lords; when the lords shall be no more masters than ourselves.”

The revolt was suppressed. John Ball was captured and hung, drawn and quartered. Part of the blood-soaked history of the British ruling class.

Later on, the 17th-century Diggers movement wanted to create small, egalitarian rural communities and farm on common land that had been privatised by enclosures.

The 1975 song ‘The world Turned Upside Down’ by Leon Rosselson commemorates the Diggers. His lyrics describe the aims and plight of the movement. In Rosselson’s words, the Diggers were dispossessed via theft and murder but reclaimed what was theirs only to be violently put down.

Little surprise then that, in the 1980s, Margaret Thatcher used the state machinery to defeat the country’s most powerful and trade union and the shock troops of the labour movement, the National Union of Mineworkers – ‘the enemy within’. She needed to do this to open the gates for capital to profit from the subsequent deindustrialisation of much of the UK and the dismantling of large parts of the welfare state.

And the result?

A hollowed-out, debt-bloated economy, the destruction of the social fabric of entire communities and the great financial Ponzi scheme – the ‘miracle’ of deregulated finance – that now teeters on the brink of collapse, leading the likes of Kapito and Pill to tell the public to get ready to become poor.

And now, in 2023, the latest version of the ‘enemy within’ disseminates ‘misinformation’ – anything that challenges the official state-corporate narrative. So, this time, one goal is to have a fully controlled (censored) internet.

For instance, US Special Operations Command (USSOCOM) recently awarded Accrete a contract for Argus to detect disinformation threats from social media. Argus is AI software that analyses social media data to predict emergent narratives and generate intelligence reports at a speed and scale to help neutralise viral disinformation threats.

In a recent press release, Prashant Bhuyan, founder and CEO of Accrete, boasts:

Social media is widely recognised as an unregulated environment where adversaries routinely exploit reasoning vulnerabilities and manipulate behaviour through the intentional spread of disinformation. USSOCOM is at the tip of the spear in recognising the critical need to identify and analytically predict social media narratives at an embryonic stage before those narratives evolve and gain traction. Accrete is proud to support USSOCOM’s mission.”

This is about predicting wrong think on social media. But control over the internet is just part of a wider programme of establishment domination, surveillance and dealing with protest and dissent.

The authors of the article ask us to consider some of the ways the US government is weaponizing its surveillance technologies to flag citizens as a threat to national security, whether or not they have done anything wrong – from flagging citizens as a danger based on their feelings, phone and movements to their spending activities, social media activities, political views and correspondence.

The elite has determined that the existential threat is you. The article ‘Costs of War: Peterloo’, written by UK Veterans for Peace member Aly Renwick, details the history of the brutal suppression of protesters by Britain’s rulers. He also strips away any notion that some may have of a benign, present-day ruling elite with democratic leanings. The leopard has not changed its spots.

As we saw during COVID, the thinking is that hard-won rights must be curtailed, freedom of association is reckless, free thinking is dangerous, dissent is to be stamped on, impartial science is a threat and free speech is deadly. Government is ‘the truth’, Fauci (or some similar figure) is ‘the science’ and censorship is for your own good.

The economic crisis is making many people poorer, so they must be controlled, monitored and subjugated.

The transitions mentioned at the start of this article along with the surveillance agenda (together known as the ‘Great Reset’) are being accelerated at this time of economic crisis when countless millions across the West are being impoverished. The collapsing financial system is resulting in an interrelated global debt, inflation and ‘austerity’ crisis and the biggest transfer of wealth to the rich in history.

As a result, the powers that be fear that the masses might once again pick up their pitchforks and revolt. They are adamant that the peasants must know their place.

But the flame of protest and dissent from centuries past still inspires and burns bright. So, with that in mind, let’s finish with Leon Rosselson’s lyrics in reference to the Diggers movement (Billy Bragg’s version of the song can be found on YouTube):

In sixteen forty-nine To St. George’s Hill A ragged band they called the Diggers Came to show the people’s will They defied the landlords They defied the laws They were the dispossessed reclaiming what was theirs

We come in peace they said To dig and sow We come to work the lands in common And to make the waste grounds grow This earth divided We will makе whole So it will be A common treasury for all

Thе sin of property We do disdain No man has any right to buy and sell The earth for private gain By theft and murder They took the land Now everywhere the walls Spring up at their command

They make the laws To chain us well The clergy dazzle us with heaven Or they damn us into hell We will not worship The God they serve The God of greed who feed the rich While poor man starve

We work we eat together We need no swords We will not bow to masters Or pay rent to the lords We are free men Though we are poor You Diggers all stand up for glory Stand up now

From the men of property The orders came They sent the hired men and troopers To wipe out the Diggers’ claim Tear down their cottages Destroy their corn They were dispersed Only the vision lingers on

You poor take courage You rich take care The earth was made a common treasury For everyone to share All things in common All people one We come in peace The order came to cut them down We come in peace The order came to cut them down

Economic issues are some of the most politically abused issues often because the data politicians exploit is easy to present out of context. The vast majority of the public doesn’t spend their time immersed in the intricacies of monetary policy, unemployment stats and the processes of inflation vs deflation. They hear a soundbite on the news or social media once in a while, assume it must be true and then go on with their day.

This is how economic crisis events always seem to take the population by surprise – The establishment tells people all is well and no one questions the narrative in the face of numerous warning signs. Sometimes, the populace continues to believe that everything is fine despite the financial framework burning down around them, all because the “experts” continue to convince them that recovery is “right around the corner.”

There are numerous incentives for government officials and mainstream economists to mislead the citizenry with tales of imminent prosperity in the midst of instability. Primarily, the goal is to keep the middle-class population as docile as possible so that they don’t revolt until it’s too late (the middle class being predominantly conservative, and the greatest threat to any corrupt regime). Understand that economics is the root of power, and economic perception is the key to influencing the masses.

Hidden Indicators And Rampant Money Printing

The reality is that the US was hurtling towards stagflationary disaster ever since the crash of 2008, when Barack Obama and Joe Biden (with the help of the Federal Reserve) oversaw the near doubling of the national debt from $10 trillion to almost $20 trillion – The most egregious abuse of monetary policy that the US had ever seen.

And, keep in mind this was only the officially reported cash. Because of pressure brought by people like Ron Paul in 2011, the government was forced to pursue a limited audit of the Federal Reserve bailouts at that time. This revealed at least $16 trillion created from nothing by the Fed to prop up the failing system.

In 2006, right before the derivatives collapse, the Federal Reserve conveniently and abruptly ended their M3 money supply report. They now only report the M2 money supply, which does not include the vast assets held in corporate coffers, large time deposits in banks, institutional money market funds, short-term repurchase agreements (repo), and larger liquid assets. It was as if they knew an inflationary event was about to take place and they needed to obscure the evidence.

In other words, in economics there is the “official government data” and then there is the REAL data, which is sometimes so hidden it is impossible to quantify.

Even if we only go by the M2 report, the money supply skyrocketed starting in 2020, and rose exponentially through 2021 and 2022 – It jumped by 40% in only two years. This is why the cost of most necessities has risen 25% or more.

I’m sure most readers have noticed that inflation is not going away despite Joe Biden’s claims that he has “cut inflation in half” under his “Bidenomics” plan. This is because inflation is cumulative. The CPI might fluctuate, but the effects of inflation remain as prices tend to increase and stay high perpetually.

There Is No Such Thing As “Bidenomics”

The supposed financial progress that Biden is trying to take credit for has nothing to do with Biden’s policies. Not a thing. Unless, of course, you count market manipulation as a positive.

For example, the reduction in CPI is directly related to the continuous interest rate hikes of the Federal Reserve, which Biden has zero control over. The Fed is autonomous and makes its decisions independent of the White House or government. This is a fact openly admitted by former chairman Alan Greenspan. When the fed raises rates, debt becomes more expensive, lending slows down and thus the economy slows down.

One of the only ways that Biden can influence CPI is through artificial deflation of energy prices. The Biden Administration has been dumping US strategic oil reserves on the market for the past year as a means to suppress oil prices, thereby directly and indirectly keeping the CPI numbers down. This is not progress, it’s economic fraud.

The misuse of stats extends to other sectors, such as Biden’s attempt to take credit for the recent reduction in the US deficit. Again, this has nothing to do with Biden; the Fed’s interest rate hikes make it more expensive for the government to take on debt, therefore, debt spending drops.

It’s also not a situation that signals a recovery in the economy – The Fed continues to hike rates supposedly to stall inflation, but higher rates in a debt heavy environment lead to inevitable deflationary upheaval. As I predicted a year ago, the Fed is continuing to increase interest rates until this happens.

Employment Miracle Or Employment Scam?

This issue has been brought up by many analysts but I’ll touch on it again here because Biden is relentless in his falsehoods when it comes to employment data. FACT: 72% of all “new jobs” Biden takes credit for were originally lost during the pandemic lockdowns. The very lockdowns which Democrats avidly enforced and tried to keep in place perpetually. You can’t take credit for “creating” jobs that you are responsible for destroying.

In terms of higher labor demand, the pressure is in low wage service sector jobs and these are the majority of jobs added since Biden took office. And, this rush into retail/service was purchased with $8 trillion+ in covid stimulus cash along with a moratorium on rent and student loan payments. That much extra money in circulation buys at least a few years of consumer spending, propping up jobs numbers.

Throughout history, such gains from inflationary actions and government interventions are always short term, and they always end with a dramatic plunge in employment once the effects subside.

Biden’s Fake Manufacturing Boom

Biden has recently touted a jump in US manufacturing as the latest achievement of Bidenomics, but like every other claim he makes, you have to look at the context. These are not free market manufacturing facilities built according to market demand. Rather, Biden is pumping billions of taxpayer dollars into green tech, once again artificially engineering a “manufacturing boom” through government subsidies for products that have limited demand.

Biden wants to rig the demand, too, by enforcing climate laws which make gas, oil and coal sources too expensive and solar panels and wind turbines cheaper by comparison. For example, Biden is increasing costs for oil and gas exploration on federal lands, while greatly lowering the prices for building solar farms on federal lands. In other words, the government uses your money to create factories for green tech and then creates laws which force people to use that green tech.

In the meantime, Joe’s manufacturing “boom” paid for with tax dollars also comes at the cost of America’s oil, gas and coal industries, not to mention less energy freedom for the general public. It’s socialism, not a revolution in domestic manufacturing.

For Biden, The Key Is To Create As Many Government Cash Injections As Possible Until 2025

You want to know why Democrats are so angry that the Supreme Court blocked Biden’s plan to make taxpayers cover student loan debts? It’s not because they care about naive college kids who paid too much money for garbage degrees – It’s because student debt relief would immediately add trillions more in spending in the short term to the US economy.

An interesting side effect of the college loan moratorium is the surprising credit boost – As soon as college loan payments were put on hold, millions of former students had their credit ratings increase by default. Meaning, they could now hike their credit limits and spend MORE money they don’t have. It’s an incredibly sneaky way to artificially prop up the system WITHOUT using direct stimulus measures that rely on the central bank. This false boost will disappear by October of this year.

Biden’s constant attempts to introduce infrastructure programs are another way the government can create the illusion of recovery by using debt spending as a means to mitigate the signals of greater fiscal decline. Without Fed stimulus it’s the only option Biden has, and as rates rise it becomes costly.

The bottom line is this – The US economy is on a short timetable as long as the Fed continues to raise interest rates into weakness as a means to suppress inflation. As we witnessed in the spring, higher rates are already breaking the back of mid-tier banks across the western world and the Fed’s backstop funds are only enough to stall the debt crisis for a time. I continue to predict that once the Fed Funds Rate is raised to 6% or more, we will once again see a banking calamity similar to the 2008 crash, but this time if the Fed steps in with a bailout hyperinflation will be the immediate result.

Bidenomics is a sham in every respect. Anything that could be considered an economic improvement is due to the Federal Reserve playing the odds with interest rates. A massive 40% increase in the money supply sure helps in obscuring fiscal weakness as well. Luckily, nearly 60% of Americans in recent polls say they aren’t buying the Bidenomics fairytale – They see the dangers around them every day.

The covid event was a catalyst that revealed all the weaknesses of the US system that many of us in alternative economics have been warning about for years. And now it seems as if the establishment is trying to drag things along for just a little while longer. The reason why is up for speculation, but the fact remains that a broken structure cannot be propped up with stop gaps. I’m doubtful that Biden will be able to ride the wave created by covid stimulus until the end of 2024. Something has to give.

I do not claim any expertise in social contract theory, but in broad brush we can delineate two implicit contracts: one between the citizenry and the state (government) and another between citizens.

We can distinguish between the two by considering a rural county fair. Most of the labor to stage the fair is volunteered by the citizenry for the good of their community and fellow citizens; they are not coerced to do so by the government, nor does the government levy taxes to pay its employees or contractors to stage the fair.

The social contract between citizens implicitly binds people to obeying traffic laws as a public good all benefit from, not because a police officer is on every street corner enforcing the letter of the law.

The social contract between the citizens and the state binds the government to maintaining civil liberties, equal enforcement of the rule of law, defending the nation, and in the 20th century, providing social welfare for the disadvantaged, disabled and low-income elderly.

Critiques of “trickle down economics” focus on income inequality as a key metric of the Social Contract: rising income inequality is de facto evidence that the Social Contract is broken.

I think this misses the key distinction in the Social Contract between citizens and the state, which is the legitimacy of the process of wealth creation and the fairness of the playing field and the referees, i.e. that no one is above the law.

Few people begrudge legitimately earned wealth, for example, the top athlete, the pop star, the tech innovator, the canny entrepreneur, the best-selling author, etc. The source of these individual’s wealth is transparent, and any citizen can decline to support this wealth creation by not paying money to see the athlete, not buying the author’s books, not shopping at the entrepreneur’s stores, etc.

The Social Contract is broken not just by wealth inequality per se but by the illegitimate process of wealth acquisition, i.e. the state has tipped the scales in favor of the few behind closed doors and routinely ignores or bypasses the intent of the law even as the state claims to be following the narrower letter of the law.

By this definition, the Social Contract in America has been completely smashed. One sector after another is dominated by cartel-state partnerships that are forged and enforced in obscure legislation written by lobbyists. Once the laws have been riddled with loopholes and the regulators have been corrupted, “no one is above the law” has lost all meaning.

Those who violate the intent of the law while managing to conjure an apparent compliance with the letter of the law are shysters, scammers and thieves who exploit the intricate loopholes of the system, all the while parading their compliance as evidence the system is fair and just. In this way, the judicial system becomes part of the illegitimate process of wealth accumulation.

In America, political and financial Elites are above the intent of the law. Is bribery of politicos illegal? Supposedly it is, but in practice it is entirely and openly legal.

This is the norm in banana republics, whose ledgers are loaded with thousands of codes and regulations that are routinely ignored by those in power. In the Banana Republic of America, financial crimes go uninvestigated, unindicted and unpunished: banks and their management are essentially immune to prosecution because the crimes are complex (tsk, tsk, it’s really too much trouble to investigate) and they’re “too big to prosecute.”

The rot has seeped from the financial-political Aristocracy to the lower reaches of the social order. The fury of those still working legitimate jobs and paying their taxes is grounded in a simple, obvious truth: America is now dominated by scammers, cheaters, grifters and those gaming the system, large and small, to increase their share of the swag.

The honest taxpayer is a chump, a mark who foolishly ponies up the swag that’s looted by the smart operators. Everyone knows that the vast majority of wealth accumulation in America flows not from transparent effort on a level playing field, but from persuading the Central State (the Federal government and the Federal Reserve) to enforce cartels and grant monopolistic favors such as tax shelters designed for a handful of firms and unlimited credit to private banks.

When scammers large and small live better than those creating value in the real economy, the Social Contract has ceased to exist. When the illegitimate process of wealth acquisition–a rigged playing field, a bought-off referee, and an Elite that’s above the law by every practical measure–dominates the economy and the political structure, the Social Contract has been shattered, regardless of how much welfare largesse is distributed to buy the complicity of state dependents.

Once the chumps and marks realize there is no way they can ever escape their exploited banana-republic status as neofeudal debt-serfs, the scammers, cheats and grifters large and small will be at risk of losing their perquisites. The fantasy in America is that legitimate wealth creation is still possible despite the visible dominance of a corrupt, venal, self-absorbed, parasitic, predatory Aristocracy. Once that fantasy dies, so will the marks’ support of the Aristocracy.

As Voltaire observed, “No snowflake in an avalanche ever feels responsible”: every claim, every game of the system, every political favor purchased is “fair and legal,” of course. This is precisely how empires collapse.

In broad brush, we can trace the transition from feudalism to capitalism to the present financialized, globalized cartel-state neofeudalism and next, to a synthesis built on the opposite of neofeudalism, which is decentralization, transparency, accountability, legitimacy and the adaptive churn of competing ideas and proposals.

Let’s start with the basics. Roughly 5% of the human race currently live in the United States of America. That very small fraction of humanity, until quite recently, enjoyed about a third of the world’s energy resources and manufactured products and about a quarter of its raw materials. This didn’t happen because nobody else wanted these things, or because the US manufactured and sold something so enticing that the rest of the world eagerly handed over its wealth in exchange. It happened because, as the dominant nation, the US imposed unbalanced patterns of exchange on the rest of the world, and these funnelled a disproportionate share of the planet’s wealth to itself.

There’s nothing new about this sort of arrangement. In its day, the British Empire controlled an even larger share of the planet’s wealth, and the Spanish Empire played a comparable role further back. Before then, there were other empires, though limits to transport technologies meant that their reach wasn’t as large. Nor, by the way, was any of this an invention of people with light-coloured skin. Mighty empires flourished in Asia and Africa when the peoples of Europe lived in thatched-roofed mud huts. Empires rise whenever a nation becomes powerful enough to dominate other nations and drain them of wealth. They’ve thrived as far back as records go and they’ll doubtless thrive for as long as human civilisations exist.

America’s empire came into being in the wake of the collapse of the British Empire, during the fratricidal European wars of the early 20th century. Throughout those bitter years, the role of global hegemon was up for grabs, and by 1930 or so it was pretty clear that Germany, the Soviet Union or the US would end up taking the prize. In the usual way, two contenders joined forces to squeeze out the third, and then the victors went at each other, carving out competing spheres of influence until one collapsed. When the Soviet Union imploded in 1991, the US emerged as the last empire standing.

Francis Fukuyama insisted in a 1989 essay that having won the top slot, the US was destined to stay there forever. He was, of course, wrong, but then he was a Hegelian and couldn’t help it. (If a follower of Hegel tells you the sky is blue, go look.) The ascendancy of one empire guarantees that other aspirants for the same status will begin sharpening their knives. They’ll get to use them, too, because empires invariably wreck themselves: over time, the economic and social consequences of empire destroy the conditions that make empire possible. That can happen quickly or slowly, depending on the mechanism that each empire uses to extract wealth from its subject nations.

The mechanism the US used for this latter purpose was ingenious but even more short-term than most. In simple terms, the US imposed a series of arrangements on most other nations that guaranteed the lion’s share of international trade would use US dollars as the medium of exchange, and saw to it that an ever-expanding share of world economic activity required international trade. (That’s what all that gabble about “globalisation” meant in practice.) This allowed the US government to manufacture dollars out of thin air by way of gargantuan budget deficits, so that US interests could use those dollars to buy up vast amounts of the world’s wealth. Since the excess dollars got scooped up by overseas central banks and business firms, which needed them for their own foreign trade, inflation stayed under control while the wealthy classes in the US profited mightily.

The problem with this scheme is the same difficulty faced by all Ponzi schemes, which is that, sooner or later, you run out of suckers to draw in. This happened not long after the turn of the millennium, and along with other factors — notably the peaking of global conventional petroleum production — it led to the financial crisis of 2008-2010. Since 2010 the US has been lurching from one crisis to another. This is not accidental. The wealth pump that kept the US at the top of the global pyramid has been sputtering as a growing number of nations have found ways to keep a larger share of their own wealth by expanding their domestic markets and raising the kind of trade barriers the US used before 1945 to build its own economy. The one question left is how soon the pump will start to fail altogether.

When Russia launched its invasion of Ukraine in February 2022, the US and its allies responded not with military force but with punitive economic sanctions, which were expected to cripple the Russian economy and force Russia to its knees. Apparently, nobody in Washington considered the possibility that other nations with an interest in undercutting the US empire might have something to say about that. Of course, that’s what happened. China, which has the largest economy on Earth in purchasing-power terms, extended a middle finger in the direction of Washington and upped its imports of Russian oil, gas, grain and other products. So did India, currently the third-largest economy on Earth in the same terms; as did more than 100 other countries.

Then there’s Iran, which most Americans are impressively stupid about. Iran is the 17th largest nation in the world, more than twice the size of Texas and even more richly stocked with oil and natural gas. It’s also a booming industrial power. It has a thriving automobile industry, for example, and builds and launches its own orbital satellites. It’s been dealing with severe US sanctions since not long after the Shah fell in 1978, so it’s a safe bet that the Iranian government and industrial sector know every imaginable trick for getting around those sanctions.

Right after the start of the Ukraine war, Russia and Iran suddenly started inking trade deals to Iran’s great benefit. Clearly, one part of the quid pro quo was that the Iranians passed on their hard-earned knowledge about how to dodge sanctions to an attentive audience of Russian officials. With a little help from China, India and most of the rest of humanity, the total failure of the sanctions followed in short order. Today, the sanctions are hurting the US and Europe, not Russia, but the US leadership has wedged itself into a position from which it can’t back down. This may go a long way towards explaining why the Russian campaign in Ukraine has been so leisurely. The Russians have no reason to hurry. They know that time is not on the side of the US.

For many decades now, the threat of being cut out of international trade by US sanctions was the big stick Washington used to threaten unruly nations that weren’t small enough for a US invasion or fragile enough for a CIA-backed regime-change operation. Over the last year, that big stick turned out to be made of balsa wood and snapped off in Joe Biden’s hand. As a result, all over the world, nations that thought they had no choice but to use dollars in their foreign trade are switching over to their own currencies, or to the currencies of rising powers. The US dollar’s day as the global medium of exchange is thus ending.

It’s been interesting to watch economic pundits reacting to this. As you might expect, quite a few of them simply deny that it’s happening — after all, economic statistics from previous years don’t show it yet, Some others have pointed out that no other currency is ready to take on the dollar’s role; this is true, but irrelevant. When the British pound lost a similar role in the early years of the Great Depression, no other currency was ready to take on its role either. It wasn’t until 1970 or so that the US dollar finished settling into place as the currency of global trade. In the interval, international trade lurched along awkwardly using whatever currencies or commodity swaps the trading partners could settle on: that is to say, the same situation that’s taking shape around us in the free-for-all of global trade that will define the post-dollar era.

One of the interesting consequences of the shift now under way is a reversion to the mean of global wealth distribution. Until the era of European global empire, the economic heart of the world was in east and south Asia. India and China were the richest countries on the planet, and a glittering necklace of other wealthy states from Iran to Japan filled in the picture. To this day, most of the human population is found in the same part of the world. The great age of European conquest temporarily diverted much of that wealth to Europe, impoverishing Asia in the process. That condition began to break down with the collapse of European colonial empires in the decade following the Second World War, but some of the same arrangements were propped up by the US thereafter. Now those are coming apart, and Asia is rising. By next year, four of the five largest economies on the planet in terms of purchasing power parity will be Asian. The fifth is the US, and it may not be in that list for much longer.

In short, America is bankrupt. Our governments from the federal level down, our big corporations and a very large number of our well-off citizens have run up gargantuan debts, which can only be serviced given direct or indirect access to the flows of unearned wealth the US extracted from the rest of the planet. Those debts cannot be paid off, and many of them can’t even be serviced for much longer. The only options are defaulting on them or inflating them out of existence, and in either case, arrangements based on familiar levels of expenditure will no longer be possible. Since the arrangements in question include most of what counts as an ordinary lifestyle in today’s US, the impact of their dissolution will be severe.

In effect, the 5% of us in this country are going to have to go back to living the way we did before 1945. If we still had the factories, the trained workforce, the abundant natural resources and the thrifty habits we had back then, that would have been a wrenching transition but not a debacle. The difficulty, of course, is that we don’t have those things anymore. The factories were shut down in the offshoring craze of the Seventies and Eighties, when the imperial economy slammed into overdrive, and the trained workforce was handed over to malign neglect.

We’ve still got some of the natural resources, but nothing like what we once had. The thrifty habits? Those went whistling down the wind a long time ago. In the late stages of an empire, exploiting flows of unearned wealth from abroad is far more profitable than trying to produce wealth at home, and most people direct their efforts accordingly. That’s how you end up with the typical late-imperial economy, with a governing class that flaunts fantastic levels of paper wealth, a parasite class of hangers-on that thrive by catering to the very rich or staffing the baroque bureaucratic systems that permeate public and private life, and the vast majority of the population impoverished, sullen, and unwilling to lift a finger to save their soi-disant betters from the consequences of their own actions.

The good news is that there’s a solution to all this. The bad news is that it’s going to take a couple of decades of serious turmoil to get there. The solution is that the US economy will retool itself to produce earned wealth in the form of real goods and non-financial services. That’ll happen inevitably as the flows of unearned wealth falter, foreign goods become unaffordable to most Americans, and it becomes profitable to produce things here in the US again. The difficulty, of course, is that most of a century of economic and political choices meant to support our former imperial project are going to have to be undone.

The most obvious example? The metastatic bloat of government, corporate and non-profit managerial jobs in American life. That’s a sensible move in an age of empire, as it funnels money into the consumer economy, which provides what jobs exist for the impoverished classes. Public and private offices alike teem with legions of office workers whose labour contributes nothing to national prosperity but whose pay cheques prop up the consumer sector. That bubble is already losing air. It’s indicative that Elon Musk, after his takeover of Twitter, fired some 80% of that company’s staff; other huge internet combines are pruning their workforce in the same way, though not yet to the same degree.

The recent hullaballoo about artificial intelligence is helping to amplify the same trend. Behind the chatbots are programs called large language models (LLMs), which are very good at imitating the more predictable uses of human language. A very large number of office jobs these days spend most of their time producing texts that fall into that category: contracts, legal briefs, press releases, media stories and so on. Those jobs are going away. Computer coding is even more amenable to LLM production, so you can kiss a great many software jobs goodbye as well. Any other form of economic activity that involves assembling predictable sequences of symbols is facing the same crunch. A recent paper by Goldman Sachs estimates that something like 300 million jobs across the industrial world will be wholly or partly replaced by LLMs in the years immediately ahead.

Another technology with similar results is CGI image creation. Levi’s announced not long ago that all its future catalogues and advertising will use CGI images instead of highly-paid models and photographers. Expect the same thing to spread generally. Oh, and Hollywood’s next. We’re not too far from the point at which a program can harvest all the footage of Marilyn Monroe from her films, and use that to generate new Marilyn Monroe movies for a tiny fraction of what it costs to hire living actors, camera crews and the rest. The result will be a drastic decrease in high-paying jobs across a broad swathe of the economy.

The outcome of all this? Well, one lot of pundits will insist at the top of their lungs that nothing will change in any way that matters, and another lot will start shrieking that the apocalypse is upon us. Those are the only two options our collective imagination can process these days. Of course, neither of those things will actually happen.

What will happen instead is that the middle and upper-middle classes in the US, and in many other countries, will face the same kind of slow demolition that swept over the working classes of those same countries in the late 20th century. Layoffs, corporate bankruptcies, declining salaries and benefits, and the latest high-tech version of NO HELP WANTED signs will follow one another at irregular intervals. All the businesses that make money catering to these same classes will lose their incomes as well, a piece at a time. Communities will hollow out the way the factory towns of America’s Rust Belt and the English Midlands did half a century ago, but this time it will be the turn of upscale suburbs and fashionable urban neighbourhoods to collapse as the income streams that supported them disappear.

This is not going to be a fast process. The US dollar is losing its place as the universal medium of foreign trade, but it will still be used by some countries for years to come. The unravelling of the arrangements that direct unearned wealth to the US will go a little faster, but that will still take time. The collapse of the cubicle class and the gutting of the suburbs will unfold over decades. That’s the way changes of this kind play out.

As for what people can do in response this late in the game, I refer to a post I made on The Archdruid Report in 2012 titled “Collapse Now and Avoid the Rush”. In that post I pointed out that the unravelling of the American economy, and the broader project of industrial civilisation, was picking up speed around us, and those who wanted to get ready for it needed to start preparing soon by cutting their expenses, getting out of debt, and picking up the skills needed to produce goods and services for people rather than the corporate machine. I’m glad to say that some people did these things, but a great many others rolled their eyes, or made earnest resolutions to do something as soon as things were more convenient, which they never were.

Over the years that followed I repeated that warning and then moved on to other themes, since there really wasn’t much point to harping on about the approaching mess when the time to act had slipped away. Those who made preparations in time will weather the approaching mess as well as anyone can. Those who didn’t? The rush is here. I’m sorry to say that whatever you try, it’s likely that there’ll be plenty of other frantic people trying to do the same thing. You might still get lucky, but it’s going to be a hard row to hoe.

Mind you, I expect some people to take a different tack. In the months before a prediction of mine comes true, I reliably field a flurry of comments insisting that I’m too rigid and dogmatic in my views about the future, that I need to be more open-minded about alternative possibilities, that wonderful futures are still in reach, and so on. I got that in 2008 just before the real estate bubble started to go bust, as I’d predicted, and I also got it in 2010 just before the price of oil peaked and started to slide, as I’d also predicted, taking the peak oil movement with it. I’ve started to field the same sort of criticism once again.

We are dancing on the brink of a long slippery slope into an unwelcome new reality. I’d encourage readers in America and its close allies to brace themselves for a couple of decades of wrenching economic, social, and political turmoil. Those elsewhere will have an easier time of it, but it’s still going to be a wild ride before the rubble stops bouncing, and new social, economic, and political arrangements get patched together out of the wreckage.

This is how we’ll end up with severe shortages of truly skilled labor and high unemployment of those who lack the necessary skills.

The labor force and the job market are referred to as if they were monolithic structures. But they’re not monolithic, they are complex aggregates of very different cohorts of age, skills, mobility, education, experience, opportunity, potential and motivation.

As a result, numbers such as the unemployment rate tell us very little about the labor force and the job market in terms of what matters going forward. So what does matter going forward?

1. Demographics–the aging and retirement of key sectors of the work force.

2. Skills and experience that will be increasingly scarce due to mismatched demand for skills that are diminishing as older workers retire.

3. What skills and experience will be demanded by re-industrialization, reshoring and expanding the electrification of the economy.

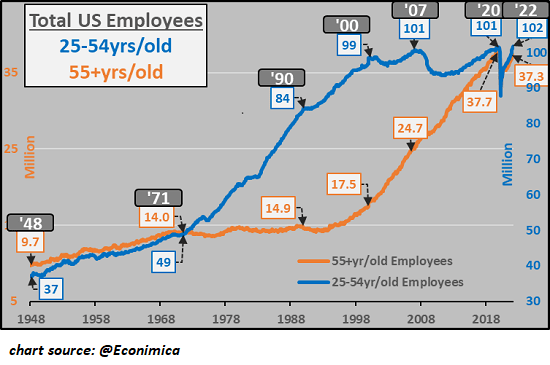

Consider these two charts of the US work force by age. (Courtesy of CH @econimica) In the first chart, Total US Employees, note that the prime working age work force (ages 25-54) has been flatlined for the past 20 years at 101-102 million. In contrast, the 55-and-older cohort of employees soared from 17 million to 37 million. This increase of 20 million accounts for virtually all growth in the employed work force.

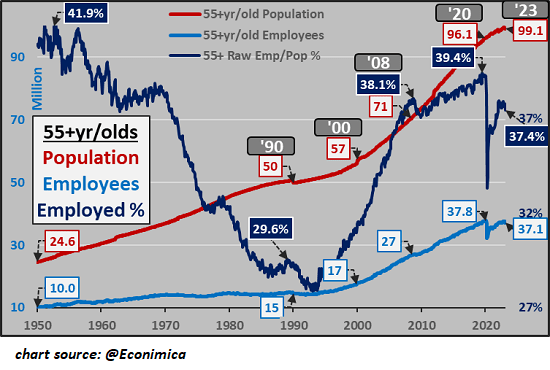

A funny thing happens as workers get old; they retire and leave the work force. Their skills and experience are no longer available to employers or the nation’s economy. The second chart shows the aging of the American populace, as the 55+ cohort increased from 57 million to 99 million since 2000, as the number of older employees skyrocketed from 17 million to 37 million.

While the total US population increased by 18% from 281 million in 2000 to 331 million today, the 55+ cohort increased 74% (from 57 million to 99 million).

The key takeaway here is the number of experienced workers who will retire in the next decade will track the explosive growth in the 55+ cohort. The general consensus is this will not be a problem because there are plenty of younger workers available to fill the vacated slots.

But this overlooks the qualitative and quantitative differences in the millions leaving the work force and those joining the work force. This is especially consequential in real-world jobs, i.e. all those jobs that require engaging real-world materials rather than staring at screens.

Though few analysts and commentators will admit to it, the implicit assumption is that the jobs that matter all involve staring at screens–processing data, finance, entertainment and shaping narrative make the world go round. All the real-world stuff (boring!) will magically get done by tax donkeys who are out of sight, out of mind.

This mindset has it backwards: it’s the real-world work of changing the industrial / energy / energy distribution foundation of the economy that matters going forward, not the staring-at-screens jobs.

What few seem to realize is the work force that’s aging and retiring is the cohort with the real-world skills. It’s a nice idea to remake the entire electrical grid of the nation to transport much larger quantities of electrical power, but who’s going to do all that work? Young people whose career goals are becoming YouTube influencers or day-traders? No. All the ChatAI bots in the world aren’t going to get the real work done, either.

In other words, there is a massive mismatch between the skills available to hire in the young-worker cohort and the skills and experience needed to rebuild the material, real-world foundations of the US economy. It’s well-known but apparently not worth worrying about that the average age of the US farmer is pushing 60 years of age. Nobody left to grow all our food? Hey, isn’t there a ChatAI bot to do all that for us? It can all be automated, right? No? Well, why not? Somebody out there, get it done! Food in super-abundance should be delivered to everyone staring at screens 24/7, it’s our birthright.

The average age of skilled tradespeople is also skewed to the aging work force. There is no easy way to quantify real-world skills gained by on-the-job experience. I suspect it follows a power-law distribution: the newly minted worker just out of school / apprenticeship can handle basic functions, but when tough problems arise, the number of workers with the requisite experience to diagnose and fix the problem diminishes rapidly.

This distribution presents an enormous problem for the economy and employers. Once the super-experienced workers who can solve any problem leave, they cannot be replaced by inexperienced workers. So when the really big problems arise, the systems will break down because those who knew how to deal with the problems are no longer available.

This is how you can have 10 million unemployed workers and 1 million unfilled positions that can’t be filled because few are truly qualified. You want to erect new electrical transmission lines? Nice, but you’re not going to get the job done with green workers accustomed to staring at screens. It takes years of hard labor to acquire even a bare minimum of the skills required. These are not assembly-line jobs that can be filled by unskilled labor, these are jobs in the messy real world, not a distribution center.

As I note in my book on Self-Reliance, individuals with a full spectrum of real-world skills are now extremely rare. Skills that were once common are now performed by specialists. We seem to have all the time in the world to stare at hundreds of cooking programs on TV but how many people actually prepare three meals a day, week in, week out, month in, month out, year in, year out? How many people know how to repair anything, build anything, or maintain a machine?

My direct experience is that many young people don’t know how to put air in the tires of the vehicle Mom and Dad gave them. Young people with graduate-level diplomas don’t know what a green bean plant looks like. (Eeew, gross, it grows in dirt?) The cultural value system that only values wealth, regardless of its source, and minting money from staring at screens has generated a fundamental mismatch between the skills that will be needed going forward and the skills being presented as oh-so-valuable.

Yes, there are many young workers with sharp real-world skills. The question is, are there enough?

This is how we’ll end up with severe shortages of truly skilled labor and high unemployment in the cohort of workers with few real-world skills and a surplus of skills for which there is limited demand. As a real-world experiment, go find a tough old rancher and ask them a series of questions about livestock, machinery, fencing, generators, etc., and then ask the average newly minted college graduate that followed the warped values embedded in our economy the same questions.

Of course the young worker can’t match the experience of the old worker, but do they have any experience at all of a spectrum of essential real-world skills? If not, do they have the requisite physical endurance and commitment needed to acquire real-world skills?

Who’s going to do all the real-world work going forward? A few people talk about it as an abstraction, but it’s not an issue to everyone focused on Federal Reserve policy or GDP. But eventually, the real world will matter more than staring at screens and day-trading, because when the systems break down due to lack of truly qualified employees, we’ll all wake up. But by then it will be too late. We’ll be staring at dead screens begging for somebody somewhere to restore power so we can continue playing with ChatAI to trade zero-day options.

The resulting erosion of collateral will collapse the global credit bubble, a repricing/reset that will bankrupt the global economy and financial system.

Scrape away the complexity and every economic crisis and crash boils down to the precarious asymmetry between collateral and the debt secured by that collateral collapsing. It’s really that simple.

In eras of easy credit, both creditworthy and marginal borrowers are suddenly able to borrow more. This flood of new cash seeking a return fuels red-hot demand for conventional assets considered “safe investments” (real estate, blue-chip stocks and bonds), demand which given the limited supply of “safe” assets, pushes valuations of these assets to the moon.

In the euphoric atmosphere generated by easy credit and a soaring asset valuations, some of the easy credit sloshes into marginal investments (farmland that is only briefly productive if it rains enough, for example), high-risk speculative ventures based on sizzle rather than actual steak and outright frauds passed off as legitimate “sure-fire opportunities.”

The price people are willing to pay for all these assets soars as the demand created by easy credit increases. And why does credit continue increasing? The assets rising in value create more collateral which then supports more credit.

This self-reinforcing feedback appears highly virtuous in the expansion phase: the grazing land bought to put under the plow just doubled in value, so the owners can borrow more and use the cash to expand their purchase of more grazing land. The same mechanism is at work in every asset: homes, commercial real estate, stocks and bonds: the more the asset gains in value, the more collateral becomes available to support more credit.

Since there’s plenty of collateral to back up the new loans, both borrowers and lenders see the profitable expansion of credit as “safe.”

This safety is illusory, as it’s resting on an unstable pile of sand: bubble valuations driven by easy credit. We all know that price is set by what somebody will pay for the asset. What attracts less attention is price is also set by how much somebody can borrow to buy the asset.

Once the borrower has maxed out their ability to borrow (their income and assets-owned cannot support more debt) or credit conditions tighten, then those who might have paid even higher prices for assets had they been able to borrow more money can no longer borrow enough to bid the asset higher.

Since price is set on the margin (i.e. by the last sales), the normal churn of selling is enough to push valuations down. At first the euphoria is undented by the decline, but as credit tightens (interest rates rise and lending standards tighten, cutting off marginal buyers and ventures) then buyers become scarce and skittish sellers proliferate.

Questions about fundamental valuations arise, and sky-high valuations are found wanting as tightening credit reduces sales, revenues and profits. Once the “endless growth” story weakens, the claims that bubble prices are “fair value” evaporate.

As defaults rise, lenders are forced to tighten credit further. The first tumbling rocks are ignored but eventually the defaults trigger a landslide, and the credit-inflated bubble in asset valuations collapses.

As valuations plummet, so too does the collateral backing all the new debt. Debt that appeared “safe” is soon exposed as a potential push into insolvency. When the bungalow doubled in value from $500,000 to $1 million, the trajectory of valuation gains looked predictably rosy: every decade housing prices went up 30% or more. So originating a mortgage for $800,000 on a house that looked to be worth $1.3 million in a few years looked rock-solid safe.

But the $1 million was a bubble based solely on easy, abundant, low-cost credit. When credit tightens, the home is slowly but surely repriced at its pre-bubble valuation ($500,000) or perhaps much lower, if that value was merely an artifact of a previous unpopped bubble.

Now the collateral is $300,000 less than the mortgage. The owner who made a down payment of $200,000 will be wiped out by a forced sale at $500,000, and the lender (or owner of the mortgage) will take a $300,000 loss.

Given the banking system is set up to absorb only modest, incremental losses, losses of this magnitude render the lender insolvent. The lender’s capital base is drained to zero by the losses and then pushed into negative net-worth by continued losses.

The collateral collapses when bubbles pop, but the debt loaned against the now-phantom collateral remains.

This is the story of the Great Depression, a story that’s unloved because it calls into question the current series of credit-inflated bubbles and resulting financial crises. So the story is reworked into something more palatable such as “the Federal Reserve made a policy error.”

This encourages the fantasy that if central banks choose the right policies, credit bubbles and valuations detached from reality can both keep expanding forever. The reality is credit bubbles always pop, as the expansion of borrowing eventually exceeds the income and collateral of marginal borrowers, and this tsunami of cash eventually pours into marginal high-risk speculative vebtures that go bust.

There is no way to thread the needle so credit-asset bubbles never pop. Yet here we are, watching the global Everything Bubble finally start collapsing, guaranteeing the collapse of collateral and all the debt issued on that collateral, and the rabble is arguing about what policy tweaks are needed to reinflate the bubble and save the global economy from bankruptcy.

Sorry, but global bankruptcy is already baked in. Too much debt has been piled on phantom-collateral and income streams derived from bubble assets rising (for example, capital gains, development taxes, etc.). The asymmetry is now so extreme that even a modest decline in asset valuations/collateral due to a garden-variety business-cycle recession of tightening financial conditions will trigger the collapse of The Everything Bubble and the mountain of global debt resting on the wind-blown sands of phantom collateral.

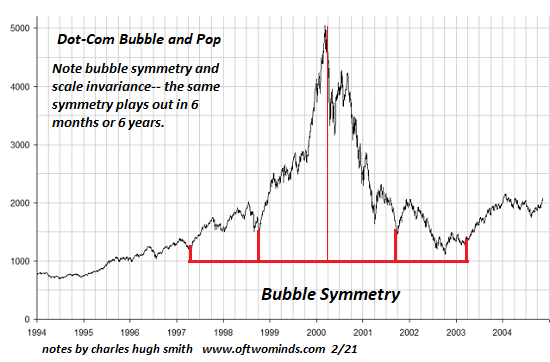

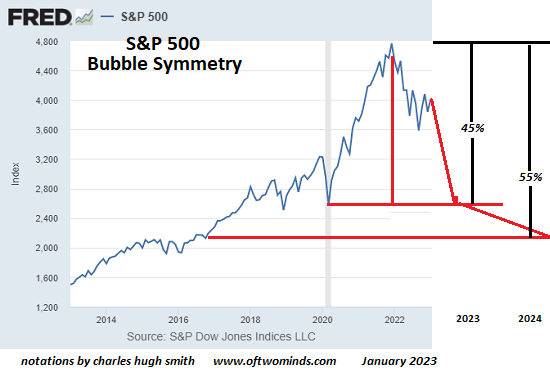

There are persuasive reasons to suspect global debt far exceeds the official level around $300 trillion, most saliently, the largely opaque shadow banking system. When assets roughly double in a few years, bubble symmetry suggests that valuations will decline back to the starting point of the bubble in roughly the same time span.

The resulting erosion of collateral will collapse the global credit bubble, a repricing/reset that will bankrupt the global economy and financial system.