By Charles Hugh Smith

Source: Of Two Minds

Are we heading into another real estate bubble / crash? Those who say “no” see the housing shortage as real, while those who say “yes” see the demand as a reflection of the Federal Reserve’s artificial goosing of the housing market via its unprecedented purchases of mortgage-backed securities and “easy money” financial conditions.

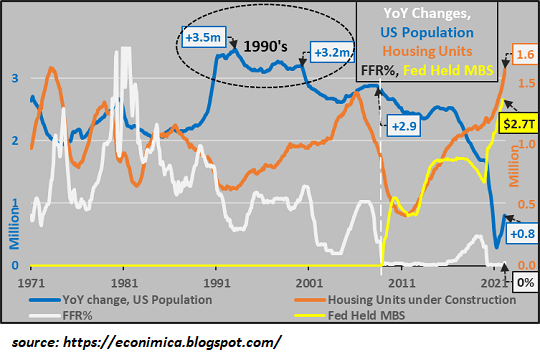

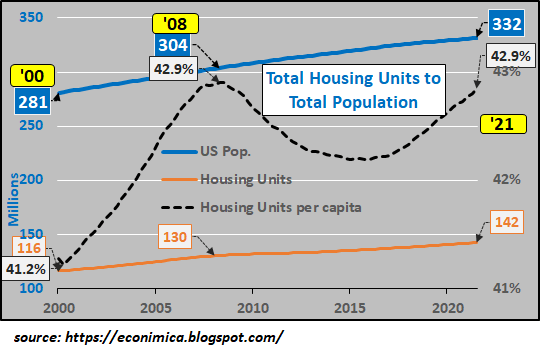

My colleague CH at econimica.blogspot.com recently posted charts calling this assumption into question. The first chart (below) shows the U.S. population growth rate plummeting as housing starts soar, and the second chart shows housing unit per capita, which has just reached the same extreme as the 2008 housing bubble.

Demographics and housing do not reflect a housing shortage nationally, though there could be scarcities locally, of course, and other factors such as thousands of units being held off the market as short-term rentals or investments by overseas buyers who have no interest in renting their investment dwellings.

On a per capita basis, housing has reached previous bubble levels. That suggests housing shortages are artificial or local, not structural.

Next, let’s consider how the current housing bubble differs from previous bubbles in the late 1970s and 2000s. In my view, the previous bubbles were driven by demographics, inflation and monetary policy: in the late 70s, the 65 million-strong Baby Boom generation began buying their first homes, pushing demand higher while inflation soared, making real-world assets such as housing more desirable.

Once the Federal Reserve pushed interest rates to 18%, mortgage rates rose in lockstep and housing crashed as few could afford sky-high housing prices at sky-high mortgage rates.

The housing bubble of 2007-08 was largely driven by declines in mortgage rates (as the Fed pursued an “easy money” policy to escape the negative effects of the Dot-Com stock market bubble crash) and a loosening of credit/mortgage standards. These fueled a bubble that morphed into a speculative free-for-all of no-down payment and no-document loans.

This decline in the cost of borrowing money (mortgage rates) enabled a sharp rise in the price of housing, a speculative boom that was greatly accelerated by “innovations” in the mortgage market such as zero down payments loans, interest-only loans, home equity loans, and no-document “liar loans”–mortgages underwritten without the usual documentation of income and net worth.

These forces generated a speculative frenzy of house-flipping, leveraging the equity in the family home to buy two or three homes under construction and selling them before they were even completed for fat profits, and so on.

Needless to say, the pool of potential buyers expanded tremendously when people earning $25,000 a year could buy $500,000 houses on speculation.

Once the bubble popped, the pool of buyers shrank along with the home equity.

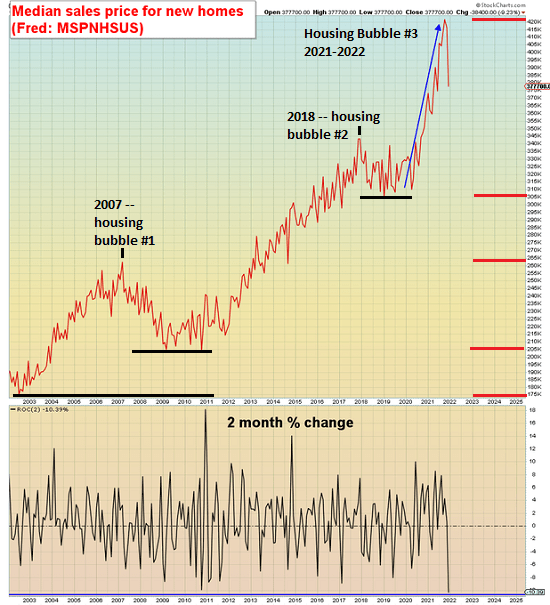

If we study this chart below of new home prices (courtesy of Mac10), we can see that the 21st century’s Bubble #2 rose as the Federal Reserve pushed mortgage rates far below historic norms. Once rates reached a bottom, the 7-year inflation of home prices (from 2011 to 2018) began rolling over.

This deflation of home prices was reversed by the pandemic recession, as the Fed’s vast expansion of credit and mortgage-buying, which pushed mortgage rates to new lows. Trillions of dollars in new credit and cash stimulus ignited a speculative frenzy in stocks, bonds and real estate, a frenzy which drove bubble #3 to extraordinary heights.

All this unprecedented fiscal and monetary stimulus also ignited inflation, and so rates are rising in response. Bubble #3 is already deflating, at least by the measure of new home prices.

But the current bubble has a number of dynamics that weren’t big factors in previous bubbles.

One is the rise of remote work. Many people have been working remotely since the late 1990s enabled Internet-based work, but the pandemic greatly increased the pool of employers willing to accept remote work as a permanent feature of employment.

This trend has been well documented, but the consequences are still unfolding: remote workers are no longer trapped in unaffordable, congested cities and suburbs.

Several other trends have attracted much less attention, but I see them as equally consequential.

1. Housing in many urban zones are out of reach of all but the top 10% without extraordinary sacrifice, and now that employment isn’t necessarily tied to urban zones, the bottom 90% of young people without family wealth or high incomes are coming to realize the benefits of urban living are not worth the extreme sacrifices needed to buy an overvalued house.

A middle-class life–home ownership, financial security, leisure and surplus income to invest in one’s family and well-being–is no longer affordable for the majority of young Americans.

Few are willing to concede this because it reveals the neofeudal nature of American life. Those who bought homes in coastal urban zones 20+ years ago are wealthy due to soaring housing valuations while young people can’t even afford the rent, much less buying a house.

If you’re not making $250,000 or more a year as a couple, the only hope for a middle-class life that includes leisure and some surplus income to invest is top move to some place with much lower housing and other costs. That place is rural America.

2. The benefits of urban living are deteriorating while the sacrifices and downsides are increasing. Urban living is fun if you’re wealthy, not so fun if you don’t have plenty of surplus income to spend.

Urban problems such as homelessness, traffic congestion and crime are endemic and unresolvable, though few are willing to state the obvious. Americans are expected to be optimistic and to count on some new whiz-bang technology to solve all problems.

Unfortunately, problems generated by dysfunctional, overly complex institutions, corruption and unaffordable costs can’t be solved by some new technology, and so the decay of cities will only gather momentum.

The hope that billions of federal stimulus funding would solve these problems is about to encounter reality as the funds dry up and all the problems remain or have actually expanded despite massive “investments” in solutions.

Few analysts have looked at the finances of high-cost cities. The decline in bricks-and-mortar retail, rising crime, soaring junk fees, rents and property taxes have all made urban small business insanely costly and therefore risky.

Small businesses are the core sources of employment and taxes. As high costs, crime, etc. choke small businesses, employment and tax revenues drop and commercial real estate sits empty, generating decay and defaults.

Once office and retail space is no longer affordable or necessary, commercial real estate crashes in value as owners who bought at the top default and go bankrupt.

People need shelter but they don’t need office space or to start a bricks-and-mortar retail business.

As urban finances unravel, cities won’t have the funding to run their bloated, inefficient, overly complex and unaccountable bureaucracies.

3. In geopolitics, we speak of the core and the periphery. Empires have a core (Rome and central Italy in the Roman Empire) and a periphery (Britain, North Africa, Egypt, the Levant).

As finances and trade decay and costs soar, the periphery is surrendered to maintain the core.

In urban zones, the same dynamic will become increasingly visible: the peripheral neighborhoods will be underfunded to continue protecting the wealthy enclaves.

Crime will skyrocket in the periphery even as residents of the wealthy enclaves see little decay in their neighborhoods.

This asymmetry–already extreme–will drive social unrest and disorder. This is a self-reinforcing feedback: as the periphery neighborhoods deteriorate, the remaining businesses flee and the smart money sells and moves away.

Tax revenues plummet and city services decay even further, persuading hangers-on to move before it gets even worse. Cities compensate for the lower revenues by increasing taxes on the remaining residents and cutting services.

Each turn of the screw triggers more closures and selling and fewer tax revenues.

4. Dependency chains will become increasingly consequential: the greater a city’s dependency on essentials trucked/shipped from hundreds or thousands of of kilometers/miles away, the more prone that city will be to disruptions of essentials: food, energy, materials and infrastructure.

Though few are willing to dwell on such vulnerabilities, most cities are totally dependent on diesel fueled fleets of trucks, rail and jet fuel for luxuries flown in from afar for virtually all goods. Cities produce very little in the way of essentials such as food and energy.

The past reliability of long supply chains has instilled a confidence that these supply chains stretching thousands of kilometers and miles are unbreakable and forever. They aren’t, and the initial disruptions will be a great shock to Americans who believe full gas tanks and fully stocked store shelves are their birthright.

5. As I’ve explained in my new book Global Crisis, National Renewal, the era of cheap, reliable abundance has drawn to a close and now we are entering an era of scarcity in essentials.

Another reality few discuss is the relative stability of global weather over the past 40 years. As weather becomes less reliable, so too do crop yields and food supplies.

Globalization has poured capital into expanding acreage under cultivation to the point that the planet’s forests are being decimated to grow more soy to feed animals to be slaughtered for human consumption.

On the margins, land that was once productive has been lost to desertification. Fresh water aquifers have been drained and glaciers feeding rivers are melting away. Soil fertility has declined even as fertilizer use has expanded.

The low-hanging fruit of GMO seeds, fertilizers, insecticides, herbicides and Green Revolution hybrids have all been plucked. The gains have been reaped but now the downsides of these dependencies are becoming increasingly consequential: fertilizer costs are rising fast, insects and diseases are evading chemicals and vaccines, and the vulnerabilities of mono-crop, industrialized agriculture and animal husbandry threaten to cascade into crop failures, soaring prices and shortages.

6. This will have two consequences: rural incomes which have been falling for decades due to globalization (i.e. bringing in cheap food from places with no environmental standards, cheap labor and few taxes / social costs) will start rising sharply, fueling a reversal in the long decline of rural communities based on agricultural income.

The soaring costs of essentials will reduce the disposable income of the bottom 90%, reducing the money they’ll have to spend on eating out, retail shopping, etc.–all the surplus spending that drives cities’ economies and tax revenues.

Few (if any) commentators forecast a cyclical reversal of the demographic trend of people moving from rural locales to cities. I think this trend has already reversed and will gather momentum as cities become increasingly unlivable, disposable incomes decline as scarcities push prices higher and people flee for lower cost, more secure environs.

7. As I often note, following what the super-wealthy are doing is a pretty sound investment strategy because the super-wealthy spend freely to buy the best advice and are highly motivated to protect their wealth.

People who live in well-known, highly desirable rural towns (Telluride, Jackson Hole, Lake Tahoe, etc.) are describing a feeding frenzy of wealthy urbanites buying multi-million dollar homes. Small cities such as Bozeman, MT and Ashville, NC are experiencing a flood of new residents that is straining infrastructure and pushing housing prices out of reach for local residents with average wages.

8. Rural towns in the U.S., Italy, Japan and even Switzerland are trying to attract new residents with offers of free land, subsidized rent, low cost homes, etc. This shows that the trends are global and not limited to any one nation. Would you take free land in rural America?

The decay of urban life isn’t yet consequential enough to push people into making a major move, but once someone has been robbed, repeatedly found human feces on their doorstep or experienced scarcities that trigger the madness of crowds, the decision to leave becomes much, much easier.

Some cities will manage the decline of employment and tax revenues more gracefully than others. Most will suffer from the dynamic I’ve often described on the blog: the Ratchet Effect. Costs move effortlessly higher as tax revenues have increased in one speculative bubble after another, but once revenues drop, cities have no mechanisms or political constituency to manage a sharp, long-term decline in revenues.

They then become prone to the other dynamic I’ve described, the Rising Wedge Breakdown (see chart below): as agencies and institutions become sclerotic, unaccountable and self-serving, even a relatively modest cut in revenues triggers institutional collapse, as the system requires 100% funding to function. A 10% reduction doesn’t cause a 10% decline in service, it causes an 50% decline in service, on the way to complete dysfunction.

Few believe cities can unravel, but remote work, geographic arbitrage (discussed below), tightening credit, rising crime, the decline of commercial real estate, end of massive stimulus, scarcities, the madness of crowds, the decline of civic services and amenities and an insanely high cost of living all have consequences and second-order effects.

What were beneficial synergies become fatal synergies as dynamics reverse and begin reinforcing each other.

So let’s put all this together.

A. The cycle of declining interest rates and inflation has ended and a cycle of much higher interest and mortgage rates and inflation is beginning. Higher mortgages rates will depress housing prices as only the highest income households will be able to afford today’s prices once mortgage rates rise.

B. The decay of urban finances and quality of life will accelerate as stimulus ends, credit dries up and inflation decimates disposable income.

C. The stress of trying to make enough money to afford the high costs of city/suburban living as the real estate bubble pops and the benefits of city living decline will burn out increasing numbers of people who will have no choice but to find more affordable, more secure and more livable places.

D. While the wealthy have already secured second or third homes in the toniest desirable towns, there are still opportunities for lower cost, more secure residences in rural areas.

E. This migration, even at the margins, will further depress urban housing prices and push prices in desirable rural locales higher.

F. This migration will have regional, ethnic and cultural variations. For example, some African-Americans leaving the upper Midwest are finding favor with communities in the South where family, church and cultural ties beckon.

G. Correspondent John F. used the phrase geographic arbitrage which means earning money remotely in high-wage sectors while living some place that’s low cost and secure.

I wrote about this many years ago in my post about young Japanese maintaining a part-time remote-work gig while pursuing farming in rural communities: Degrowth Solutions: Half-Farmer, Half-X (July 19, 2014).

H. Though monetary / inflationary forces will pop housing prices based solely on low mortgage rates, this doesn’t mean housing everywhere will decline: as burned out urbanites seek lower cost, more secure and livable places in rural locales, homes in desirable towns and small cities could rise sharply because they’re starting from such low levels.

I. If urban areas decay rapidly, housing prices could plummet much faster than most people think possible.

When cities lose employment, tax revenues and desirability, they can go down fast. Property values can fall in half and then by 90%.

How is this possible? Supply and demand: if demand falls off a cliff, there won’t be buyers for thousands of homes that come on the market all at once. This is just like a stock market in which buyers disappear, as no one wants to buy an asset that’s rapidly losing value.

As I’ve noted many times, prices for assets are set on the margins: the last sale of a house resets the price for the entire neighborhood.

The stock market is easily manipulated by the big players, who can stop a slide in prices by buying huge chunks of stocks and call options. There are no equivalent forces which can stop a decline in housing prices.

And since rates will rise regardless of what the Federal Reserve does because global capital is demanding a real return above inflation, then the hope for lower mortgage rates to support bubble-level housing prices will be in vain.

How low could housing go? As explained above, there will likely be very asymmetric declines and increases in housing valuations going forward. But on a technical-analysis level, we can anticipate a general decline to previous lows, first to the 2019 lows and then to the 2011 lows.

Some analysts believe inflation will funnel capital into housing as investors seek assets that will go up with inflation, but this is a murky forecast: the bottom 90% of American households are already priced out of coastal housing, so inflation only robs their wages of purchasing power. They don’t have any hope of buying a house anywhere near current prices.

Corporations are buying thousands of houses for the rental income, but once all the stimulus runs out and the excesses of speculation reverse, they’ll find few renters can afford their sky-high rents. At that point corporate buyers become corporate sellers, but they won’t find buyers willing or able to pay their asking prices, which are based on bubble pricing, not reality.

All these swirling currents will affect housing valuations in different places differently. Some areas could see 50% declines while others see 50% increases, regardless of mortgage rates or Fed policy.

What will become most desirable is a low cost of living, security and livability, which includes community, reduced dependency on long supply chains and local production of essentials.

We are all prone to believing the recent past is a reliable guide to the future. But in times of dynamic reversals, the past is an anchor thwarting our progress, not a forecast.